Compass Pathways: Deep Dive Analysis

A high risk / high reward small-cap biotech investment thesis in a field I understand the most.

Overview & Positioning

Compass Pathways is a London-headquartered biotechnology company focused on developing new treatments for serious mental health conditions. Founded in 2016, the company is best known for COMP360, its investigational synthetic psilocybin treatment being developed primarily for treatment-resistant depression, with additional work including a Phase 2b/3 PTSD trial and Phase 2 data in anorexia nervosa.

The main author of Hated Moats is a board certified psychiatrist with a PhD in the field, and attended a lecture by professor Siegfried Kasper in 2022 about treatment of resistant depression and perspective of psychedelics in its treatment. Since then, I’ve been following the field closely for nearly 4 years now, and for the past 4 months, I’ve been also researching the companies developing these drugs. Since this is in the field of my life’s work, I do apologise for the length of this article in advance. :)

Compass Pathways is still a clinical-stage biotech, but it is no longer just a “psychedelics concept stock.” The company is now the most advanced classical-psychedelic developer in the public markets for Treatment-resistant depression (TRD). Its lead asset, the mentioned COMP360, has produced positive primary-endpoint results in two ongoing Phase 3 TRD trials, has U.S. Food and Drug Administration (FDA) Breakthrough Therapy designation, has been granted rolling NDA (New Drug Application) submission and review, and has been selected for the FDA Commissioner’s National Priority Voucher (CNPV) pilot program. Management says it expects to complete the NDA submission in Q4 2026. That is real regulatory lead, not just scientific promise.

We believe the company’s positioning is also more specific than the market sometimes gives it credit for. This is not a generic and recently popular “mental health platform.” It is a company building around a proprietary synthetic psilocybin formulation, a growing intellectual-property estate, and a defined care-delivery model for monitored administration in professional healthcare settings. We believe its current positioning is therefore strong - the first potential FDA-approved classic psychedelic in TRD, differentiated on speed of onset, durability, and a solid controlled-data package.

That being said, it still remains a development-stage business with no real product revenue and substantial losses (as it usually goes with companies at this stage). In 2025 it reported a net loss of $287.9 million (heavily distorted by a $122.6 million non-cash warrant-liability fair-value adjustment), and as of year-end it had $149.6 million of cash and cash equivalents. The company then completed a $150 million equity financing and received approximately $200 million from warrant exercises in February 2026. By March 31, 2026, cash and cash equivalents had increased to $466.0 million, and management said the current cash position should fund operating expenses and capital expenditure requirements into 2028. So, the equity story has clearly de-risked on science recently, partially on financing as well, but the company is still not self-funding and still depends on commercial execution going right on the first launch.

Commercially, management argues that the opportunity is meaningful because roughly 4 million U.S. patients are considered to have TRD, fewer than 200,000 receive an FDA-approved treatment indicated for TRD, and launch readiness work now includes payers, KOLs (Key Opinion Leaders - respected doctors, researchers, psychiatrists, academic clinicians, etc…), policymakers, product distribution, pricing, reimbursement, and site-of-care training in mind, with delivery planning across an existing infrastructure of more than 7,300 centers offering multi-hour treatments. That is exactly why this story now looks less like a typical early biotech scientific lottery ticket and more like an early commercial-franchise buildout.

Competitive Moat & Peer Comparison

The core moat is a biotech moat made of four main things, including regulatory lead, owned clinical data, intellectual property (IP), and an emerging provider-access infrastructure. On regulatory lead, the company is ahead of the field in classic psychedelics for TRD, with positive primary-endpoint results from two ongoing Phase 3 trials, rolling NDA submission and review underway, and selection for the FDA Commissioner’s National Priority Voucher pilot program. On IP, its 2025 annual report lays out a broad estate covering crystalline psilocybin, pharmaceutical formulations, methods of treatment, redosing schedules, and treatment with SSRIs (currently most used antidepressants), with estimated protection stretching roughly into 2038–2042. On commercialisation, management is already preparing pricing, reimbursement, site certification, field force, and policy work before approval.

But the moat is not impregnable, of course, especially at this stage. Particularly, the same filings that make the bull case also explain the vulnerability. COMP360, if approved, is expected to be subject to a REMS (Risk Evaluation and Mitigation Strategy) program and to rely on certified third-party treatment sites, trained healthcare professionals, and a proposed model involving at least six hours of post-dose monitoring by a licensed healthcare professional at a certified centre. The company doesn’t plan to directly employ most treating clinicians. That means the moat depends partly on external site buildout, provider training, reimbursement adequacy, and rescheduling logistics. In other words, the moat is real, but it is operationally complex and heavy.

Definium Therapeutics

As far as competition goes, the main name mentioned is Definium Therapeutics ( DFTX 0.00%↑ , fromerly MindMed ). But the contrast with CMPS 0.00%↑ is sharp. Definium’s lead franchise, DT120 ODT, is built around lysergide tartrate for Generalised anxiety disorder (GAD) and Major depressive disorder (MDD), with 3 pivotal readouts expected in 2026, Phase 3 expansion into PTSD, and $373.4 million of cash, cash equivalents, and investments as of March 31, 2026, which management says should fund operations into 2028. Definium also emphasises a multi-layered IP strategy, including issued patents covering pharmaceutical formulation, manufacturing, and treatment, as well as a broader lysergide patent/application estate with expected expirations around 2041–2044 if issued, plus an 8-hour pivotal-study monitoring period and a potential 5–8-hour real-world monitoring model that it argues could support single-visit reimbursement, although reimbursement and coding have not yet been established. The market is already giving this story a meaningfully larger capitalisation of about $2.3B versus roughly $1.4B for Compass.

The key difference is that Definium’s moat thesis is scalability across bigger diagnostic markets, not current regulatory lead in TRD. It is further behind in terms of filing readiness for a commercial product, but its treatment model is explicitly being designed for standalone drug effect, broader labels, and a more efficient clinic workflow. So if we are ranking “commercial elegance,” Definium may already have the cleaner playbook. If we are ranking “who is closest to turning psychedelic psychiatry into an approved product,” Compass still has the lead, which is why we chose Compass for our analysis and investment. However, we believe that both companies have potential to do well.

AtaiBeckley

Against AtaiBeckley ( ATAI 0.00%↑ ), we believe the comparison is even more important because it is more directly TRD-on-TRD. AtaiBeckley’s BPL-003 is a proprietary intranasal mebufotenin benzoate program with Breakthrough Therapy designation, granted U.S./U.K./European composition-of-matter patents, and a Phase 3 program on track to initiate in Q2 2026. It is explicitly pitching a short, roughly two-hour in-clinic experience, no in-session psychotherapy, and seamless integration into existing interventional psychiatry workflows, including those already used for Spravato (esketamine). The company reported $209.9 million of cash, cash equivalents, and short-term securities as of March 31, 2026, and says its cash position should fund operations into 2029, covering the anticipated early-2029 Phase 3 BPL-003 topline readouts.

That makes AtaiBeckley the most serious structural threat to Compass’s future moat. Compass currently wins on timing, evidence maturity, and regulatory momentum. To be fair and remain objective, due to mentioned, AtaiBeckley may eventually win on convenience, practice economics, and potentially stronger composition-of-matter protection if its Phase 3 results replicate the earlier signal. The two companies are at roughly similar market capitalisations, which implies the market isn’t yet giving Compass a dominant monopoly-like commercial lead despite its much closer filing timeline.

Our bottom-line moat view is that the company’s regulatory moat is stronger than its delivery moat. Today, that is enough to make it the category leader. Over a five-year horizon, though, Compass doesn’t just need approval. It needs to prove that a six-hour monitored psilocybin session plus psychological support can beat shorter-duration, lower-friction rivals in real-world adoption and reimbursement. And that might not be easy. We still believe that Compass’s head start and first-mover advantage create a compelling investment case.

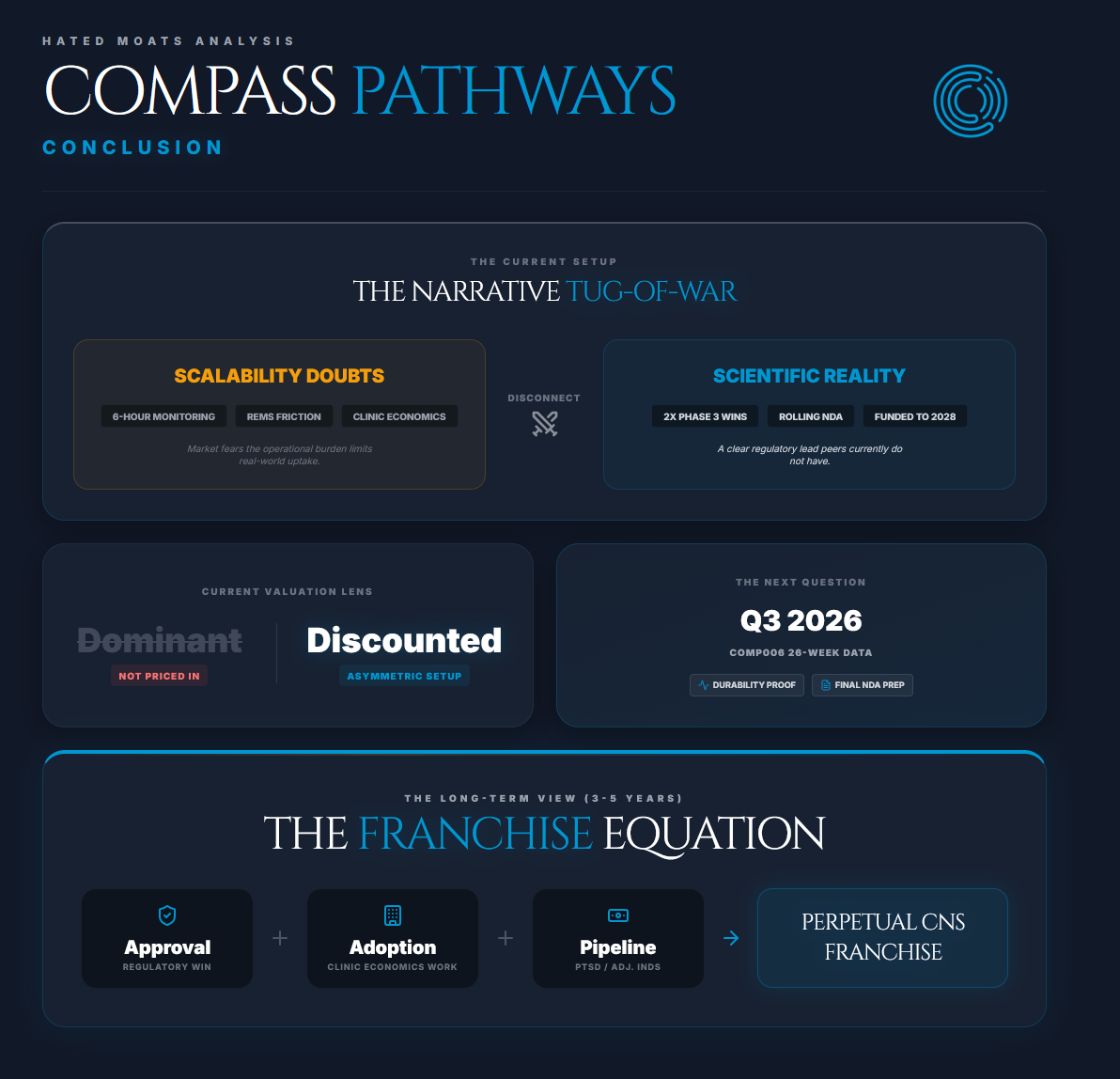

So, the question is “why choose Compass over the other two?”. Our preference is not because Compass has the cleanest eventual workflow. Definium and AtaiBeckley may both have more convenient commercial models if their pivotal data hold up. We chose Compass because its remaining risk has shifted further from ‘does the drug work in controlled trials?’ toward regulatory completion, launch execution, reimbursement, and delivery buildout. COMP360 has already produced positive primary-endpoint results in two Phase 3 TRD trials, rolling NDA submission and review are underway, and management says the company is funded into 2028. Definium still needs its 2026 GAD/MDD pivotal readouts, while AtaiBeckley’s BPL-003 pivotal TRD readouts are not expected until early 2029. Thus in our view, Compass offers the better near-term regulatory asymmetry. Definium and AtaiBeckley offer potentially attractive but later and more data-dependent scalability. We also note that we don’t really need to rely on long-term execution of the company in our investment. Re-rating and stock surge upon go-to-market readiness alone could be sufficient for a market beating result in terms of our ROIC.

Recent Stock Performance & Market Sentiment

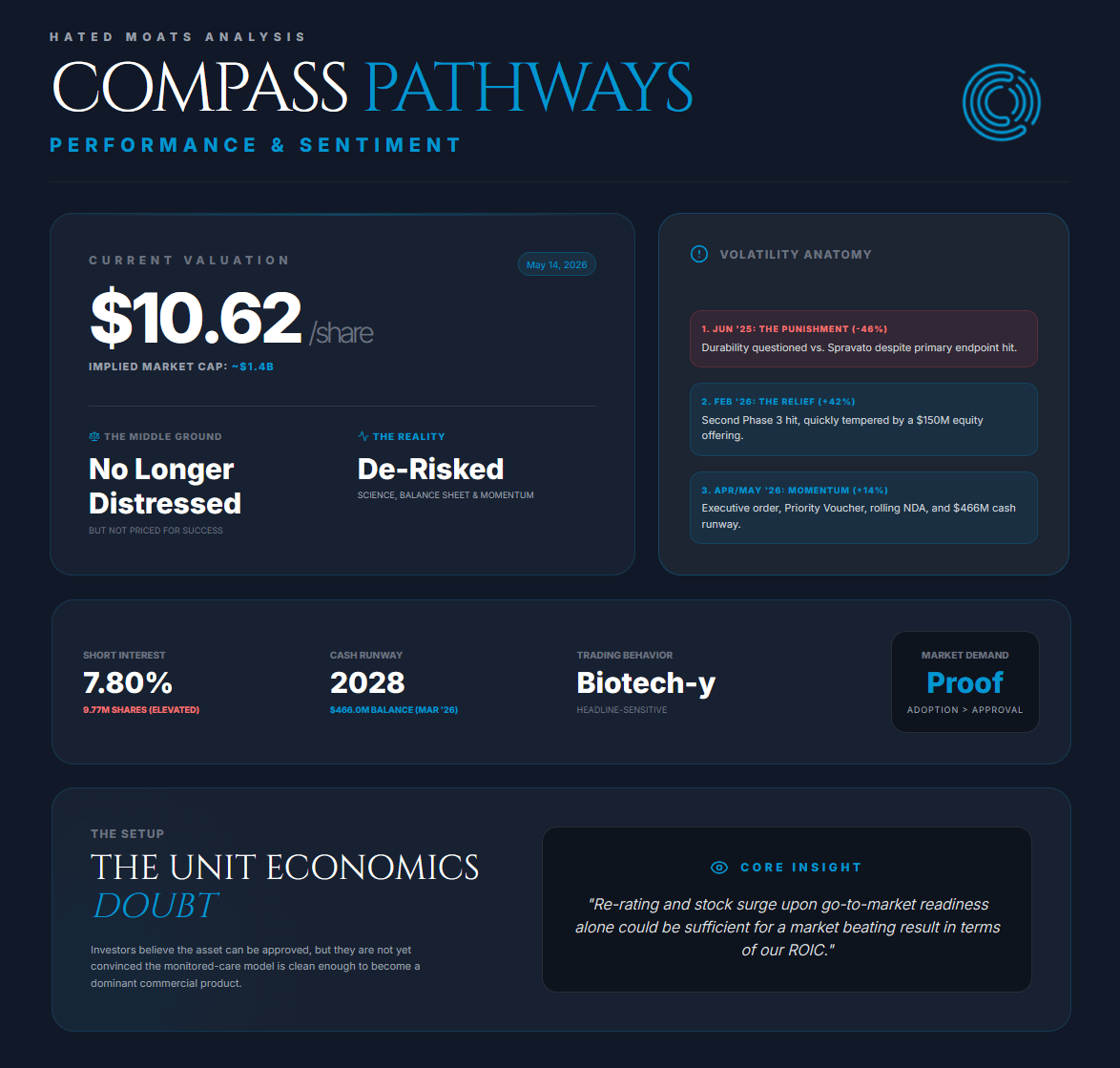

As of May 14, 2026, the shares closed at $10.62, implying a market cap of roughly $1.4B based on the company’s March 31 share count. The Q1 update pushed the stock to a two-year high. The current level still leaves the stock in a strange middle ground where it’s no longer distressed like it was after the first Phase 3 market’s disappointment in mid-2025, but still nowhere near priced like a de-risked near-commercial CNS company.

The market’s path over the last year explains the scepticism. On June 23, 2025, the shares fell more than 46% even though COMP005 hit its primary endpoint, because the treatment effect at 6 weeks came in below investor expectations and analysts questioned durability and commercial competitiveness versus Johnson & Johnson Spravato. Then sentiment flipped on February 17, 2026, when the second Phase 3 trial met its primary endpoint and the stock jumped nearly 42%. The celebration was quickly tempered by a $150 million equity offering priced at $8.00 per ADS the next day. In April 2026, the shares rallied again after President Trump signed an executive order directing faster review for breakthrough-designated psychedelic drugs and the FDA selected COMP360 for the Commissioner’s National Priority Voucher program while granting Compass rolling NDA submission and review. A further push upwards by roughly 14% came in May after Compass’s Q1 update, which highlighted $466.0 million of cash and cash equivalents at March 31, 2026, runway into 2028, and the ongoing accelerated regulatory path.

So the stock is being valued less like a clean secular grower and more like a headline-sensitive catalyst vehicle, i.e. biotech-y. That interpretation is reinforced by elevated short interest of about 9.77 million shares sold short, or 7.80% of float, as of April 30, 2026, down from about 11.01 million shares at April 15. At the same time, sell-side coverage is broad, spanning specialist biotech houses and larger brokers, which tells you the name is widely followed even if conviction remains uneven. In other words, a lot of people are watching, but the market still wants proof that “approval” will translate into “adoption.”

Our read on sentiment is that it has improved materially on science, balance-sheet risk, and regulatory momentum, but not yet on unit economics. That is why the market cap still looks modest relative to the regulatory lead. Investors believe the asset can be approved but they are not yet convinced the monitored-care model is clean enough to become a dominant commercial product.

Fundamental Analysis

Growth

Compass Pathways’ fundamentals now hinge on successful late‐stage trials and commercialisation plans, rather than traditional revenue growth. Compass has now achieved two positive Phase 3 TRD readouts for COMP360: COMP005 in June 2025 and COMP006 in February 2026. COMP005 showed a single 25 mg dose versus placebo produced a -3.6 point MADRS (Montgomery–Åsberg Depression Rating Scale) treatment difference at Week 6, while COMP006 showed two 25 mg doses versus a 1 mg comparator produced a -3.8 point MADRS treatment difference at Week 6, both with p<0.001. Management says rolling NDA submission and review are already underway, with sections of the NDA submitted, and that final NDA submission remains on track for Q4 2026, aligned with the company’s goal of being launch-ready by year-end (while targeting a U.S. TRD market of roughly 4 million patients of whom <5% currently receive an FDA-approved TRD treatment). COMP360 has Breakthrough Therapy designation (TRD) and promising Phase 2 data in PTSD (Phase 2b/3 study just initiated). In short, the “growth” story is driven by this pipeline and near-term regulatory milestones, not current sales. But with two pivotal trials positive, the company has a rare catalyst‐rich outlook.

Pipeline & Market Opportunity

As we mentioned, Compass’s lead program is COMP360 for TRD. The Phase 3 data to date show rapid onset, with effects seen as early as the day after dosing, and a generally well-tolerated safety profile with no unexpected safety findings. As a clinician in the field myself, I find that profile unusually compelling, while recognising that durability, real-world safety, and adoption still need to be proven at scale. The 26-week COMP006 Part B data are expected in early Q3 2026, rolling NDA submission and review are already underway, and final NDA submission remains on track for Q4 2026. With FDA approval, COMP360 could “fit seamlessly” into existing specialty clinics (over 7,300 in U.S.) and even expand the treatment paradigm. Compass is also initiating a late-stage PTSD program and has early-stage exploratory studies (e.g. anorexia nervosa [my specialty :)]). The addressable markets are large and no classic psychedelic therapy is FDA-approved in the U.S., which leaves meaningful upside if COMP360 reaches market and the monitored-care model is reimbursed and adopted.

Financials - Operating Expenses

Compass Pathways has no product revenues yet and has incurred net losses as expected for a development-stage biotech. For FY2025, R&D spend was $118.4M (nearly flat vs $119.0M in 2024) and G&A was $60.6M ($59.2M in 2024). In Q4 2025 alone, R&D was $29.9M (down from $32.1M YoY due to prior reorg) and G&A was $16.0M (vs $16.3M). These expenses reflect the Q4 2024 reorganisation and the termination of certain discovery programs, with spending increasingly focused on the COMP360 TRD program, PTSD, and commercial-readiness work, which provides an insight about rational capital allocation. Core R&D is now focused on the two Phase 3 TRD trials and initiating PTSD, which explains why FY2025 spend held steady.

The net loss widened in 2025, largely due to a non-cash warrant revaluation (not underlying operations). Q4 2025 net loss was $93.9M ($1.00 per ADS) vs $43.3M ($0.63) in Q4 2024. FY2025 net loss was $287.9M ($3.08) vs $155.1M ($2.30) in 2024. In both cases, the increases were primarily driven by large non-cash losses on fair-value adjustments of warrants (-$38M in Q4, -$122.6M for FY). Excluding these accounting items, 2025 operating losses were similar to 2024’s. Notably, Compass had no revenues in either year, which is logical. On a per-share basis, 2025 EPS ($-3.08) obviously reflects this pipeline spending. Using non-GAAP or cash-adjusted measures, the company remains well in the red, in line with most pre-commercial biotechs.

Balance Sheet & Cash Runway

Compass’s balance sheet has materially strengthened since year-end. As of December 31, 2025, the company held $149.6M in cash and cash equivalents against $31.6M of debt. by March 31, 2026, cash had increased to $466.0M, while debt rose more modestly to $50.5M. In simple net-cash terms, Compass moved from roughly $118M at year-end to about $416M at Q1, a major de-risking event ahead of the final COMP360 NDA package and potential commercial launch. The step-change was driven by successful financing and warrant exercises completed during Q1, and, as we mentioned above, management now expects the current cash position to fund operating expenses and capital expenditure requirements into 2028. This matters a lot (and was reflected by the +14% stock gain upon earnings) because Compass is entering its most capital-intensive transition period, i.e. completing the rolling NDA submission, preparing for 26-week COMP006 Part B data in early Q3, targeting final NDA submission in Q4, and building the commercial launch infrastructure around payers, KOLs, HCP education, reimbursement, rescheduling, and treatment-site readiness. The one important caveat that needs to be mentioned from Q1 earnings is that Q1’s reported net income of $91.2M shouldn’t be mistaken for operating profitability, as it was primarily driven by a $130.9M non-cash warrant fair-value gain. The company still posted a $42.9M operating loss. Still, the practical takeaway after Q1 2026 earnings is clearly positive for the company’s financials. Compass has converted a previously adequate runway into a launch-ready balance sheet, materially reducing near-term financing risk through the key regulatory and early-commercialisation window.

Cash Burn & Capital Allocation

As we said, Compass naturally generates no positive operating cash flow. Net cash used in operating activities was $157.2M in 2025, above its earlier $120M-$145M guidance range. Most operating expense is R&D, but G&A is still meaningful - 2025 R&D was $118.4M and G&A was $60.6M, while capex appears minimal. It’s worth to note that since 2022, management has been disciplined in this area. Expenses were trimmed via reorganisations, and in Q4 2025 share-based comps were lower due to leaner staff. With the new funds, management says proceeds will support the ongoing COMP005 and COMP006 Phase 3 trials, the Phase 2b/3 PTSD trial, acceleration of commercial-readiness activities, working capital, and general corporate purposes. No buybacks or dividends exist, again, naturally :). Overall, capital allocation is focused on financing operations. The successful $150M public offering at $8.00 per ADS, including pre-funded warrants at $7.9999 and a 30-day underwriters’ option to purchase up to 2,812,500 additional ADSs, together with warrant exercises, was structured to strengthen the balance sheet rather than return capital to shareholders, which is a sound practice at this stage.

Valuation & Investor Sentiment

At roughly $10.62 per ADS on May 14, 2026, Compass Pathways trades at a market capitalisation of about $1.4B. The valuation picture has changed meaningfully after Q1 2026. With $466.0M of cash and equivalents and $50.5M of debt as of March 31, 2026, Compass carries an estimated enterprise value of roughly $1.0B at a $10.62 share price, depending on whether one uses the company’s March 31 share count or market-data share count. In other words, what this means is the stock has risen, but the balance sheet has improved materially, too, leaving Compass better funded while valuing the pipeline and commercial option at roughly $1B on an EV basis.

Traditional valuation ratios remain largely unhelpful in this case :). Compass is still effectively pre-revenue, so P/S, P/FCF and normalised P/E are virtually meaningless.

Investor sentiment has improved sharply following the Q1 update, which makes us pat ourselves on the shoulder a little bit for investing in the company before this shift :). The shares jumped to a two-year high after the print. Analyst sentiment remains broadly constructive, with consensus price targets generally clustered around the low-$20s (roughly $20–22 per share depending on the source) implying substantial upside from current levels, though with the usual binary regulatory and commercialisation risks attached to a late-stage biotech.

Conclusion

Compass Pathways now has stronger scientific, regulatory, and financial momentum than it did only a few months ago. COMP360 has positive primary-endpoint results from two ongoing Phase 3 TRD trials behind it, the FDA has granted a rolling NDA submission and review request, 26-week COMP006 Part B data are expected in early Q3 2026, and final NDA submission remains on track for Q4 2026. The company was selected for the FDA Commissioner’s National Priority Voucher pilot program, further improving the regulatory setup.

The biggest change (and a positive one) is the balance sheet. Compass ended Q1 2026 with $466.0M in cash, which means the company is now funded through the key NDA, approval-preparation, and early launch-readiness window. Compass is still operationally loss-making, and Q1’s reported net income was mainly driven by a non-cash warrant fair-value gain, not recurring profitability. But, as we explained, that is expected for a late-stage biotech company.

In short, Compass remains a high-risk, high-upside story, but the risk has shifted. The central question is no longer whether the company has enough cash to fund the expected NDA and launch-preparation window.

Management Quality and Insider Activity

Management quality looks better than the stock multiple might imply. Kabir Nath has been CEO and a board member since August 2022, after holding senior leadership roles at Otsuka, including senior managing director of global pharmaceuticals and president and CEO of Otsuka’s North America Pharmaceutical Business. Guy Goodwin has served as CMO since August 2021 and is Emeritus Professor of Psychiatry at the University of Oxford. Teri Loxam became CFO in March 2024, after consulting for the company from December 2023, and brought prior biotech CFO/COO experience as well as investor-relations experience from Merck, IMAX, and Bristol-Myers Squibb. Board chair Gino Santini, who has served as Chair since September 2024, brings decades of large-pharma and public-company board experience, including senior roles at Eli Lilly and board roles at Collegium, Horizon, Intercept, Allena, and AMAG. During 2025, the board held 10 meetings and all then-serving directors attended at least 75% of the aggregate board and committee meetings on which they served. That’s not conclusive evidence of excellence, but it is surely consistent with a serious, commercially minded leadership bench backed by experienced operators rather than a founder-led science experiment.

Insider alignment is decent but not especially exceptional. As of April 6, 2026, current executive officers, directors, and nominees as a group beneficially owned 4.0 million ordinary shares, or 2.82% of the company, but that figure includes 1.72 million shares underlying options exercisable within 60 days. Actual ADSs/shares held by the group were about 2.28 million. Individually, the proxy lists beneficial ownership of 1.02 million shares for Kabir Nath, 121,802 for Teri Loxam, 300,244 for Guy Goodwin, and 1.72 million for director Robert McQuade. McQuade’s figure mostly reflects 1.59 million ADSs held by the McQuade Center for Strategic Research and Development LLC, over which Dr. McQuade may be deemed to have voting and investment power while disclaiming beneficial ownership of those shares. The proxy also says all reporting persons complied with applicable Section 16 filing requirements during 2025. That is respectable alignment, but it is not founder-style ownership concentration.

On recent insider activity, the filings we reviewed for Nath, Goodwin, and Loxam show that 2026 activity has mainly been compensation-related or tax-withholding related. The recent filings show RSU and option grants for the CEO and CFO, option grants for the CMO, and tax-withholding dispositions on RSU vesting for the CFO. We did not see a discretionary open-market insider-buy signal in the recent Form 4s we reviewed. The activity appears to be grants, option awards, and tax-withholding dispositions rather than executives putting fresh personal cash into the market. That's notable because, at this stage, we would prefer to see at least one meaningful open-market purchase after the scientific and financial de-risking and after the February financing, especially if management believes the commercial gap versus peers is overstated.

Overall, we would still rate management as above average for a single-asset biotech. The team has raised capital when needed, solidified the balance sheet to a truly respectable level exactly when it mattered, accelerated launch readiness after positive FDA interactions, and moved the company from Phase 2b promise to a near-filing posture. What it has not yet proven is late-stage commercialisation under operational constraints. And that, especially for management, remains the real exam.. The main question is whether COMP360 can win approval, secure reimbursement, and scale through a controlled treatment-site model. If Compass executes, today’s enterprise value could prove conservative. If approval or commercial adoption disappoints, the downside remains substantial. That’s why this is still a high risk / high reward story. We like it, though, especially after the Q1 print.

Risk Factors

Let’s not sugarcoat it, a company in this field, at this stage, has more than enough risks, including the inherent uncertainty of drug development (including FDA review and DEA scheduling for a controlled substance), and the challenges of creating a new treatment paradigm (therapist training, treatment centres, payer acceptance). Le’ts lay them out.

Capital and cash-burn risk

Compass remains unprofitable and has no product revenue, meaning its business still depends on cash reserves and access to external capital until COMP360 is approved and commercially launched. Operating expenses remain substantial. In Q1 2026, the company reported $42.9M in operating expenses, including $26.5M in R&D and $16.4M in G&A, as it continues NDA preparation, launch-readiness work, site-of-care training, payer engagement, and pipeline development.

That said, near-term financing risk has materially improved through Q1 2026 and management now expects to fund operations and capital expenditures into 2028. as we mentioned previously, this should cover the key NDA, regulatory, launch-preparation, and early commercialisation period. The risk, therefore, has shifted from immediate survival funding to longer-term execution risk. If approval is delayed, reimbursement is slower than expected, launch costs are higher, or adoption disappoints, Compass may still need to raise additional capital. Future equity raises could dilute shareholders, especially if market sentiment weakens after regulatory or commercial setbacks.

Possible mitigation: The company has significantly reduced near-term dilution pressure by strengthening its balance sheet before the most important regulatory milestones. The runway into 2028 gives management flexibility to complete the NDA process, prepare launch infrastructure, and negotiate from a stronger position. Continued positive regulatory progress could also improve access to capital if further financing is eventually needed.

Clinical development and FDA approval risk

Compass’s fate hinges on successful development and approval of COMP360.Compass has already reported positive primary-endpoint results from both Phase 3 TRD trials, COMP005 and COMP006, but COMP006 26-week Part B data are still expected in early Q3 2026, and the FDA must still accept, review, and approve the NDA. This is the single biggest risk in the entire thesis and no assurance of success exists – as the company notes, it:

“cannot give any assurance that COMP360 will successfully complete clinical trials or receive regulatory approval”.

Clinical trials are inherently unpredictable and expensive, and delays or failures in ongoing studies (or future trials in PTSD or other indications) could derail the program. Even with positive Phase 3 toplines (COMP005 in June 2025 and COMP006 in February 2026), any unexpected safety signals, assay errors, or regulatory questions (e.g. demands for additional studies) could postpone approval or require study repeats. The company’s 10-K emphasises that lengthy or delayed trials could render regulatory approval unobtainable on schedule or at all, which “will adversely affect our business”.

Possible mitigation: Compass has FDA Breakthrough Therapy designation for COMP360 in TRD, and FDA has now granted rolling NDA submission and review, with rolling submission already underway. Robust positive results from its Phase 3 TRD trials (announced Feb 2026) reduce, but don’t eliminate, approval risk. The company is engaging proactively with regulators: FDA has granted rolling NDA submission and review, selected COMP360 for the Commissioner’s National Priority Voucher pilot program, and Compass says final NDA submission remains on track for Q4 2026. These steps may reduce regulatory uncertainty, but they do not eliminate the need for FDA approval and DEA scheduling or rescheduling before commercial marketing.

Controlled-substance classification and public perception risk

COMP360 contains psilocybin, a controlled psychedelic. This introduces an extra layer of regulatory and social risk beyond a typical drug. Regulators (e.g. FDA, DEA) will not only review safety/efficacy but also evaluate abuse potential. The 10-K warns that during FDA review “the FDA may require additional data” on abuse/misuse potential, which could delay approval or any subsequent drug re-scheduling. In the U.S., DEA scheduling decisions are needed before a commercial launch. If psilocybin is placed in a strict schedule, access and prescribing might be tightly limited or require special licensing, potentially shrinking the market. In addition, psilocybin’s historical stigma could affect uptake. Compass itself notes that public controversy or adverse publicity around its compound or psychedelic treatments “may negatively influence the success” of its therapy.

Possible mitigation: Compass is working with regulatory and medical stakeholders to demystify the therapy. Its pre-approval programs in Europe and FDA meetings may allow coordination with DEA on scheduling. The company and its academic collaborators publish and educate about psilocybin’s safety profile. Moreover, positive clinical data (e.g. peer-reviewed Phase 2b results in NEJM - The New England Journal of Medicine) help build credibility. Over time, mounting clinical evidence and changing laws (e.g. expanded medical-use laws for psychedelics) may reduce scheduling barriers and stigma, mitigating this risk. The U.S. government favourable approach also appears to be a good sign in this matter.

Market access, infrastructure and reimbursement risk

Even if COMP360 is approved, its commercial success is not guaranteed. The drug cannot simply be written at a pharmacy. It must be administered in a supervised setting with psychological support, and commercialisation requires building a novel delivery network. The company emphasises that it has “never commercialized a therapeutic candidate before” and “may lack the necessary expertise, personnel and resources to successfully commercialise” COMP360. Success also depends on market acceptance. Future sales will hinge on market access and acceptance of COMP360 among healthcare professionals, patients, and payors. Insurers and health systems may balk at covering a multi-hour treatment with a new controlled drug. Furthermore, the model requires scaling qualified therapists and treatment centres. The company’s 10-K warns that its strategy “depends on [its] ability to identify, qualify, prepare, and support third-party treatment centers”, and that failure to build this network would materially harm the business. In short, obstacles in distribution logistics, provider training or insurance reimbursement could severely limit uptake.

Possible mitigation: Compass is already investing in commercialisation infrastructure, including healthcare-provider education, site-of-care readiness, payer engagement, and digital support tools such as myPathfinder, but the commercial delivery model still needs to be proven at scale. The company has engaged health technology assessment bodies (Compass notes an “Innovative Licensing” designation in the UK) and may pursue outcomes-based pricing. These steps, along with a growing number of specialised psychedelic clinics, could ease adoption. However, significant execution risk remains in coordinating all these pieces.

Competition and alternative therapies risk

Compass operates in a competitive field. Other companies and organisations (including AtaiBeckley, Definium Therapeutics, GH Research, Usona Institute, Helus Pharma, and Resilient Pharmaceuticals/Lykos, formerly MAPS Public Benefit Corporation) are developing psychedelic or adjacent neuropsychiatric therapies (for TRD, PTSD, etc.), and traditional TRD treatments (such as ketamine/esketamine, SSRIs, neuromodulation devices) are well-entrenched. As the 10-K rather bluntly states, Compass “faces substantial competition” and rivals may bring therapies to market sooner or more successfully, potentially “reducing or eliminating” Compass’s commercial opportunities. If a competitor’s treatment gains first-mover advantage, insurers and doctors may prefer it, making COMP360’s uptake harder. Further, generic or alternative novel treatments (non-psychedelic) for depression or PTSD may also capture market share once COMP360 is approved.

Possible mitigation: COMP360’s positive Phase 3 primary-endpoint data, rapid onset, and six-month durability in COMP005 responders could differentiate it from peers, while COMP006 26-week durability data remain pending. The company is also pursuing multiple indications (e.g. PTSD, anorexia) to broaden its pipeline. Strategic partnerships or licensing could help shore up expertise (the company’s collaborations with academic centres and a broad IP portfolio can provide some defense). Ultimately, time-to-market and real-world outcomes will determine advantage. For now, investors should recognise and fully realise that any successful competitor could limit COMP360’s pricing power and uptake.

Intellectual property and patent risk

Compass’s value depends on protecting its science. The company relies on patents and trade secrets to shield COMP360 and associated methods (manufacturing, dosing protocols, digital support tools). However, patent protection for psilocybin therapies is inherently uncertain and time-limited. The 10-K warns that failure to obtain or maintain “adequate patent” coverage could “materially adversely affect” Compass’s ability to market COMP360. Pending patents might not be granted or could be challenged (some granted patents have already faced post-grant reviews). Competitors might work around patents or invoke compulsory licensing. Notably, many key COMP360 patents, including method-of-use, crystalline psilocybin, formulation, and manufacturing patents, have estimated expirations around 2037–2042. After expiry or successful challenge, competing synthetic psilocybin products could become easier to market, subject to regulatory requirements.

Possible mitigation: Compass has built a broad IP portfolio (covering psilocybin formulations, uses, manufacturing) which may deter some competition. It can also seek to extend exclusivity through new formulations or new indications. In the near term, the lack of effective alternatives in TRD means Compass has some lead time before generics arrive. Nevertheless, IP is a critical risk area in the broad sense. The company notes that enforcing IP rights is costly and uncertain, so we as investors should definitely monitor patent litigation or challenges as future risk factors.

Third-party manufacturing and trial execution risk

As a virtual pharma, Compass depends on outside firms to make its drug and run trials. The 10-K cautions that the company “relies on third parties to supply and manufacture” COMP360, and if a contract manufacturer fails or loses regulatory compliance, “development could be stopped, delayed or made commercially unviable”. Currently, a single supplier provides COMP360’s API (active ingredient), so any hiccup (e.g. quality issue, plant inspection failure) could disrupt production. Similarly, many clinical trials (including investigator-initiated studies) are run by external sites. If third-party researchers “raise concerns” in data or mishandle trials, Compass’s regulatory approval could be impaired.

Possible mitigation: Compass reports having identified backup suppliers and maintains inventory to mitigate API outages. It conducts due diligence on contract manufacturers (all cGMP-compliant) and drug supply is closely monitored. For clinical sites, the company continues to oversee trial conduct and has the option to terminate non-performing sites. In practice, the recent Phase 3 trials appear well-run (nearly 30 sites across US/EU), suggesting execution risk here is manageable. Still, any supply-chain or trial execution failures would significantly delay approval or launch.

Cybersecurity and international operations risk

Compass’s operations span the UK, US and other jurisdictions, and it collects sensitive patient data. The 10-K flags risks typical of global biotech, i.e. exchange-rate fluctuations could slightly affect results, and data breaches or cyberattacks could disrupt business. While not the top risk, a major IT failure or hack of patient information (e.g. trial data) could harm the company’s reputation and incur costs.

Possible mitigation: The company maintains standard cybersecurity measures and insurance. As it scales, it is likely to invest further in compliance and IT infrastructure. Internationally, Compass’s U.K. headquarters, U.S. Nasdaq listing, and cross-border regulatory / commercial strategy give it some geographic flexibility, but they do not meaningfully eliminate capital-market or execution risk.

Risk Map

Our Scenarios (3-5 Year Horizon): Bull, Base, Bear Case

Please note that the ranges below are our estimates, not company guidance. They are anchored to management’s expectation of final NDA submission in Q4 2026, cash runway into 2028, a U.S. TRD population measured in the millions, and the practical reality that COMP360 is expected to require certified sites, trained healthcare professionals, and at least six hours of post-dose monitoring.

Bull Case (30% Probability)

Key Assumptions

The company completes the final NDA submission on time, benefits from rolling NDA submission / review and the FDA Commissioner’s National Priority Voucher pilot program, and wins approval in 2027, and converts its current launch-readiness work into a fast site rollout and acceptable payer access. Clinicians buy into the argument that rapid response and durability after one or two doses can offset the operational burden, and the remaining COMP006 26-week follow-up strengthens the label narrative instead of weakening it.

Financial Outcomes

Our estimate is that revenue could reach roughly $750 million to $1.2B by 2030 if uptake is strong in certified sites, reimbursement is workable, and the company does not lose too much ground to shorter-duration competitors. In that case, the business likely avoids another major dilutive raise after launch and earns the right to fund adjacent indications internally. Our rough valuation logic in this case is 4.5-6.0x sales, limited dilution and successful launch re-rating with stock price of $30-55 (+182.5% to +417.9% upside from current levels).

Base Case (45% Probability)

Key Assumptions

Approval still happens, but commercialisation is slower than biotech bulls want. REMS, certification, staffing, and reimbursement friction constrain early uptake. The product works, the science holds, and the company launches, but the real-world rollout ends up looking more like a careful specialty build than a rapid category land-grab. Meanwhile, competitors with shorter clinic times keep investors from assigning a premium multiple.

Financial Outcomes

In this case, our estimate is that 2030 revenue lands more in the $250 million to $500 million range. That would still validate the franchise and likely support a meaningfully higher valuation than today, but it could also require at least one more financing event before the company reaches self-sustaining cash generation, especially if it continues to invest in PTSD and broader pipeline work. We’d assume roughly 3.5-5.0x sales, slower rollout, and some dilution/continued investment, implying a broad stock-price range of roughly $14-25 per share (+31.8% to +135.4% from $10.62), although the low end of that price range assumes either meaningful remaining net cash, a better-than-minimum revenue outcome, or a higher market multiple.

Bear Case (25% Probability)

Key Assumptions

The biggest risk is not that COMP360 suddenly “stops working.” The bigger risk is that durability, safety follow-up, label restrictions, site economics, or reimbursement prove less favorable than hoped. A regulatory delay or additional-study requirement would be especially painful because the company is still pre-revenue, and a slower path would give shorter-duration rivals more time to narrow the convenience gap before launch.

Financial Outcomes

In this case, our estimate is for little to modest commercial revenue by 2030, likely below $100 million, alongside further dilution or strategic alternatives. The equity would then behave more like a perpetually financed development story than a future specialty-CNS franchise. With delayed or limited launch, ongoing dilution, continued cash burn, and only strategic optionality, we’d assume a stock price of $3-8 per share, or roughly -72% to -25% downside from $10.62.

Moat Resilience Index™ (MRI)

Moat Strength: 7/10

The company has earned this rating through regulatory lead, repeated controlled efficacy signals, a broad IP estate, and visible launch-readiness work. That is enough to say the moat exists. It is not enough to say it is dominant, though.

Moat Hate: 6/10

The market has repeatedly treated the shares as if pivotal success alone may not be enough. The June 2025 selloff after a primary-endpoint win, the equity financing immediately after the February 2026 clinical pop, and still-notable short interest all show a market that remains suspicious of the commercial story even as the science improves. That is exactly the kind of setup a hated-moats framework is looking for and before Q1 2026 results, we’d rate Moat Hate 7.5 or even 8 out of 10. The strengthened balance sheet in Q1 has clearly improved this metric, but valid scepticism remains present.

Moat Vulnerability: 7/10

The vulnerability is operational really, not primarily scientific. Six-hour monitoring, third-party site dependence, expected REMS restrictions, clinician-training bottlenecks, and competition from shorter-duration or no-psychotherapy models make the moat attackable. If someone else can deliver similar outcomes with much better clinic throughput, that matters enormously and Compass’s commercial model could be materially impaired.

Hated Moats Outperformance Score™ (HMOS): 65%

On our read, the stock has enough real moat and enough real market scepticism to create asymmetric upside, but it doesn’t yet have enough commercial proof to deserve a truly elite score. This is a high-potential bet, not a finished classic moat fortress that’s currently hated.

Conclusion

Compass Pathways has moved well beyond the stage of being merely an “interesting psychedelic science” story. With positive primary-endpoint results from two ongoing Phase 3 studies, rolling NDA submission and review underway, and selection for the FDA Commissioner’s National Priority Voucher pilot program, the company now has a regulatory lead that peers currently do not have. That lead matters.

However, the investment case is still not simple. COMP360 may be closest to turning psychedelic psychiatry from clinical possibility into reimbursable clinical reality, but the treatment model remains operationally heavy. Certified sites, trained healthcare professionals, monitoring time, payer acceptance, DEA scheduling, and real-world clinic economics all still matter. In this field, the eventual winner may not simply be the company that proves efficacy first and “paves the path”. It may be the company that makes the care model easiest for clinics, payers, and patients to adopt.

That is why the market is not ignoring the science. It is discounting the scalability. Compass currently leads on timing, regulatory momentum, and maturity of evidence. However, it does not (yet) clearly lead on convenience. The shares therefore look like an attractive moat-being-built candidate, not a completed moat compounder.

The main unresolved issues are the remaining COMP006 26-week durability and follow-up data, the exact shape of the eventual label and access restrictions, and whether site economics work cleanly at scale. If those pieces fall into place, today’s valuation could look too conservative. If they do not, the stock still has meaningful downside despite the improved balance sheet.

Final Verdict

Our verdict is Buy, but not Strong Buy. Compass offers one of the most compelling risk/reward setups in late-stage neuropsychiatry because the company combines real Phase 3 progress, regulatory momentum, a strengthened balance sheet, and a still-sceptical market. But the unresolved commercial and operational risks are too large to justify a top-tier conviction rating. This is a high-risk, high-upside, small-allocation Buy, and it's attractive for investors comfortable with biotech volatility, regulatory uncertainty, and the possibility that approval may not automatically translate into broad adoption.

Disclaimer & Our Investment

At the time of publishing, the author of this article does hold a position in the security of Compass Pathways plc., at average price of $9.66 per share, which accounts for 1.35% weight of his private stock portfolio. This report is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

Wonderful work my friend!