Quick Summary & Investment Thesis

Key Investment Drivers

Core razor-and-blade engine. Installed base growth + sticky, high-margin disposable sensors. Long hospital contracts underpin visibility (multi-year backlog ~$1.76bn).

Margin expansion from focus. Exit/divest Sound United. Mix shift back to healthcare lifts gross margin (~63%) and adj. operating margin towards 28–30% (guiding ~27% for 2025).

Operating leverage & EPS trajectory. 2025 non-GAAP EPS $5.20–$5.45 (+~25–30% y/y) with scope to compound mid-teens in the base case as opex grows slower than revenue.

Deleveraging & cleaner FCF. Potential Sound United sale proceeds to reduce ~$642m debt. Capex <3% of sales, 2025 FCF outlook $275–315m (forward FCF yield ~4–5%).

Product/portfolio execution. Incremental innovation on Root platform and rainbow® parameters. Commercial lift in capnography/EEG; better pricing/contracting discipline.

Improved governance & alignment. New board/management cadence; insider/institutional ownership high; recent insider buy after a dip signals confidence.

Valuation re-rating potential. Trading below peak multiples and some peers on EV/Sales and P/E; sustained delivery could move shares toward $200–235 in 3–5 years (base).

Primary Risks

Competitive & tech disruption. Medtronic pricing pressure, Big Tech health features (e.g., Apple) designing around IP could nibble at the moat over time.

Legal/regulatory overhangs. Ongoing Apple/ITC/Customs disputes. Any adverse rulings or costly compliance could dent margins and sentiment.

Divestiture execution. A delayed/weak Sound United sale would slow deleveraging and distract management.

Customer concentration & GPOs. One major distributor (~18% of healthcare revenue) and GPO pricing pressure can squeeze margins.

Macro & hospital spending. Recessionary or budget-tight periods can delay capital equipment cycles (though disposables are resilient).

Supply chain & tariffs. Mexico-sourced manufacturing and geopolitics may add cost/complexity.

Personnel/culture & expectations. Post-leadership change execution risk; “show-me” market may punish even good quarters if not “good enough.”

Hated Moats Verdict

Rating: BUY (Moderate/Outperform).

Attractive entry for quality at a reasonable price. Not “table-pounding cheap,” but improving fundamentals and catalysts (Sound United sale, sustained beats/raises, possible legal resolution) support upside skew.

Add-levels: ‘Confident Buy’ <$138; ‘Strong Buy’ <$120.

The Deep Dive

Overview & Positioning

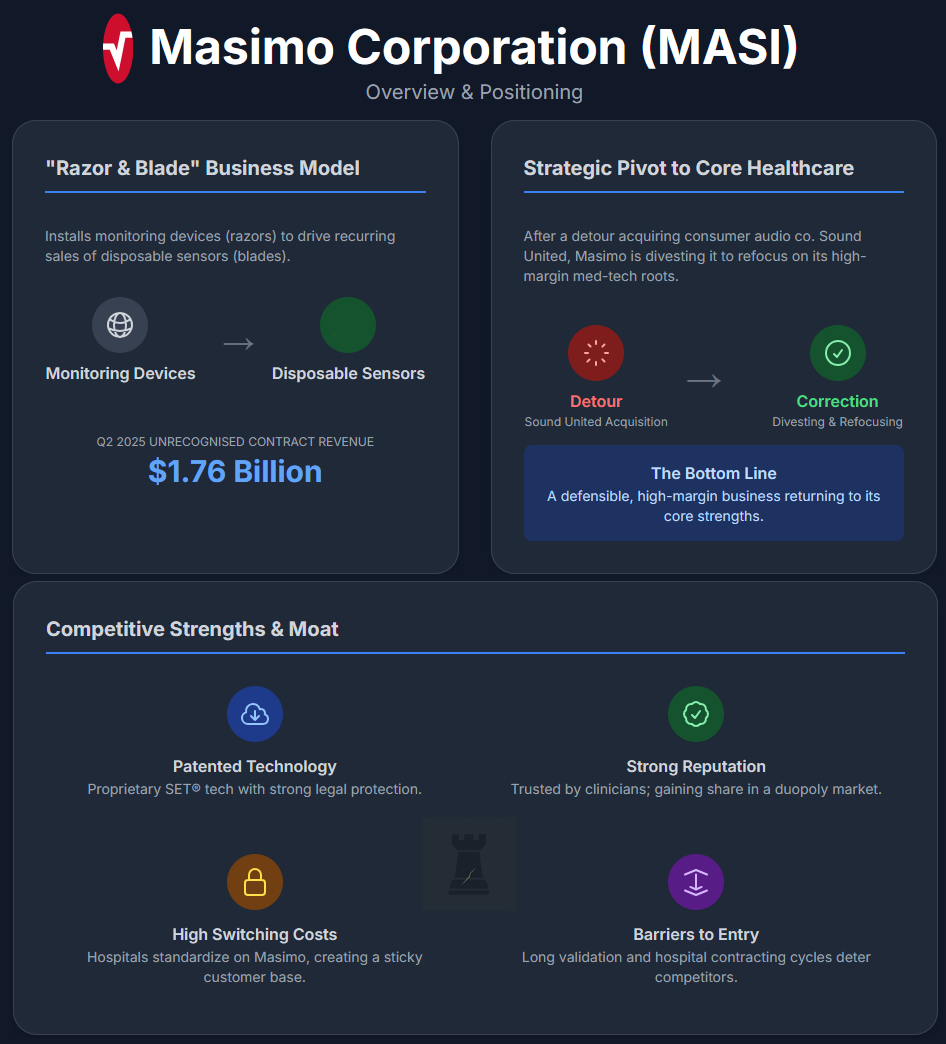

Masimo is a medical technology company renowned for its "gold standard" Signal Extraction Technology (SET®) pulse oximetry used in hospitals. The company operates a highly effective "razor-and-blade" business model. It installs its monitoring devices and then generates steady, recurring revenue from the sale of disposable sensors. This has created a loyal customer base and a substantial unrecognised contract revenue backlog of approximately $1.76 billion as of Q2 2025.

However, the company took a strategic detour in 2022 by acquiring consumer audio company Sound United for about $1 billion. The move was poorly received by investors, loaded the company with debt, and added a lower-margin business with declining sales. Under activist pressure, Masimo is now divesting Sound United to refocus entirely on its core healthcare business and return to its roots as a pure-play med-tech firm.

Competitive Moat

Masimo's wide competitive moat is built on several key factors. It possesses a deep portfolio of proprietary, patented technology (a major legal victory against Apple in 2023 but currently back in a situation where the battle has evolved from a patent infringement case into a fight over regulatory enforcement and administrative law), a strong brand reputation among clinicians for reliability, and high switching costs for hospitals that have standardised on its systems. In its core market, Masimo operates in a duopoly with Medtronic and has been steadily gaining market share.

The barriers to entry for competitors are formidable, requiring extensive clinical validation and long hospital contracting cycles. Masimo continually widens its moat by innovating and bundling more value into its platform, adding new measurements like total hemoglobin and brain function monitoring. Ultimately, Masimo is a critical-care technology provider with a defensible, high-margin consumables business.

Recent Stock Performance & Market Sentiment

Masimo’s stock has endured a roller-coaster ride. After peaking above $300 in late 2021, it began a steep descent following the poorly received Sound United acquisition and subsequent earnings volatility. The stock ultimately bottomed out in the mid-$70s in October/November 2023, a stunning ~75% collapse from its highs. This crash reflected the market’s harsh verdict on the company's non-core foray, a sharp drop in earnings, and the impact of rising interest rates.

The inflection point came in 2023–2024 with a high-profile activist campaign by Politan Capital Management. Politan waged a two-year campaign that culminated in shareholders ousting founder Joe Kiani from the board in September 2024, he subsequently resigned as CEO. The board was reconstituted with Politan nominees. The market reacted positively to these governance changes, with the stock rallying ~40% in 2024. The new leadership, including CEO Catherine Szyman (an industry veteran from Becton Dickinson), has pivoted back to the core healthcare business and initiated a strategic review to sell the consumer segment. This has turned Masimo into a turnaround story, with the stock climbing back to the mid-$100s and hitting a 52-week high of ~$195 before recently settling around ~$140-145.

Current market sentiment is cautiously optimistic but mixed. On the bullish side, most sell-side analysts rate the stock a Buy, with an average price target around $195 and some targets as high as $210. This confidence is echoed by a recent insider share purchase by a Politan-backed director. However, skepticism lingers. Short interest remains notable at 6-7% of the float, and the stock's reaction to good news has been tepid. For instance, after a strong Q2 2025 earnings beat, the stock dropped ~12% as Wall Street expressed concern that the new strategy sounded too "incremental" and might not deliver dramatic growth.

This indicates the market is now in "show me" mode. After the initial turnaround euphoria, expectations have risen. Trading around ~$145, the stock is no longer "hated" per se, but the company must now translate its potential for margin expansion and new product wins into sustained earnings growth to earn back a premium valuation.

Fundamental Analysis

Growth & Profitability

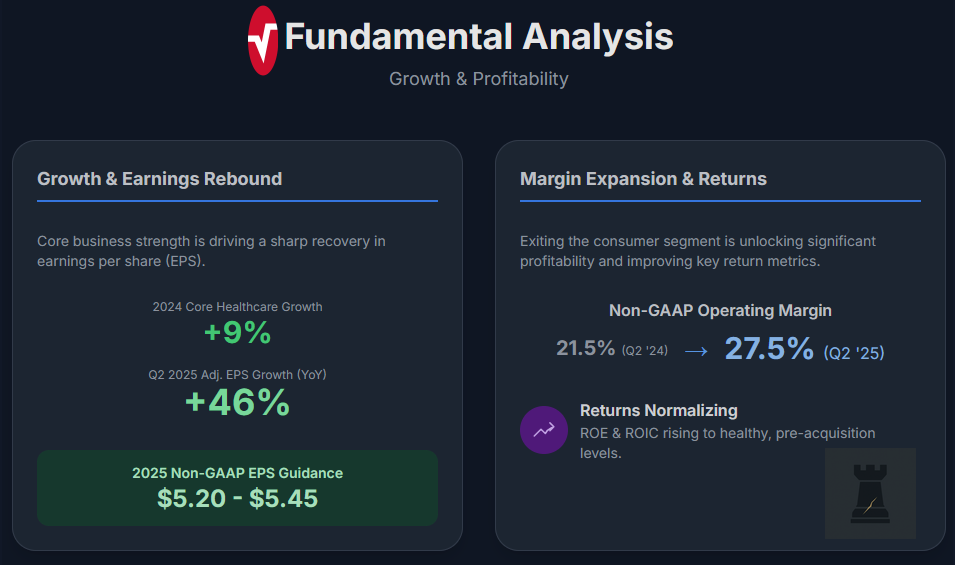

Masimo’s core healthcare business remains strong, with its revenue growing +9% in 2024. This performance was masked by a -10% decline in the consumer segment, which limited total company growth to just +2%. The healthcare division's strength is confirmed by Q2 2025 results, which showed healthy year-over-year increases in both instrument shipments and consumable revenues.

For fiscal year 2025, the company guides for $1.50–$1.53 billion in healthcare revenue, representing +8–11% constant-currency growth. While total reported revenue will appear to shrink due to the Sound United divestiture, opportunities exist to accelerate growth in areas like capnography through better commercial execution. Analyst estimates currently seem conservative, factoring in the divestiture. A reasonable base-case assumption is for mid-single-digit organic growth, driven by continued hospital adoption and new product introductions.

As far as profitability goes, Masimo is demonstrating a strong rebound. The 2024 headline GAAP net loss of -$305 million was misleading, as it was caused by a large, non-cash impairment charge on Sound United. Excluding this, 2024 non-GAAP EPS was actually $4.40, a +16% increase from the prior year. This recovery accelerated sharply in 2025, with Q2 adjusted EPS soaring +46% year-over-year to $1.33, driven by significant margin expansion.

The key driver is operating leverage. In Q2, non-GAAP gross margin climbed to 62.9%, while operating expenses remained nearly flat even as revenue grew. This caused the non-GAAP operating margin to jump 600 basis points to 27.5%, up from 21.5% a year ago. For the full year 2025, Masimo guides for a ~27% adjusted operating margin, a substantial improvement from ~22% in 2024, as it exits the low-margin consumer business. This highlights the attractive profitability of the core business, where top-line growth can drive outsized profit increases.

Masimo’s bottom-line earnings are set to normalise at solid levels. The company expects $5.20–$5.45 in non-GAAP EPS for 2025, which represents ~25–30% growth over 2024 on a comparable basis. While GAAP EPS will be lower (around $4.10 consensus) due to amortisation and other charges, the overall trajectory is clearly upward.

Key return metrics are also improving. Underlying Return on Equity (ROE) is healthy and likely to normalise in the high-teens to 20% range, consistent with pre-acquisition levels. Similarly, Return on Invested Capital (ROIC), recently low due to depressed earnings, is expected to rise substantially as profits grow and the company de-leverages. In summary, Masimo's profitability profile is strong and improving, with gross margins over 60% and operating margins in the mid-20s. The erratic earnings of recent years were due to non-recurring charges, and the core business's underlying earnings power is now returning.

Free Cash Flow & Capital Allocation

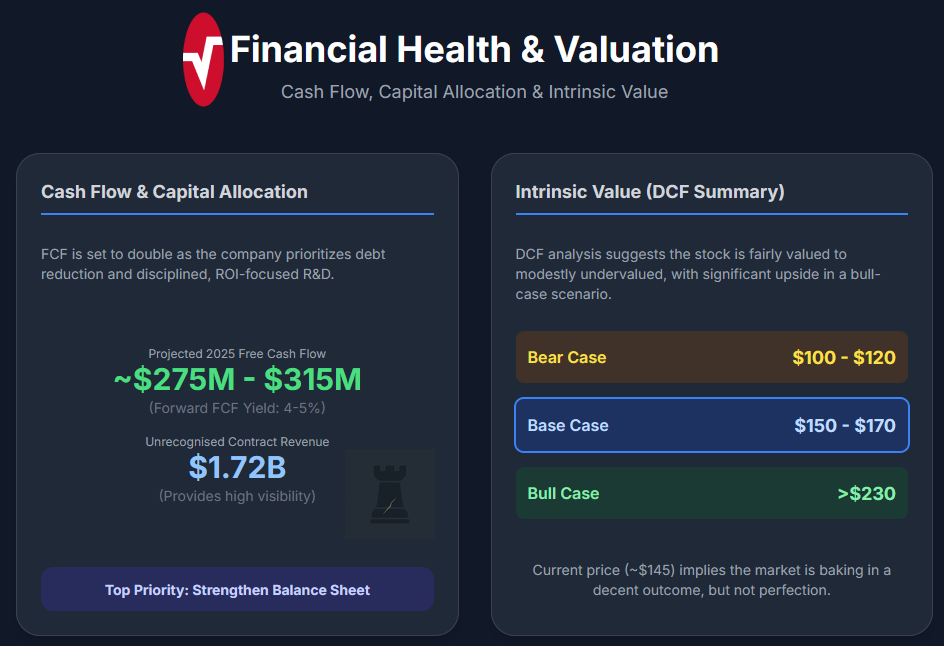

Masimo generates solid free cash flow (FCF), although it dipped during its recent transition. Over the last 12 months, FCF was ~$160 million, equating to a modest ~2% FCF yield that reflects a recent earnings trough. However, FCF is expected to rise significantly going forward. With minimal capex needs (less than 3% of sales), as net income rebounds, annual FCF could move into the ~$250M+ range. For 2025, projections indicate Masimo could generate ~$275–$315 million in FCF, roughly double the trailing twelve-month figure. This implies a more reasonable forward FCF yield in the 4–5% range. The company’s cash conversion is decent, and its working capital is in good shape with a current ratio of ~2.1.

As far as capital allocation goes, it’s a key focus under the new, more shareholder-friendly regime, a sharp contrast to the previous era's large, non-core acquisitions. The top priority is monetising assets like Sound United to strengthen the balance sheet. A sale is reportedly on track and it would allow Masimo to wipe out a large portion of its $642 million in total debt. The company’s current leverage (debt-to-equity of ~0.62) is higher than its historically debt-free status, and management is committed to swift deleveraging post-divestiture. Masimo does not pay a dividend, and significant share buybacks are unlikely until leverage comes down. Internal investment, particularly R&D, will now be more disciplined and ROI-focused, concentrating on high-return projects with clear hospital demand rather than speculative consumer ventures.

A hidden strength in Masimo’s financial profile is its $1.72 billion in unrecognised contract revenue from multi-year sensor agreements with hospitals. This significant backlog provides excellent visibility and lowers risk in cash flow projections. Overall, Masimo’s cash flow profile is poised to improve markedly with higher earnings and the shedding of its cash-draining consumer division. Capital allocation is now aligned with shareholder interests, prioritising core business growth and debt paydown. Strong insider alignment (evidenced by significant ownership and a recent board member's open-market share purchase after a stock dip) suggests confidence that management will deploy cash to enhance shareholder value.

Valuation & Key Financial Metrics

Intrinsic Value & DCF

To estimate Masimo’s intrinsic value, we perform a discounted cash flow (DCF) analysis focused on the core healthcare business. We base our model on the updated 2025 guidance and then project cash flows over a 5-year horizon, followed by a terminal value. Our key assumptions in the base case DCF are:

1.) Revenue grows at ~8% CAGR from 2025 to 2030 (starting from ~$1.52 B in 2025 to ~$2.25 B by 2030). This reflects mid-single-digit organic growth plus a slight boost from new products or share gains – essentially assuming Masimo can maintain its recent pace but not dramatically accelerate, which we deem as fair.

2.) Adjusted operating margin expands to ~30% by 2027 and stays around that level, as cost efficiencies and scale offset any pricing pressures. That yields operating income growing faster than revenue (low double-digit CAGR).

3.) After the sale of Sound United, Masimo becomes a pure med-tech play with a normalised tax rate ~21–22%. Depreciation and amortisation add back a bit to cash flow (though amortisation will diminish after the Sound intangibles roll-off).

4.) Capital expenditures remain low (~$20–30M annually) and working capital needs are moderate (we assume a slight use of cash as the business grows, given inventory and receivables growth, but partly offset by advance contract payments).

Using a discount rate (WACC) of ~9% (Masimo has virtually all equity financing post-divestiture, a beta ~1.2, and we assume a mid-single-digit equity risk premium – appropriate for a stable med-tech with some growth prospects), and a terminal growth rate of 2.5% (modest GDP-like growth beyond year 5), we derive the present value of future cash flows.

The result

Our DCF estimates Masimo’s intrinsic equity value in the mid-to-high $100s per share. Specifically, the PV of 5-year free cash flows is on the order of $1.2–1.4 B, and the terminal value (based on ~13× EBITDA or ~18× P/E in 2030, consistent with 2.5% growth, 9% discount) comes in around $7–8 B PV. Summing these and adjusting for net debt (~$0.5B now, likely much less after asset sale), yields an equity value around $8 B to $9 B. On ~54M shares, that’s roughly $150–$170 per share as a base-case DCF valuation. This aligns reasonably well with the current market price – in other words, the stock is trading near our DCF midpoint, implying it’s near fair value but modestly undervalued (9% below the ~$160 midpoint) under status quo assumptions.

However, Masimo’s intrinsic value is quite sensitive to growth and margin assumptions. We also analyse a bull-case DCF scenario: assume revenue growth can average 10%+ (perhaps via a breakthrough product or faster international expansion) and operating margins reach ~33% (approaching the upper-end for med-tech, through efficiencies and mix). In that scenario, 5-year CAGR in EPS might be ~18–20%, and the terminal value (using a still modest terminal growth ~3%) would be much higher. Our bull DCF indicates a valuation north of $230 per share. Conversely, a bear-case DCF might have revenue growth slump to ~4% (if competition intensifies or macro headwinds hit hospital capital spending) and margins stall out ~25%. That scenario yields a value in the ~$100–120 per share range. It’s worth noting that the current price around $145 does not seem to reflect the bull scenario (which would justify far higher), but is above the pure bear scenario. This suggests the market is baking in a decent outcome but not perfection.

In summary, our intrinsic value assessment finds Masimo approximately fairly valued to modestly undervalued at current levels, with an intrinsic value roughly in the $150–170 range per share in our base case. The stock’s margin of safety isn’t huge after the recent rebound. It’s not the deeply undervalued $110 stock it was at the depths, but there is still upside if management executes and de-risks the story. Meanwhile, the downside appears buffered by the strong cash flows and defensiveness of the core business. Overall, the DCF supports a view that Masimo is a solid long-term investment at the current price, albeit one that needs a catalyst (such as demonstrating faster growth or successfully selling the consumer unit) to unlock its higher intrinsic value. We will refine these scenarios in one of the next sections on explicit bull/base/bear cases.

Key Financial Metrics

At ~$145 per share, Masimo’s forward Price/Earnings ratio is 26–27× on 2025 consensus EPS. This is higher than the S&P 500 (~19×) but below the company's historical 30–40× multiple. On non-GAAP EPS guidance of ~$5.30, the forward P/E drops to ~24–25×, which looks attractive given ~24–30% expected EPS growth. This implies a PEG ratio of <1× on near-term growth, or ~2× based on a longer-term ~12% growth rate, suggesting fair value around a ~1.5 PEG.

The Price/Sales ratio is ~3.7× on trailing revenue, or ~5.3× on ~$1.5B in continuing operations revenue. This valuation represents a discount to peer Edwards Lifesciences (8× sales, 28× forward earnings) and is similar to diversified med-techs like Stryker (~5× sales, 20–25× earnings). The Price/Book ratio is 7.7×, while Price to tangible book is ~9×.

Masimo’s enterprise value is $8.4B. Its trailing EV/EBITDA of ~55× is high due to depressed earnings but should normalise to a more reasonable ~18–20× as EBITDA rebounds to ~$420M. EV/Sales is ~3.9× (total) or ~5.5× (core), and EV/Gross Profit is ~8.0× on a ~60% gross margin profile. The FCF yield is ~2% trailing but could reach ~4% (25× P/FCF) based on 2025 projections. Currently, the company is valued at 5.6× continuing sales and ~20× continuing operating earnings.

Wall Street’s average price target of ~$194 implies a re-rating to a ~36× forward P/E. Long-term, the stock's ~2.4× price growth since 2017 has mirrored its EPS, which also doubled over the 2017–2025E period. While no longer "on sale" as it was at $110 last year, the valuation is viewed as reasonable-to-attractive, assuming Masimo hits its achievable 2025 targets.

Management Quality and Insider Activity

Masimo’s management and board have undergone a dramatic and positive transformation. The previous founder-led era under Joe Kiani drew criticism for insular decisions, such as the abrupt Sound United deal. In contrast, the new leadership installed in late 2024 is led by CEO Katie Szyman, a med-tech veteran with a clear and transparent mandate. The setting is simple: drive commercial excellence, focus on core product innovation, and improve profitability.

The new board, chaired by a Politan nominee and composed of experienced outsiders, has already implemented more shareholder-friendly policies. This new regime has proven effective by delivering strong results despite significant operational challenges. Communication has also improved, with clearer guidance and more proactive investor engagement, signaling a fundamental governance reset.

Insider and institutional alignment is now strong. Insiders own a high ~9.7% of the stock. While former CEO Kiani retains a significant stake (~7.5%, with a legal dispute to claim up to ~13.2%) that could create a future share overhang, current board members are showing confidence, highlighted by a recent director's open-market share purchase.

Activist investor Politan Capital holds ~8–9% and its presence on the board ensures management will be held accountable. Furthermore, institutional ownership is very high at over 85% of the float, with many institutions increasing their stakes in 2025. This shareholder-aligned structure is focused on growing the core business profitably, and early execution is promising.

Risk Factors

Despite Masimo’s strengths, investors should be aware of several risk factors that could impact the company’s performance and valuation:

Competition and Technological Disruption

In the healthcare market, Masimo faces formidable competition from Medtronic, a larger rival with its entrenched Nellcor pulse oximetry technology that can compete aggressively on price. A significant long-term threat also comes from Big Tech companies like Apple, Google, and Samsung pushing into health monitoring. The patent fight over the Apple Watch underscores this risk. If these tech giants develop novel non-invasive monitoring technologies that bypass Masimo’s patents, they could encroach on both consumer and professional medical markets. To combat these competitive pressures and the risk of technological obsolescence, Masimo must maintain its technological edge through continuous and successful R&D innovation, for example by improving its rainbow© parameter suite.

Customer Concentration and Pricing Pressures

A significant portion of Masimo’s hospital revenue is concentrated, with one major distributor accounting for 18% of 2023 healthcare revenue. Any disruption with this partner could pose a short-term risk. The company also relies on contracts with the five largest Group Purchasing Organisations (GPOs), which provide essential market access but exert constant pricing pressure by demanding discounts in exchange for volume. Masimo is vulnerable to external pressures, such as hospital budget constraints or competitor price wars, which can lead to demands for better terms. Because the company’s consumables carry high margins, even modest price erosion could significantly impact profitability. While Masimo’s strategy is to sell on value and total cost of care, pressure from hospital cost-cutting remains a perennial risk.

Regulatory and Legal Risks

As a medical device company, Masimo is subject to strict FDA and global regulations, where a quality control failure like a product recall could damage its reputation and moat. While its track record is strong, changing standards for patient monitoring or data security could increase compliance costs and slow international expansion. Legally, Masimo faces costly and unpredictable litigation. The most significant is with Apple over the ITC import ban. After (seemingly) a huge win in 2023, Apple didn’t give up and used a loophole - the whole situation is now messy, with Masimo suing US Customs. In this case, Masimo can lose leverage and face stiffer competition. The company is also in a dispute with its former CEO over stock and severance claims. A related risk is that competitors could successfully design around Masimo's patents, eroding its unique selling proposition over time.

Supply Chain and Manufacturing

Masimo relies on a global supply chain, including manufacturing in Mexico, making it vulnerable to disruptions. For instance, new tariffs announced in Q2 2025 are expected to impact the costs of its Mexico-sourced products, and broader geopolitical tensions could further raise costs or complicate logistics. While the company mitigates these risks through multi-sourcing and supply chain redesigns, it remains a key issue to monitor. The company also faces cyber risks, highlighted by an incident in Q2 2025 that temporarily disrupted operations. Although it was resolved without material damage, it underscores Masimo’s vulnerability as a tech company. A major cyberattack could potentially halt manufacturing or compromise sensitive patient data, creating significant liability.

Macro-Economic and Market Risks

Masimo's business can be influenced by macroeconomic factors, despite the general resilience of the healthcare sector. High inflation, for example, can raise input costs for components and labour, potentially compressing gross margins if these increases cannot be offset by efficiencies or price hikes. The current high interest rate environment raises the company's cost of capital and can weigh on the stock's valuation by compressing equity multiples across the market. Furthermore, a recession could cause hospitals to tighten their capital budgets, delaying equipment upgrades. While Masimo's disposable sensor sales are typically steady, its capital equipment sales can be more volatile in a downturn. Finally, as a global company, Masimo's reported international revenue can be negatively impacted by a strong U.S. dollar due to foreign exchange rates.

Integration/Divestiture Execution

There is some execution risk in completing the divestiture of Sound United. If the sale process drags on or fails to fetch a good price, Masimo might decide to wind down parts of it, which could incur additional restructuring charges. Any distraction or management time spent on this is time not spent growing the core, so we hope for a clean exit by end of 2025. Integration risk is lower now (since they are de-integrating), but if Masimo were to consider any new acquisitions in healthcare to bolster its portfolio, integration of those would pose typical risks. Given management’s current stance, major M&A seems unlikely in the near term (they have their hands full), but it’s not impossible in a few years if they identify a complementary tech. Investors will closely scrutinise any such move given the last M&A fiasco.

Personnel and Culture Risk

The recent management upheaval created a risk to employee morale, with threats of a mass exodus following the former CEO. While this largely failed to materialise and key staff have remained, a significant turnover of veteran employees could still disrupt operations. The new leadership must preserve Masimo’s innovative culture while implementing its new strategy. Early signs are positive, as the company has successfully hired high-caliber executives like a new Chief Commercial Officer. However, maintaining employee buy-in through this transition remains an ongoing risk to monitor.

Market Sentiment and Expectations

Investor expectations for Masimo remain fickle, and the stock is on a "probation period" with Wall Street. As seen in the price drop after strong Q2 results, even good news can lead to a sell-off if the market was hoping for more. Any quarterly disappointment could cause a sharp negative reaction, amplified by the stock's high volatility (beta of ~1.23). Short-term price swings can also be driven by headlines related to ongoing legal battles, creating an event-driven risk premium.

Conclusion on Risks

In conclusion, Masimo’s risk factors are manageable but not trivial. The stability of its core consumables business, which hospitals will continue to buy in any economy, helps mitigate downside risk. However, investors should closely monitor competitive innovations, the outcome of the Sound United divestiture, legal battles, and the consistency of the new management's execution. While Masimo's robust moat and refocused strategy position it well to handle these challenges, consistent performance is key.

Our Scenarios (3–5 Year Horizon)

Bull Case (20% Probability)

Key Assumptions

This scenario assumes Masimo's renewed focus on innovation yields a "moonshot" product, like noninvasive glucose monitoring, that opens a major new revenue stream. A reorganised sales force successfully captures significant market share from competitors in areas like capnography or EEG monitoring. The company executes a highly successful sale of Sound United. This allows for complete debt elimination and aggressive share buybacks or a strategic acquisition. Furthermore, litigation is resolved favourably, perhaps through a licensing agreement or settlement with Apple that provides a steady, high-margin royalty stream. This case requires flawless execution, accelerated top-line growth, and a supportive med-tech market without major regulatory or reimbursement setbacks.

Financial Outcomes

These positive developments would drive core revenue growth into the 10–12% annual range. Gross margins would hold steady at approximately 63–65%, while operating margins expand beyond 30% as higher sales cover fixed costs. As a result, EPS would compound at over 20% annually, potentially reaching $8–10 per share by 2028. Recognising Masimo as a high-growth med-tech company with a fortified moat, the market could award it a P/E ratio in the high 20s or 30s. This valuation would plausibly double the stock price into the $280–$300 range, restoring its former premium valuation.

Base Case (60% Probability)

Key Assumptions

This base case is predicated on a "back-to-basics" execution story, where Masimo rebuilds investor trust by consistently delivering on its promises rather than pursuing flashy, dramatic moves. The central assumption is that growth is not driven by a single "home run" product but by incremental improvements to its existing offerings. For example, the launch of a next-gen Root platform and enhanced parameters would keep the product line competitive and encourage more frequent customer upgrades. A critical pillar of this scenario is the successful and timely sale of the Sound United division, which is expected to be completed by the end of 2025. These proceeds would be used strategically to pay down debt and increase cash reserves, strengthening the balance sheet. This outlook also depends on a stable external environment, including a healthy hospital market without major downturns in capital spending and rational competition that avoids drastic price wars. Furthermore, the threat from Apple must be contained, ensuring any reintroduction of its pulse oximetry feature does not significantly cannibalise Masimo's core hospital business. Finally, the scenario assumes management avoids new fiascos, staying on strategy and refraining from acquisitions that could spook investors.

Financial Outcomes

This disciplined operational approach is projected to generate steady core healthcare revenue growth of ~7–8% annually, sustained by gradual international expansion and a careful push into adjacent markets. Following the divestiture of the Sound United segment, the company's financial profile would improve significantly, allowing operating margins to expand into the high-20s and level off around 28–30% by 2026. This margin improvement would be supported by controlled spending, with R&D held at 8–10% of sales and SG&A growing only in line with revenue due to new efficiency initiatives. These fundamentals are expected to produce an EPS compound annual growth rate (CAGR) of approximately 15%, translating to earnings growth from an estimated ~$5 per share in 2025 to around ~$8 by 2028. Consequently, Masimo’s stock price would likely appreciate at a similar pace, tracking this steady earnings growth. This could place the stock in the $200–$235 range within 3 to 5 years, respectively, supported by a normalised P/E multiple in the mid-20s, consistent with a high-quality medical technology company. The ultimate outcome is not explosive growth, but the delivery of reliable and steady shareholder returns.

Bear Case (20% Probability)

Key Assumptions

In this scenario, revenue growth stalls at 0–3% per year. This could be caused by a failed sales force reorganisation, a slowdown in hospital purchasing, or a competitor launching a new platform that steals major accounts. At the same time, Masimo faces margin pressure from rising material costs or increased spending required to defend its market share. These operational issues are compounded by strategic failures. For instance, the company could lose its appeal against Apple, eroding its intellectual property defence. The sale of Sound United might also fall through or fetch a fire-sale price, leaving Masimo saddled with debt and ongoing losses. The re-emergence of insider turmoil, new costly regulatory requirements, or other management missteps could also contribute to this negative trajectory.

Financial Outcomes

Under these ‘perfect storm’ conditions, operating margins would likely slip back toward the low-20s. With growth stagnant, EPS would show little improvement, remaining around $4–$5 per share by 2027. The market, having lost confidence, would assign a lower P/E multiple, perhaps in the 15–18x range. This combination of flat earnings and a compressed multiple could cause the stock price to fall back into the double digits, potentially trading at $100 or lower. The narrative would shift to viewing Masimo as an ex-growth company with eroding margins.

Moat Resilience Index™ (MRI)

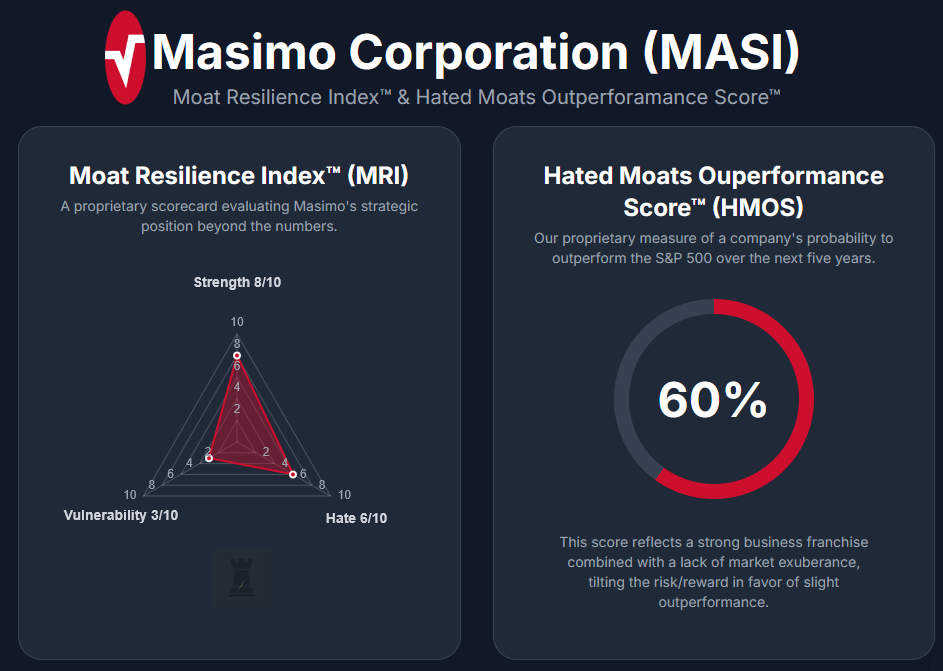

We evaluate Masimo’s moat on three custom proprietary dimensions (Moat Strength, Moat “Hate”, and Moat Vulnerability ), each scored on a 1 (worst) to 10 (best) scale, and then derive our proprietary “Hated Moats Score”, which represents the probability Masimo will outperform the broader market over 5 years.

Moat Strength: 8/10

Masimo’s moat is robust. The company enjoys a dominant position in its niche of hospital pulse oximetry with technology that has proven superior in clinical studies. Its large patent portfolio and ongoing innovations (e.g., rainbow® multi-parameter platform) create high barriers for direct tech replication. Moreover, Masimo’s long-term contracts and integration into hospital workflows give it significant switching-cost advantages. Hospitals are notoriously sticky once they standardise on a monitoring system, due to training, interoperability, and GPO agreements. Masimo also has an intangibles-based moat, i.e. a strong brand reputation among anesthesiologists, nurses, and respiratory therapists. In short, when it comes to noninvasive patient monitoring, Masimo is often the name to beat. We stop short of a perfect 10 because this is still a focused niche (not a broad, unassailable platform across all of med-tech) and because the company’s past diversification attempt didn’t leverage the moat (indicating the moat applies mainly to its core segment). But within its domain, Masimo’s moat is very strong. This is reflected by its ability to sustain premium pricing and high margins, and even legally enforce its IP against a behemoth like Apple. Few mid-size companies can boast that kind of moat strength.

Moat “Hate”: 6/10

This metric gauges how contrarian or “hated” the company is despite having a moat. We score Masimo a 6, indicating a moderate level of “hate” still baked in. A year ago, Masimo was a solid 8 or 9 on this scale. It was widely hated by the market (the stock collapse and the vitriolic proxy battle showed that). Now, sentiment has slowly improved. The company has addressed many concerns, so it’s not despised, but neither is it beloved yet. The stock’s volatile reaction to earnings implies investors haven’t fully shaken off their wariness. Masimo’s story (post-activism turnaround) is still somewhat underappreciated by the broader market, in our view. It doesn’t get the hype of, say, a cutting-edge med-tech growth company, partly due to the memory of the recent stumble. The fact that it trades at a discount to peers and has a meaningful short interest indicates some lingering negativity. This is actually a positive for contrarian investors. Masimo has a solid moat, but not everyone believes in it yet or they’re taking a “wait and see” approach. Thus, on the Hated Moats spectrum, Masimo is moderately hated/underestimated. Not an extreme contrarian play, but certainly not a market darling either. As execution continues, we’d expect this “hate” factor to diminish (the score would move lower as the company gains respect and a premium valuation – at which point the contrarian opportunity would be gone).

Moat Vulnerability: 3/10

Here we assess how susceptible Masimo’s moat is to being breached or eroded. We assign a 3 (where 1 is highly secure and 10 is very vulnerable), meaning we see low vulnerability overall. Masimo’s moat, while strong, is not utterly invincible. Yet it’s pretty well defended. The low score reflects that Masimo operates in a specialised field with high entry barriers. Any new competitor would need years of R&D, FDA approvals, and clinical validation to match Masimo’s performance. The network effect of installed base and Masimo’s OEM partnerships (many monitor makers license Masimo SET® for their devices) also protect it. That said, why not lower score? Because there are some credible long-term threats: big tech’s interest in health wearables is one (Apple). Another is that hospital purchasing could consolidate further. Additionally, if Masimo ever rests on its laurels, Medtronic or others like EDwards, Philips, etc., could innovate in advanced monitoring, eroding Masimo’s moat. However, currently Masimo has the edge and is showing no signs of complacency on innovation. The biggest vulnerability might actually lie in execution/strategy rather than direct competition. With new management refocused, that risk is lower. Overall, we think Masimo’s moat is resilient, barring extraordinary external changes (like a totally new monitoring paradigm or Apple-like disruptor), its position in its niche should remain secure. So, we view vulnerability as quite low.

Hated Moats Outperformance Score™: 60%

Combining the factors above, we derive our Hated Moats Score, which is the probability Masimo will outperform the S&P 500 over the next 5 years. Given Masimo’s strong moat, still-recovering market sentiment, and relatively low vulnerability, we are inclined to believe it has above-average chances to beat the market. We assign a Hated Moats Score of 60%, meaning we believe there is roughly a 60% probability Masimo’s total return will exceed that of the S&P 500 over a five-year horizon. This is a favourable odds in our framework. While we have confidence in Masimo’s moat-driven recovery, we also acknowledge that it’s a mid-cap single-product-line company in a competitive landscape. It’s not immune to hiccups, and broader market conditions could influence outcomes. So we stop short of an overwhelmingly bullish probability. Still, with 60%, we lean positively.

In summary, Masimo scores 8/10 on Strength, 6/10 on Hate, 3/10 on Vulnerability, and a 60% Hated Moats outperform probability. This paints a picture of a company with a high-quality moat that is somewhat underappreciated, and with limited risk of that moat being disrupted. That’s a combination that often yields attractive long-term returns, assuming management continues to execute well.

Conclusion

Masimo is a fundamentally strong med-tech business that stumbled and is now regaining its footing. It possesses a durable competitive moat in patient monitoring, built on proprietary technology, entrenched hospital relationships, and a recurring revenue model. The company’s financial performance is on an upswing. Core revenue is growing steadily, margins are expanding significantly, and earnings are rebounding from the one-off loss in 2024 to robust growth in 2025. With the distraction of the consumer electronics venture being eliminated, Masimo can focus 100% on what it does best - innovating and selling critical-care monitoring solutions. New management has shown it can execute and is aligned with shareholders. The balance sheet is set to improve post-divestiture, and free cash flow is healthy.

At the current stock price (~$140-$145), Masimo offers a balance of offense and defence. Offensively, there is upside potential if the company even modestly exceeds growth expectations or if the market rewards its higher margins with a better multiple. Defensively, the downside is mitigated by the company’s strong cash flows, sticky demand, and the fact that the stock already underwent a huge correction, i.e. it is nowhere near euphoric valuation levels. Masimo’s risk/reward profile over a 3–5 year horizon skews favourable, with our base and bull scenarios indicating solid gains, and the bear case, while a risk, representing a manageable probability.

Short-Term Outlook (< 1 Year)

In the short term, we expect the stock could be range-bound or moderately higher, as investors await tangible evidence of sustained growth. Catalysts like the successful sale of Sound United or continued earnings beats and raised guidance could push shares toward the high-$100s over the next few quarters. We also wouldn’t rule out corporate developments (e.g., a settlement with Apple or even M&A interest) that could provide upside surprises. Conversely, any slip-up in execution or softer outlook could cause volatility. Although, given current guidance and backlog, short-term surprises are more likely to be positive or within expectations.

Long-Term Outlook (3-5 Years)

Over the longer term, we see Masimo delivering solid shareholder value. We project the stock to appreciate broadly in line with per-share intrinsic value growth (about high-single to low-double digits annually in our base case) supported by ~28–30% operating margins and steady mid- to high-single-digit core growth. With a 5-year hated-moat outperform probability of ~60%, we view Masimo as more likely than not to outpace the S&P 500 over the next five years, given its moat and improving fundamentals.

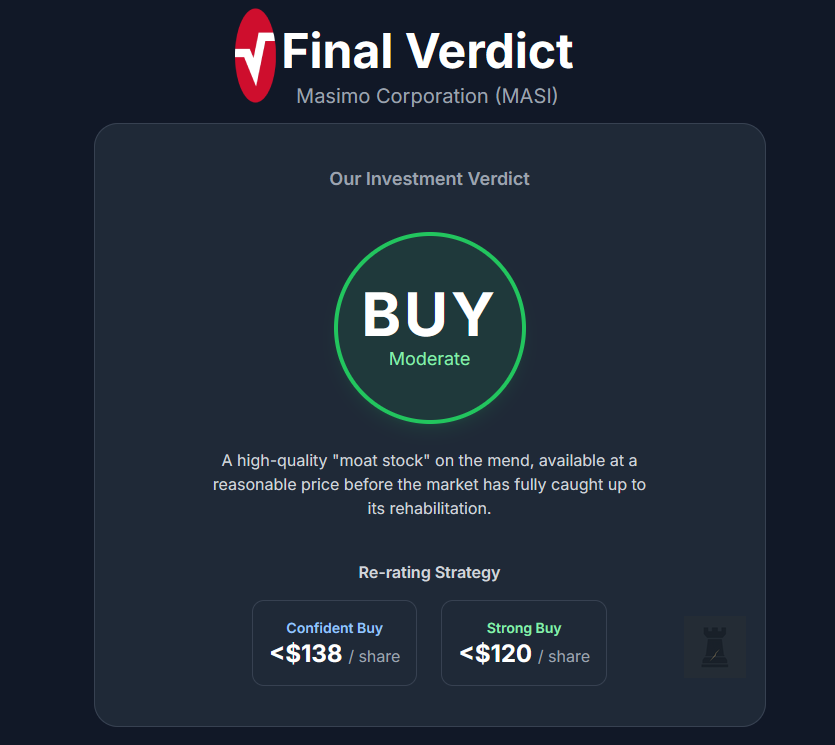

Final Verdict

Our Investment Verdict: BUY

We rate Masimo as a Buy - leaning towards a Moderate Buy/Outperform rather than an aggressive strong buy, because while we are very positive on the core business, we acknowledge that growth is likely to be steady rather than explosive. This is a high-quality franchise available at a reasonable price, exactly the kind of situation long-term, fundamentals-focused investors tend to appreciate. One might say Masimo is a “moat stock” that temporarily lost its way and is now on the mend. The market has not fully caught up to that rehabilitation. Assuming all things unchanged, here is our re-rating strategy:

Rating for ‘Confident Buy’: <$138 per share

Rating for ‘Strong Buy’: <$120 per share

Disclaimer & Our Investment

We own shares of Masimo at $142.02 per share since September 16th, 2025. No part of this entire analysis should be used as a financial advice and should be used solely for educational and research purposes.

Final words

In conclusion, Masimo represents a high-quality, if somewhat under-the-radar, investment opportunity. It’s not a flashy high-growth tech name, but a steady med-tech compounder with a dominant niche. The stock’s recent underperformance has set the stage for potential outperformance as the company executes its back-to-core strategy. Masimo has the makings of a resilient compounder that can deliver market-beating returns with lower fundamental risk, supported by a wide moat that is finally being leveraged the way it should.

Buying now offers a good price (albeit not great) as an entry point with a solid upside potential. At this point, it’s basically a bet on a competent management executing consistently well and burying the skeletons in the company’s closet for good. The potential risk is offset by a contrarian opportunity with favourable returns and since the stock is not at the peak of its ‘hate’ anymore, this might be the last chance to hop on the train before it leaves to the station called ‘Premium Valuation’. In the grand scheme, Masimo’s vital signs (financially and strategically) are stable and improving, making this a healthy addition to a portfolio for those seeking value grounded in strong business fundamentals.

Great analysis! Good to see you cover small names as well!

Visuals look great and unique.

Keep up the great work