SAP: Deep Dive Analysis

SAP Has Lost Nearly Half Its Value. Has the Market Misread the Moat?

What Does the Company Do?

SAP is an enterprise software company that helps large organisations run many of their most important business processes through an integrated suite of applications, data and technology services.

At first glance, SAP appears relatively easy to understand. It is the ERP (Enterprise Resource Planning) company. But while analysing, we quickly learnt that this description, while technically correct, is far too narrow these days. At its core, SAP records and coordinates much of the complicated work taking place across finance, procurement, manufacturing, supply chains, human resources, sales and other departments, using integrated applications and shared business data. In practical terms, SAP allows a company to process orders, track inventory, pay employees, manage suppliers, plan production and close its accounts while reducing its reliance on disconnected/unsynced applications, spreadsheets and manual reconciliations.

In simple terms, SAP forms part of the digital backbone that records what is happening across a business and helps ensure that its essential processes can continue operating.

It’s one of those companies whose importance becomes clearer when you imagine removing it. SAP software often sits underneath the daily operations of some of the world’s largest and most complicated organisations. Orders may flow through it, financial records are maintained in it, employees may be paid through it, and inventory and production schedules can depend on it. Once SAP becomes the system of record, replacing it can require years of planning, data migration, process redesign, systems integration and employee retraining. This makes SAP more of an operational infrastructure that is deeply embedded in business processes, and in some cases vital to them, than an ordinary ‘nice-to-have’ software tool. Customers may dislike the cost, complexity and UX (and they often do), but changing the system can be considerably more expensive and dangerous than continuing to use it.

SAP built its franchise around on-premise enterprise applications and ERP, but its portfolio has expanded far beyond traditional ERP. S/4HANA remains the core financial and operational system, but the company has also expanded through multiple acquisitions. The Business Technology Platform connects applications, data, analytics, development tools and AI capabilities across the broader suite. SAP is therefore best understood as a broad business-software, data and workflow platform.

The company is aggressively shifting customers from local software to cloud subscriptions via "RISE with SAP" while embedding AI directly into core business workflows. Although this transition increases revenue predictability, lingering investor concerns regarding lengthy migrations, slower backlog growth, and generative AI disruption risks triggered a sharp sell-off following Q4 2025 results.

Ultimately, SAP is caught between two competing narratives. There’s a bearish perspective viewing it as a legacy company vulnerable to disruption, and a constructive outlook seeing a deeply embedded enterprise platform successfully migrating its massive installed base to the cloud.

That gap between operating reality and market sentiment is exactly what made SAP a compelling candidate for Hated Moats Analysis.

Let’s dive in!

Competitive Moat & Peer Comparison

The Moat

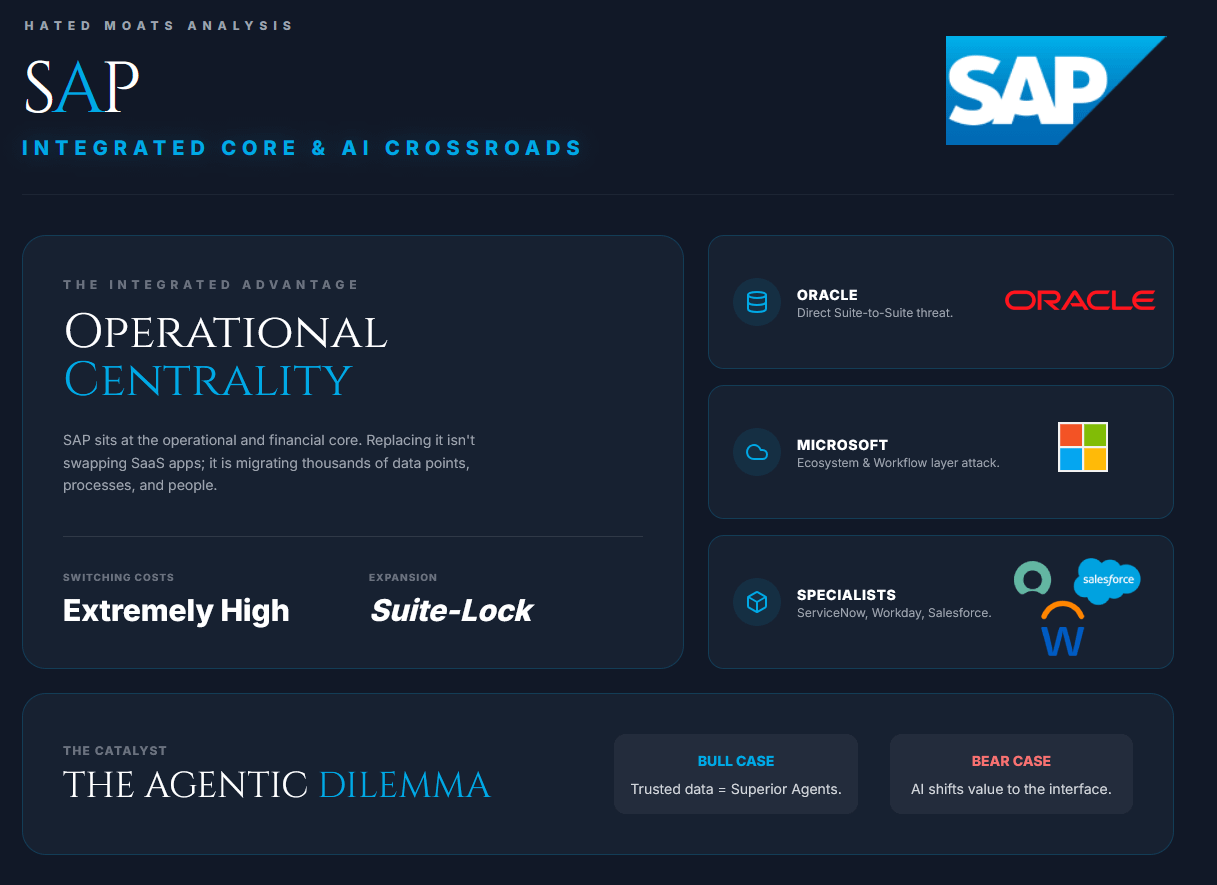

SAP’s moat is best understood as a combination of switching costs, process centrality, and accumulated business complexity. Its software often sits at the operational and financial core of an enterprise, recording transactions across finance, manufacturing, procurement, inventory, supply chains, and human resources. So it’s not a tool that’s used just by one department.

Naturally, replacing this isn’t like swapping one SaaS application for another. It means migrating years of data, rebuilding customised processes, reconnecting third-party systems, testing financial controls, and retraining thousands of employees, all while keeping the business running. Once SAP becomes the system through which orders, payments, production schedules, and accounting records move, the customer is relying on operational infrastructure. And companies generally don’t replace critical infrastructure unless the existing system has become more dangerous than the migration itself.

SAP’s real strength lies in its integrated suite. A customer may begin with core ERP, but SAP can expand into procurement through Ariba, expenses through Concur, human resources through SuccessFactors, and data management through SAP Business Technology Platform. Each additional product uses related data, permissions, and integrations, making the environment harder to separate. SAP’s scale reinforces this advantage through a global network of systems integrators, consultants, and software partners, alongside a client list that includes over 90% of the Fortune 500.

The Competition

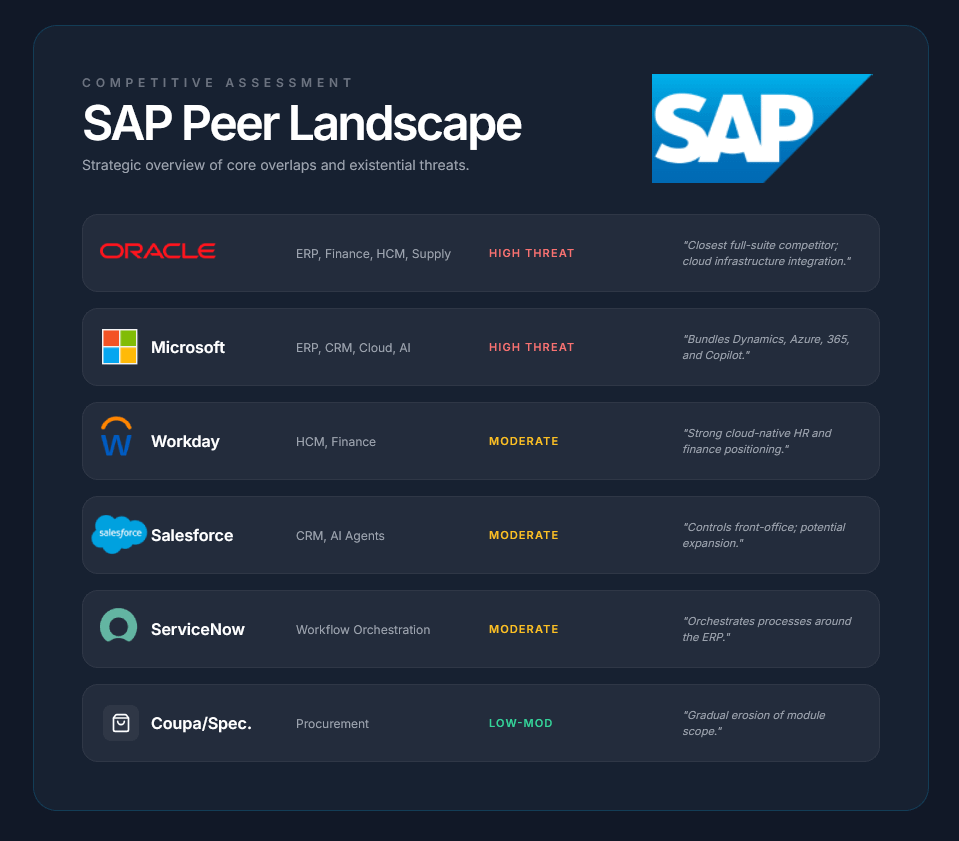

The competitive set is broad, but Oracle ORCL 0.00%↑ remains the closest direct threat. Oracle Fusion covers finance, human capital management, supply chains, and manufacturing, combining applications with Oracle’s database and cloud infrastructure. Microsoft MSFT 0.00%↑ attacks from a different direction. Dynamics 365 offers less depth in complex environments, but connects ERP and CRM with Azure, Microsoft 365, and Copilot, and this ecosystem advantage shouldn’t be underestimated. Workday WDAY 0.00%↑ is strongest in human resources, Salesforce CRM 0.00%↑ dominates customer-facing software, and specialists like ServiceNow NOW 0.00%↑ can remove individual workflows without replacing the core ERP. SAP therefore faces both full-suite competition and gradual scope erosion from specialised vendors.

SAP’s weakness is that much of its moat can look uncomfortably similar to customer dependence. Large implementations can be expensive, heavily customised, and difficult to upgrade. The ongoing migration from legacy SAP environments to S/4HANA also creates a rare moment when customers must reconsider their architecture, implementation partner, and long-term vendor strategy. We believe that most will probably remain with SAP because migration to a competitor would be even more disruptive, but the decision isn’t automatic. Regulatory pressure provides further evidence of the tension. The European Commission opened proceedings concerning SAP’s on-premise maintenance policies, raising concerns that certain practices limit customers’ ability to use competing support providers. SAP subsequently offered commitments, which remain under review. While this doesn’t invalidate the moat, it shows that aggressive monetisation of switching costs can create customer resentment and regulatory resistance.

What about AI?

AI is where the bull and bear cases meet. Bulls argue that AI makes SAP’s position more valuable because useful enterprise agents need trusted data, permissions, process knowledge, and access to the systems where transactions are actually executed. SAP’s Knowledge Graph, Joule, Business Data Cloud, and Joule Studio are designed around that advantage, allowing agents to understand business relationships and act across finance, procurement, HR, and supply-chain workflows. In this view, SAP’s decades of accumulated process knowledge become more valuable because AI can turn a passive system of record into an active system of execution.

Bears argue that AI could weaken the interface between users and SAP. If employees increasingly work through Microsoft Copilot, Salesforce Agentforce, Sana from Workday, or independent agents, SAP risks becoming an invisible database beneath a more valuable engagement layer. Oracle is embedding agentic applications directly into Fusion, Microsoft is connecting agents across Dynamics and Microsoft 365, and Workday is opening its finance and HR data to third-party agents. SAP’s data and process context provide a credible advantage, but they don’t provide exclusivity. Every major competitor wants to become the agentic control layer for enterprise work and have their portion of the lunch.

Summary

We can conclude that SAP’s moat is wide, but it isn’t untouchable. Its installed base, switching costs, product breadth, and process knowledge make rapid displacement unlikely. The greater risk is gradual erosion, with competitors taking individual workflows, controlling the AI interface, or using a major cloud migration as an opportunity to pull customers away.

The real debate is whether AI deepens SAP’s control of enterprise operations, or finally gives customers a practical way to reduce their dependence on it.

Recent Stock Performance & Market Sentiment

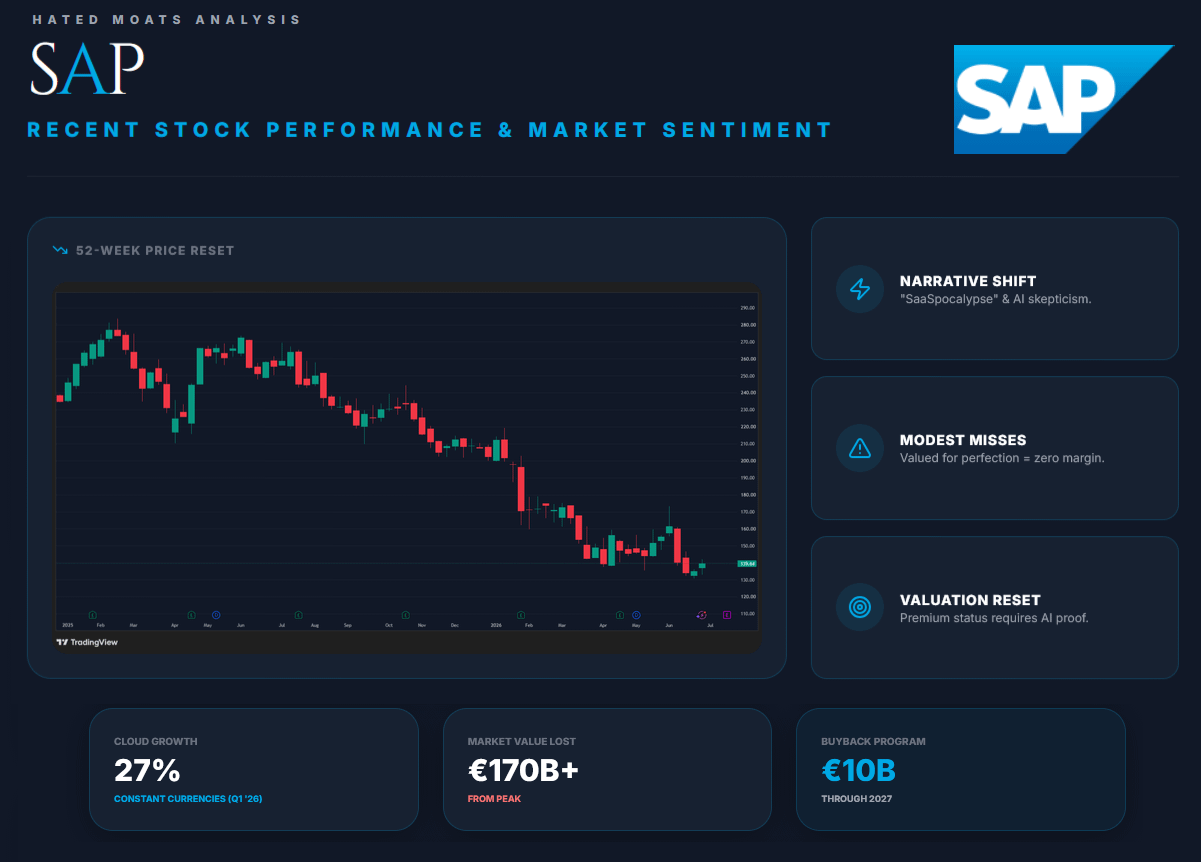

SAP’s stock has been punished far more severely than the underlying business performance would suggest. As of July 2, 2026, the shares traded at roughly €140 on Xetra, implying a market capitalisation of about €165B. That represents a decline of around 33% since the beginning of the year and roughly 47% from the 52-week high, i.e. more than €170B of market value has disappeared from the peak.

That’s a dramatic reset for a company whose Q1 2026 cloud revenue still grew 27% at constant currencies, whose current cloud backlog increased 25%, and whose operating profit exceeded expectations. The market isn’t treating SAP as a broken business but rather as a premium software asset that no longer deserves the same valuation unless growth reaccelerates and AI proves to be a genuine earnings driver.

The de-rating began when investors had already become increasingly sceptical about traditional enterprise software and whether AI agents might weaken seat-based pricing, reduce the importance of existing interfaces, or shift value towards Microsoft, Oracle, and other broader platforms. SAP’s Q4 2025 report then gave the market a company-specific reason to sell. Cloud backlog growth and the 2026 outlook came in below elevated expectations, and the shares fell as much as 17% on January 29.

The key point is that SAP reported growth that was slightly less exceptional than the market had priced in, not deteriorating fundamentals. We all know that when a stock is valued on near-perfect execution, modest disappointment can produce an outsized reaction. SAP’s problem in this environment was that the valuation left little room for anything short of acceleration.

Q1 2026 should’ve helped repair the narrative. Cloud revenue, total revenue, and non-IFRS operating profit all exceeded expectations, while management maintained full-year guidance. Yet the recovery proved rather temporary. The shares sold off again in June amid renewed concerns about AI disruption and software competition, as it goes these days with “SaaSpocalypse”.

Management’s behaviour has become more supportive as the price has fallen, though. SAP announced a €10B repurchase programme and completed its first €2.62B tranche at an average price above the current market price. CFO Dominik Asam also bought about €1M of shares following the January sell-off. Those purchases don’t prove undervaluation, but they do show internal confidence.

SAP is now caught between strong operating evidence and a market increasingly focused on what could go wrong. The bears see slowing backlog growth, AI disruption, and stronger platform competition. The bulls see a deeply embedded enterprise system still growing cloud revenue above 20%, expanding profits, and repurchasing shares.

The business is becoming more interesting precisely because the stock has become more hated.

Fundamental Analysis

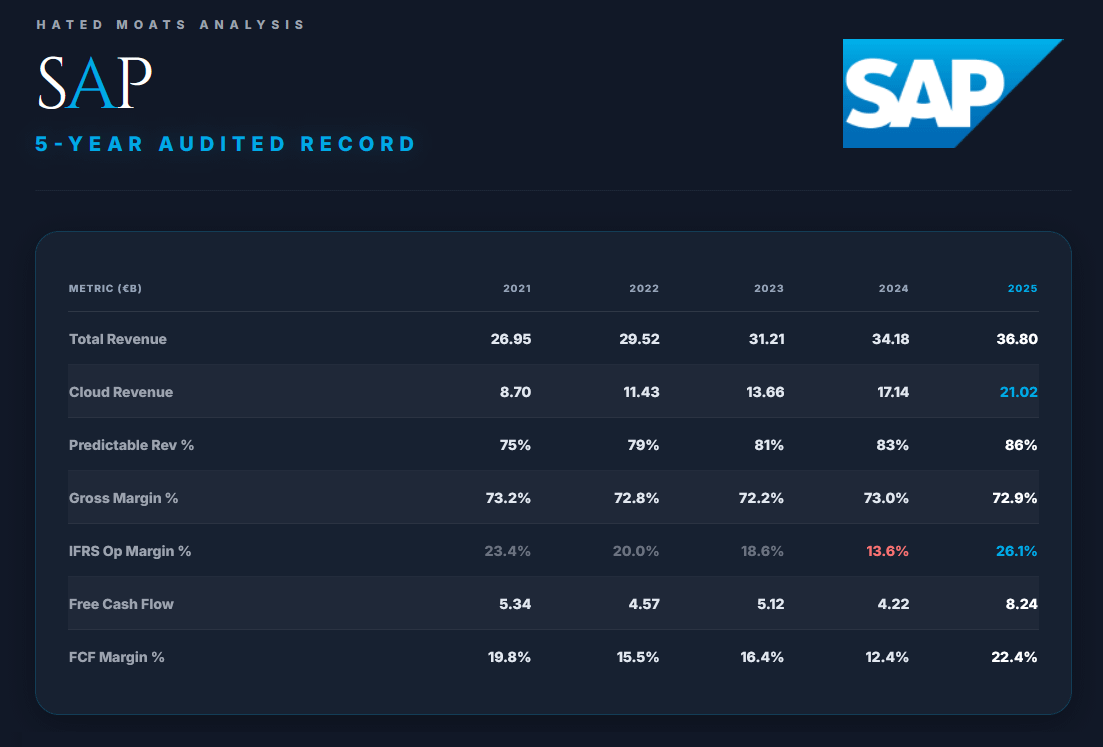

SAP’s fundamentals need to be analysed as a business in transition rather than as a conventional mature software company. The consolidated revenue line is growing at a high-single-digit rate, but beneath it 2 businesses are moving in opposite directions. Cloud ERP Suite revenue is expanding above 20%, while software licences and support are shrinking. The central question is whether cloud growth can remain strong enough, profitable enough, and durable enough to offset the decline of the legacy base without requiring permanently elevated spending.

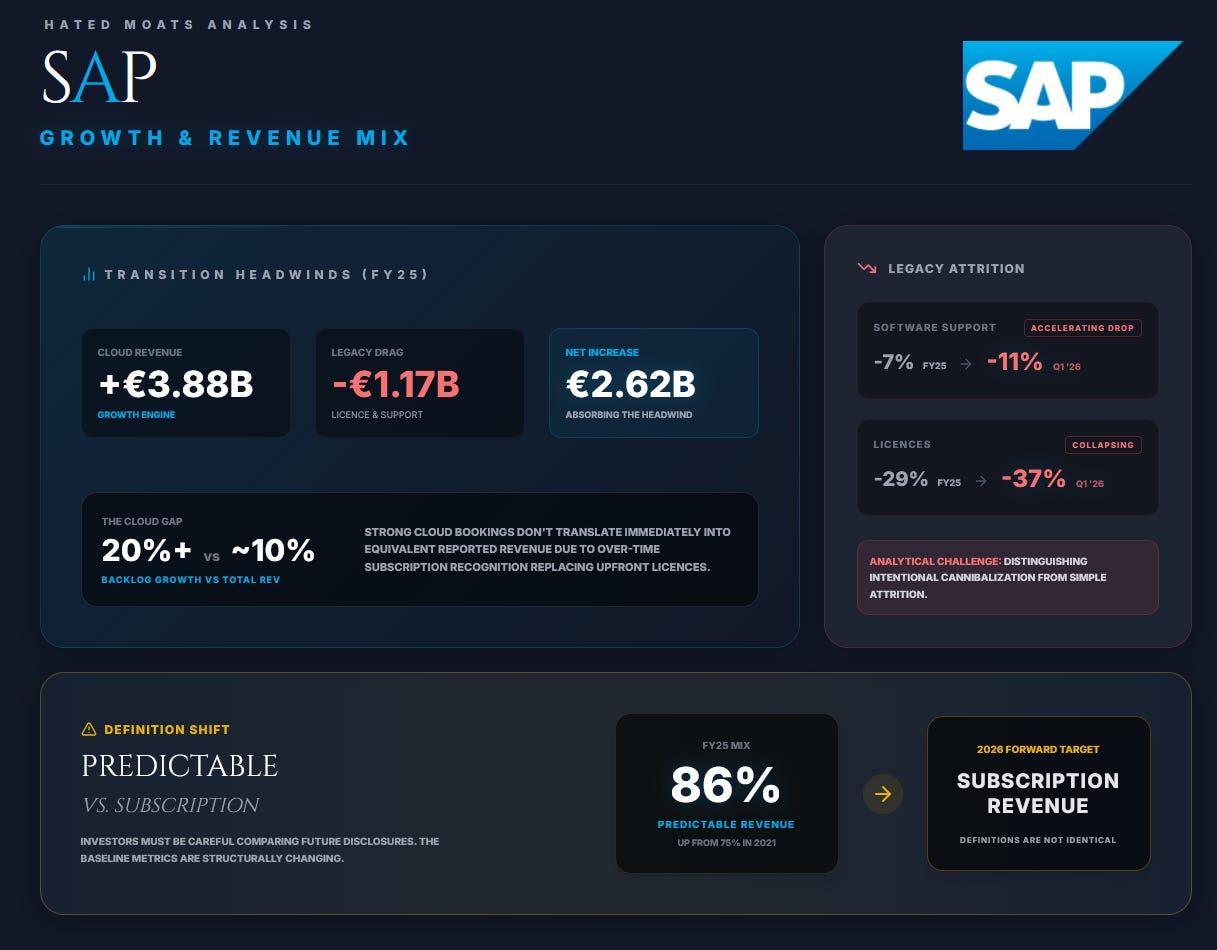

The evidence so far is broadly constructive. FY2025 revenue reached €36.80B, up 8% as reported and 11% at constant currencies. Since 2021, revenue has compounded at roughly 8.1% annually, but cloud revenue has grown at almost 25% per year, from €8.70B to €21.02B. Cloud now represents 57% of group revenue, compared with only 32% in 2021. SAP’s Cloud ERP Suite, which includes the products most closely connected to its core ERP offering, grew 28% to €18.12B in 2025, or 32% at constant currencies. That is the economic engine of the company today.

The audited 5-year record shows both the progress and the accounting noise created by SAP’s transformation:

Growth & Revenue Mix

Transition Headwinds

SAP’s growth quality is better than the consolidated revenue figure suggests. In 2025, cloud revenue increased by €3.88B, while software licences and support declined by approximately €1.17B and services fell slightly. In other words, the cloud business had to absorb a meaningful legacy headwind before producing the group’s €2.62B net revenue increase. This means that customers are moving from perpetual licences and maintenance contracts towards recurring cloud subscriptions, changing when SAP recognises revenue and how much it earns over the customer relationship.

The Cloud Gap

The transition also makes reported growth sensitive to how quickly customers migrate. New cloud sales replace upfront licence revenue with subscriptions recognised over time, while migrations to RISE mainly replace support revenue with cloud subscriptions. Over time, the model should produce greater lifetime revenue, better visibility, and more opportunities to cross-sell. During the transition, however, strong cloud bookings don’t translate immediately into equivalent reported revenue. That helps explain why cloud backlog can grow in the twenties while total revenue grows closer to 10%

Legacy Attrition Concerns

SAP’s old business is a genuine drag, not something we should wave away. Software support revenue fell 7% in 2025 to €10.53B, while licence revenue dropped 29% to €990M. Q1 2026 accelerated this trend, with support down 11% as reported and licences down 37%. Management expects the support decline to accelerate further as more customers move into the cloud. The favourable interpretation is that SAP is intentionally cannibalising itself before somebody else does. The less favourable interpretation is that part of this highly profitable maintenance stream could disappear before replacement cloud revenue fully matures. Distinguishing successful migration from simple attrition will remain one of the most important analytical tasks, and as we learnt, not an easy one.

Shifting Metric Definitions

The revenue mix has nevertheless become much more attractive. Cloud revenue + software support represented 86% of FY2025 revenue, up from 75% in 2021. SAP calls this “more predictable revenue”, which is a more accurate description than recurring revenue because some support agreements require renewal and aren’t contractually recurring forever. Beginning in 2026, SAP is replacing this measure with subscription revenue, defined as cloud revenue + time-based on-premise licences and associated support. We need to note here that investors should be careful when comparing future disclosures with the old 86% figure because the definitions aren’t identical.

Customer Base & Revenue Visibility

The Transparency

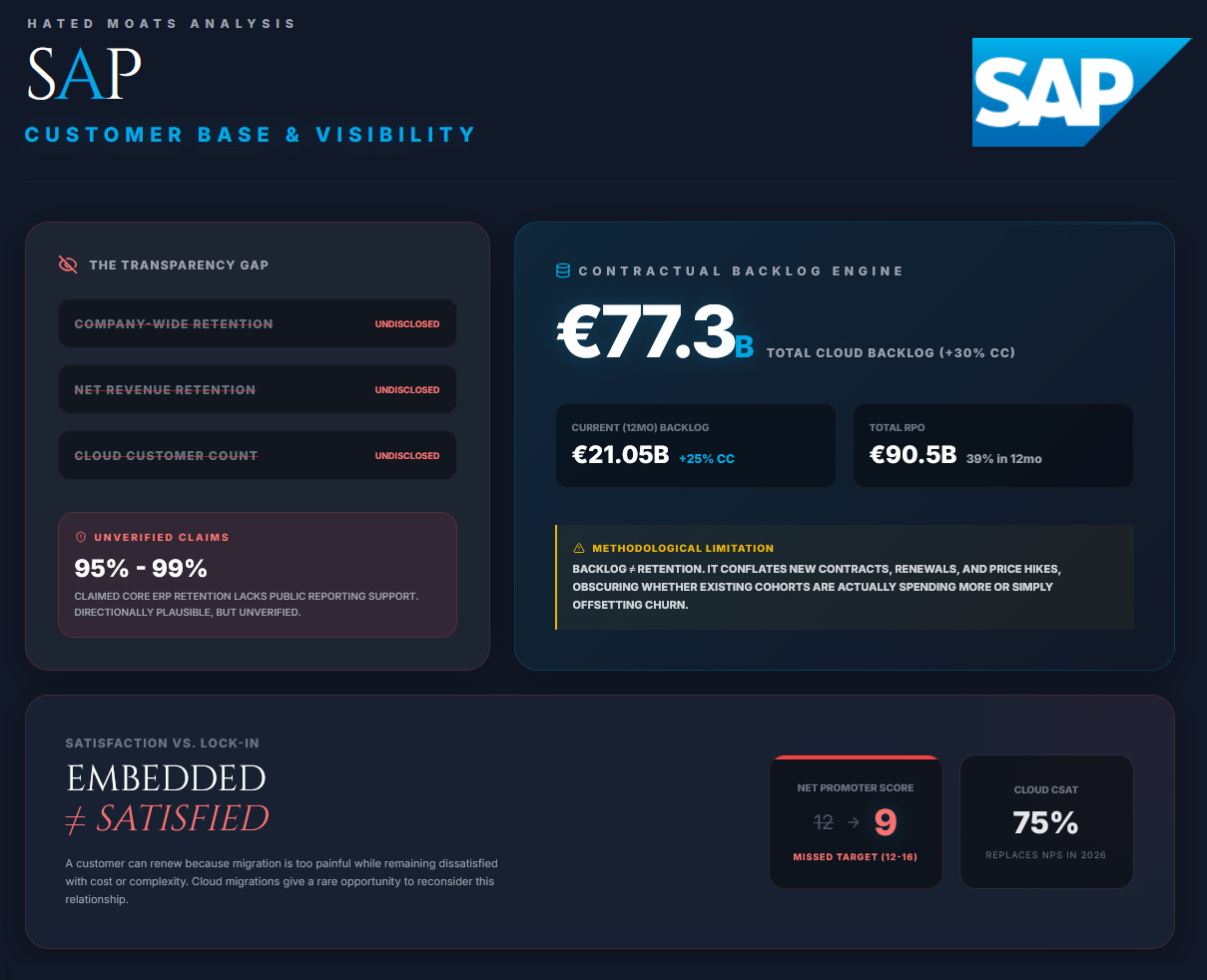

SAP doesn’t disclose the customer metrics that investors would ideally want, such as company-wide retention, net revenue retention, cloud customer count, or expansion rates by cohort. Honestly, we’re not big fans of this since it limits our ability to prove (or at least estimate) how much growth comes from new customers, migrations, price increases, or existing-account expansion. Claims of 95% to 99% retention may be directionally plausible for core ERP installations, but they aren’t supported by SAP’s public reporting and shouldn’t be treated as verified data.

Backlog as a Growth Engine

The strongest evidence available is contractual backlog. Current cloud backlog, meaning cloud revenue expected to be recognised within the following 12 months, reached €21.05B at the end of 2025. It grew 16% at reported currencies and 25% at constant currencies. Total cloud backlog, which includes contracted cloud revenue beyond the next year, reached €77.3B, up 22% and approximately 30% at constant currencies. Total remaining performance obligations across cloud, support, and eligible services were €90.5B, compared with €78.4B a year earlier, with around 39% expected to be recognised within 12 months.

These figures provide unusually strong revenue visibility, but backlog isn’t the same as retention. It incorporates new contracts, renewals, upsells, modifications, pricing changes, and currency movements. Certain contracts containing termination rights also aren’t included beyond the enforceable period. Backlog growth therefore tells us that contracted demand is expanding, but it doesn’t really reveal whether an existing customer cohort is spending more or whether SAP is compensating for churn with new business. That’s a big methodological limitation in an analysis…

Satisfaction vs. Lock-in

Customer satisfaction also provides a useful counterweight to the lock-in narrative. SAP’s Customer Net Promoter Score (NPS) fell to 9 in 2025, below its target range of 12 to 16 and down from 12 in 2024. From 2026, management is replacing NPS with Cloud Customer Satisfaction, which scored 75% in 2025 but isn’t directly comparable with NPS. SAP’s customers may be deeply embedded, but embeddedness shouldn’t be confused with actually liking the system. A customer can renew because migration is too painful while remaining dissatisfied with cost, complexity, or support. That distinction is important because cloud migrations give customers a rare opportunity to reconsider this relationship.

Profitability & Margin Structure

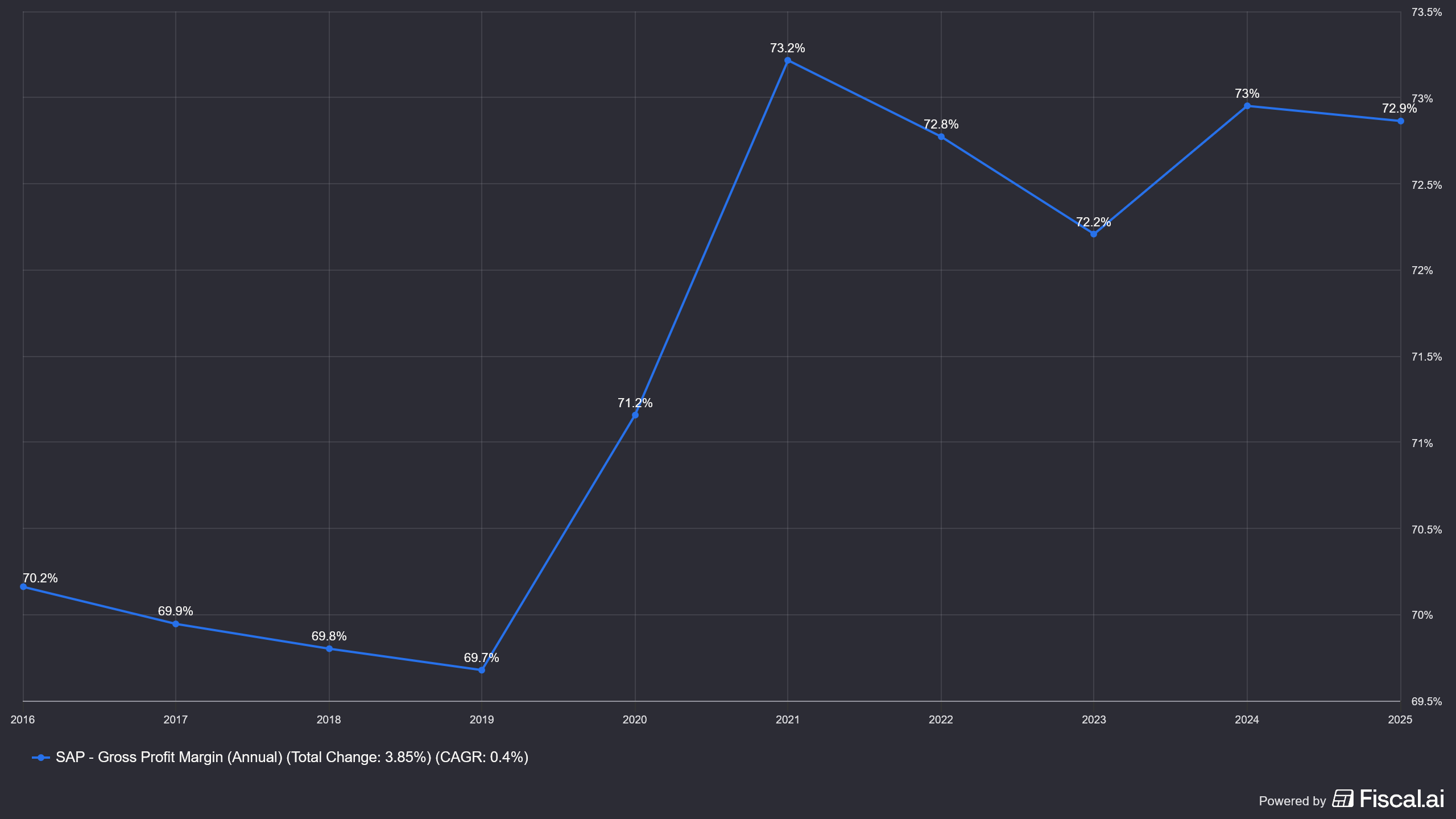

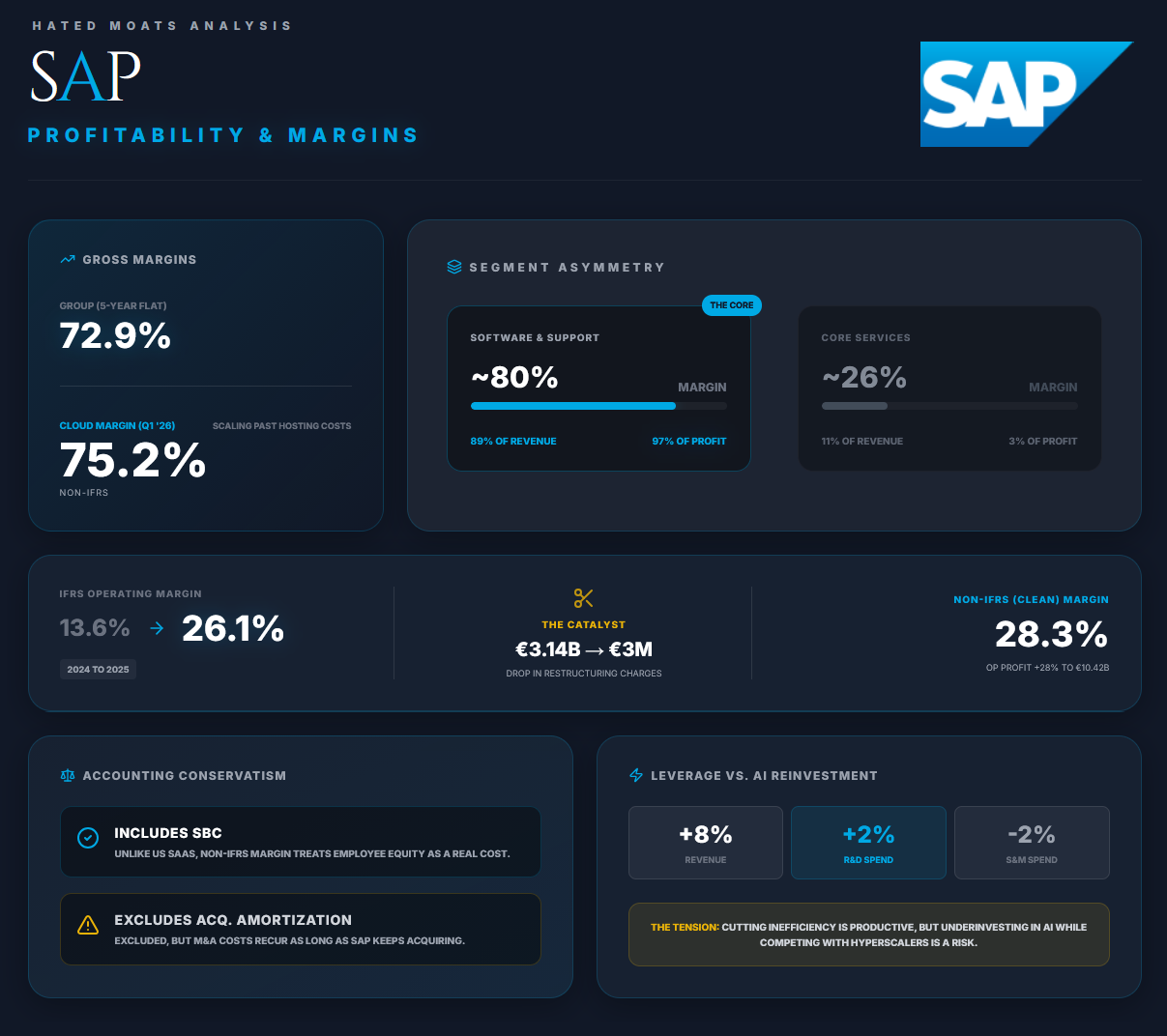

SAP’s gross economics remain excellent. Audited gross profit was €26.81B in 2025, representing a 72.9% margin, broadly unchanged over the past 5 years. Cloud gross margin improved to roughly 74%, showing that the cloud portfolio is scaling even as SAP incurs hosting, hyperscaler, and migration-related costs. Q1 2026 cloud gross margin reached 74.6% IFRS and 75.2% non-IFRS. This means that the cloud transition hasn’t structurally damaged gross profitability so far.

Core Value Drivers

The segment economics show where the value is created. On SAP’s non-IFRS segment basis, Applications, Technology & Support generated €32.85B of revenue and €26.31B of gross profit, an approximately 80% margin. Core Services generated €3.95B of revenue but only €1.02B of gross profit, a margin of roughly 26%. Applications, Technology & Support accounted for around 89% of group revenue and approximately 97% of the profit generated by the two segments before central expenses and accounting adjustments. SAP is thus fundamentally a high-margin product company with a supporting professional-services operation, rather than a consultancy disguised as software.

The Margin Recovery

FY2025 IFRS operating profit more than doubled to €9.62B, lifting the operating margin from 13.6% to 26.1%. That improvement looks extraordinary, but most of it reflects the conclusion of SAP’s restructuring programme. Restructuring charges fell from €3.14B in 2024 to just €3M in 2025. Total SBC fell from about €2.69B in 2024, including €309M classified within restructuring, to €1.70B in 2025. The cleanest comparison is therefore non-IFRS operating profit, which increased 28% to €10.42B and produced a 28.3% margin.

Earnings Quality & Accounting

SAP’s adjusted reporting is also more conservative than that of many US SaaS companies in one important respect. Since 2024, its non-IFRS results include share-based compensation. SAP excludes acquisition-related amortisation and expenses, formal restructuring charges, specified regulatory matters, the Teradata litigation, and gains or losses on equity investments, but it doesn’t simply add SBC back to profit. That makes SAP’s non-IFRS operating margin more economically meaningful than an adjusted margin that treats employee equity as free. Acquisition amortisation remains a real recurring cost, however, and the company itself acknowledges that excluded acquisition charges can recur whenever it keeps buying businesses.

Operational Leverage vs. AI Reinvestment

Research and development spending reached €6.63B in 2025, equal to 18.0% of revenue, while sales and marketing represented 24.1%. R&D grew only 2% and sales and marketing declined 2%, despite 8% revenue growth. That cost discipline drove leverage, but we note that investors need to monitor whether this can continue while SAP simultaneously funds cloud infrastructure, data integration, autonomous agents, and frontier AI research. Cutting inefficiency is productive while attempting to compete with Microsoft, Oracle, and hyperscalers while underinvesting wouldn’t be…

Earnings Quality and Share-Based Compensation

The Net Income

Audited profit after tax from continuing operations reached €7.33B in 2025, compared with €3.15B in 2024. Diluted EPS increased from €2.65 to €6.10. As with operating profit, the comparison is flattered by the 2024 restructuring charge. Non-IFRS earnings increased much more moderately, with basic non-IFRS EPS rising from €4.53 to approximately €6.14. The underlying improvement was still strong, but earnings didn’t economically double in one year.

Equity Investment Dynamics

SAP also recorded substantial gains from equity securities. Finance income included €1.39B of gains from disposals and fair-value movements, partly offset by €625M of related losses in finance costs. Non-IFRS results remove the net effect because it’s volatile and largely unrelated to the operating software business. We agree with using adjusted earnings to assess operating progress, but realised investment gains still represent genuine value received by shareholders and we believe they shouldn’t be ignored entirely.

Dilution Control and Buybacks

SBC was €1.70B, or 4.6% of revenue, versus about €2.69B, or 7.9%, in 2024. Of that amount, €1.33B was equity-settled and €364M cash-settled. This is meaningful, but considerably less burdensome than at many high-growth SaaS companies. Weighted average basic shares remained at 1.166B in both 2024 and 2025, indicating that repurchases broadly prevented dilution rather than meaningfully reducing the share base. Q1 2026 weighted average shares declined to 1.163B, before the full impact of the latest buyback tranche became visible, which objectively appears favourable. Investors should continue tracking per-share free cash flow rather than celebrating buybacks based only on their gross euro value.

Free Cash Flow

Cash Conversion Strength

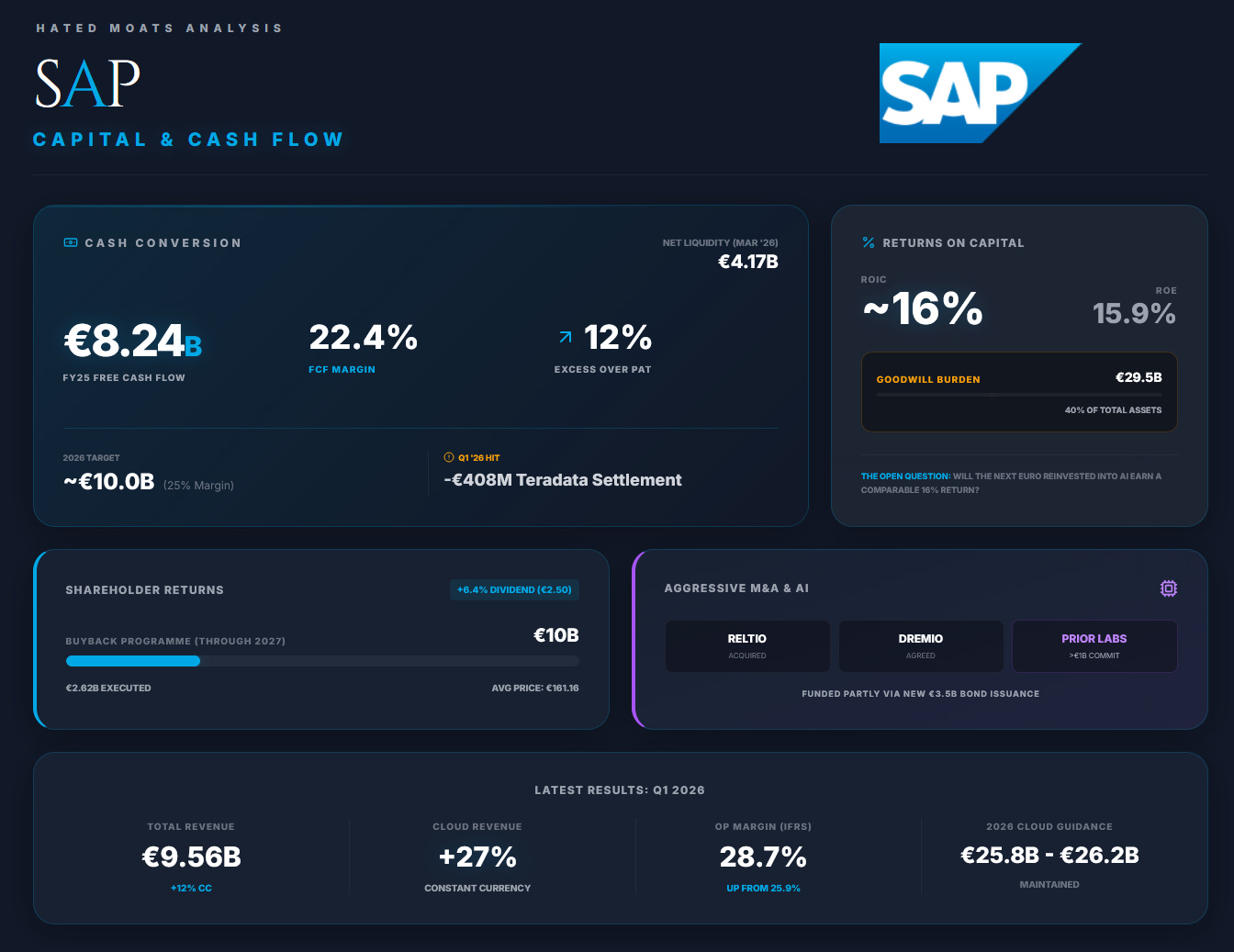

FCF is one of SAP’s strongest fundamental attributes. Operating cash flow rose 76% to €9.16B in 2025. SAP’s FCF definition subtracts capital expenditure and lease payments and adds proceeds from asset disposals, producing €8.24B of FCF and a 22.4% margin. FCF exceeded reported profit after tax by approximately 12%, indicating strong cash conversion. Low physical capital requirements, advance customer billing, and contract-liability growth all support the model.

Normalisation and One-Off Impacts

We shouldn’t annualise the 2025 improvement blindly, though. Operating cash flow benefited from restructuring payments falling from €2.5B to €0.8B and cash payments for SBC declining from €1.3B to €0.8B. Those improvements were real, but largely represented normalisation after an unusually expensive 2024. Q1 2026 FCF fell 9% to €3.25B, mainly because SAP paid €408M to settle the Teradata litigation. Excluding that payment, quarterly cash generation would’ve increased. Management continues to expect approximately €10B of FCF in 2026, which would imply a margin close to 25% based on current consensus revenue.

Balance Sheet and Capital Allocation

SAP ended 2025 with €3.38B of net liquidity before leases and €1.70B after leases, rising to €4.17B by March 2026. The balance sheet remained strong enough to support dividends, buybacks, acquisitions and investment.

Aggressive M&A & AI Investment

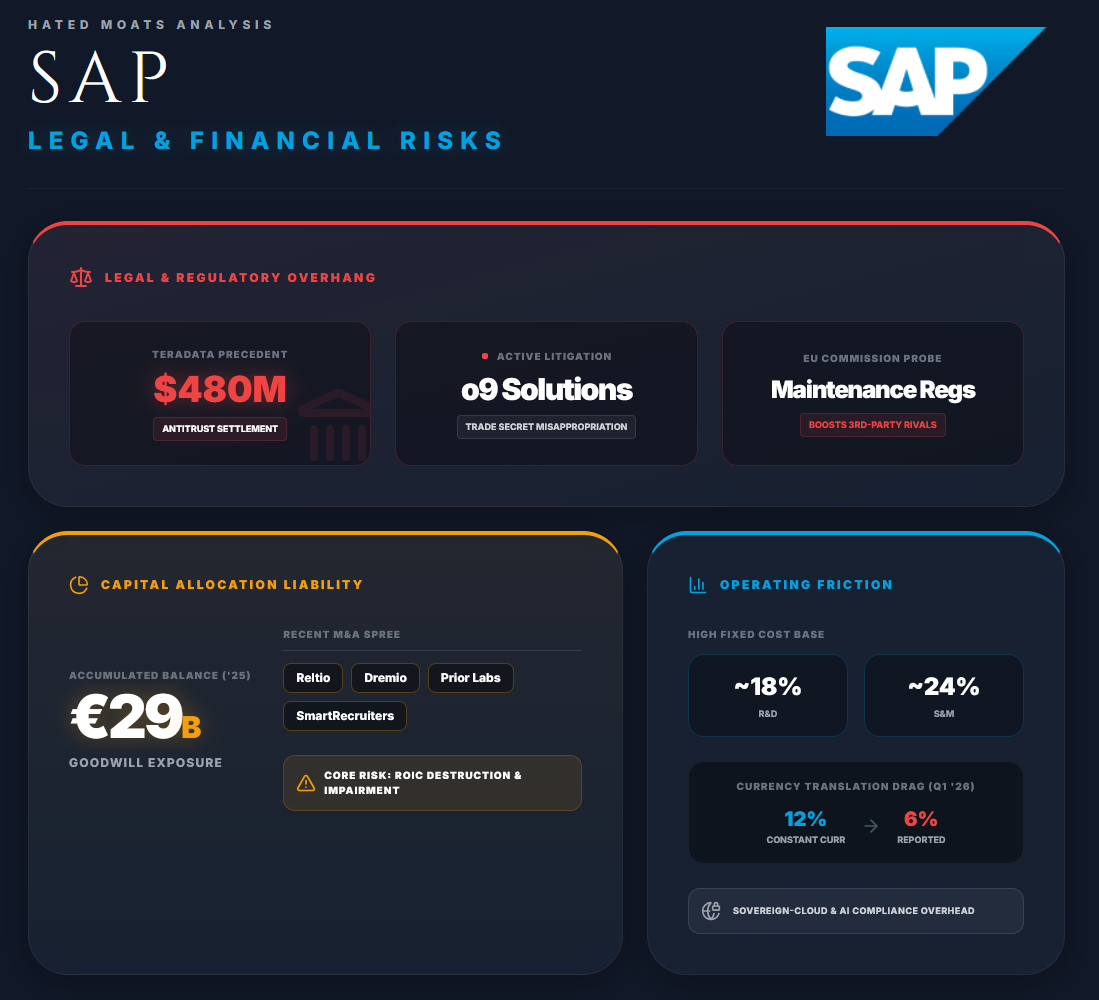

Capital allocation has become more aggressive. SAP completed the Reltio acquisition, agreed to acquire Dremio and Prior Labs, committed more than €1B to Prior Labs over 4 years after closing, and issued €3.5B of bonds partly to fund recent deals. SAP remains investment-grade, but management is now deploying more capital into data and AI rather than simply accumulating cash.

Shareholder Returns & Buyback Value

SAP also raised its FY2025 dividend by 6.4% to €2.50 per share and launched a buyback of up to €10B through 2027. The first tranche repurchased 16.28M shares for €2.62B at an average price of €161.16, above the share price at the time of publishing this analysis (€140 per share). The longer-term value depends on whether those shares are permanently retired or later reissued for compensation.

Goodwill Burden

Goodwill reached €29.49B in Q1 2026, around 40% of total assets. This poses no immediate balance-sheet risk, but reflects substantial acquisition spending and should remain part of any assessment of management’s capital-allocation record. No goodwill impairment was recorded in 2025, although adjusted earnings exclude acquired-intangible amortisation.

Returns on Capital

SAP generated approximately 15.9% ROE in 2025, using profit attributable to SAP shareholders and average parent equity. A rough after-tax ROIC calculation, including goodwill and using average equity plus net debt, also lands around 16%. These returns comfortably exceed a reasonable cost of capital and aren’t being manufactured through leverage. Excluding goodwill would produce a much higher number, but that would give management credit for acquisitions without charging the capital used to complete them.

The direction of returns matters more than one year’s figure. Cloud subscriptions should increase customer lifetime value and spread product-development spending across a larger revenue base. Conversely, acquisitions, hyperscaler commitments, and AI infrastructure consume capital before their returns become visible. SAP’s existing business generates excellent returns. The open question now is whether the next euro reinvested into AI and data products earns a comparable return.

Latest Results and Guidance

Q1 2026 reinforced SAP’s strategic progress. Revenue reached €9.56B, up 6% reported and 12% at constant currencies. Cloud revenue grew 19% and 27%, while Cloud ERP Suite revenue rose 23% and 30%, respectively. Current cloud backlog increased 20% reported and 25% at constant currencies to €21.93B. IFRS operating profit rose 17% to €2.74B, lifting the margin from 25.9% to 28.7%.

The quarter was less clean beneath the surface. Cloud growth benefited from temporary factors, management warned of slower Q2 growth, and operating profit gained €135M from lower SBC. Currency reduced reported revenue growth by about six percentage points and was expected to lower full-year cloud and cloud-and-software growth by around 1.5 points.

SAP maintained guidance for 2026 cloud revenue of €25.8B to €26.2B, cloud and software revenue of €36.3B to €36.8B, and non-IFRS operating profit of €11.9B to €12.3B. The outlook implies further margin expansion, although total revenue growth is expected to remain near the 2025 constant-currency rate rather than accelerate.

Valuation overview and Key ratios

At SAP’s 2 July closing price of €141.72 and using approximately 1.16B shares, its equity value was about €164B. Based on audited FY2025 results and year-end net liquidity, the stock traded at approximately:

The figures remain approximate because buybacks, acquisitions and subsequent financing have changed the share count and net-liquidity position.

SAP’s 2 July consensus estimates for FY2026 were €40.15B of revenue, €11.93B of non-IFRS operating profit, €7.18 of basic non-IFRS EPS and €9.99B of FCF. The shares therefore traded at roughly 20x forward earnings and 16.5x forward FCF, implying a prospective FCF yield of about 6.1%. The valuation from this point of view isn’t distressed, but no longer assumes flawless execution.

The key question is whether FY2025 FCF was sustainable or mainly a post-restructuring rebound. Lower restructuring and compensation payments materially helped the €8.24B result, but SAP’s approximately €10B guidance and expanding contracted revenue still point to further cash-flow growth.

Summary of Fundamental Analysis

SAP’s fundamentals are improving. Cloud ERP Suite growth remains strong, backlog provides visibility, gross margins are stable, and operating leverage is emerging. Cash conversion and the balance sheet also remain solid despite heavier investment.

The main weakness is the decline in support and licence revenue. Cloud growth more than offsets it, but limited customer-level disclosure makes it difficult to separate successful migration from attrition. We advise to focus on non-IFRS operating growth, FCF per share and margin progression rather than the sharp IFRS rebound:

Top 5 strengths

cloud ERP Suite growth

a highly predictable contracted revenue base

enormous backlog

strong cash conversion

high returns on capital without material financial leverage.

Main concerns

accelerating support decline

limited disclosure of retention and migration cohorts

currency exposure

increasingly aggressive AI and data investment

the risk that acquisitions or buybacks produce inadequate returns.

Key KPIs to monitor

Cloud revenue growth

Cloud ERP Suite growth

current cloud backlog growth

software-support decline

non-IFRS operating margin

FCF per share

actual share-count reduction

Single biggest question

Can SAP sustain cloud growth and operating leverage at a level that more than offsets the decline of its legacy support business, while earning attractive returns on the billions now being invested in AI, data, acquisitions, and buybacks?

Management Quality & Insider Activity

SAP’s management has largely delivered what long-term owners should expect, i.e. protecting the core franchise, accelerating the cloud transition, improving profitability and maintaining a strong balance sheet. Our view is positive, although not without reservations.

Since becoming sole CEO in 2020, Christian Klein has simplified the portfolio, completed a major restructuring and repositioned SAP around cloud, data and business AI. Cloud revenue rose from €8.7B in 2021 to €21.0B in 2025, more predictable revenue increased from 75% to 86%, and free cash flow reached €8.2B.

But the record isn’t flawless. SAP incurred more than €3B of restructuring charges in 2024, customer satisfaction missed management’s target in 2025, and communication around backlog growth and guidance contributed to the January sell-off. Management must still prove that cost discipline isn’t weakening customer experience or product execution.

Capital allocation now deserves closer scrutiny. Selling Qualtrics helped refocus SAP, but the Reltio acquisition and proposed Dremio and Prior Labs deals must ultimately deliver adoption, revenue and attractive returns. Klein’s €16.2M compensation package is largely performance-linked, although the €20M ceiling remains high.

Insider ownership is modest, but recent activity is encouraging. As ew mentioned above, CFO Dominik Asam bought about €1.02M of shares and also, COO Sebastian Steinhäuser around €349,000 after the January sell-off. Later sales were mainly tax-related.

Overall, management quality appears above average. The next test is whether heavier spending on AI, data, acquisitions and buybacks creates durable per-share value.

Intrinsic valuation & DCF

We performed a thorough and detailed DCF analysis of the company in one of our DCFriday analysis series.

You can read the whole valuation article with assumptions and methodology here:

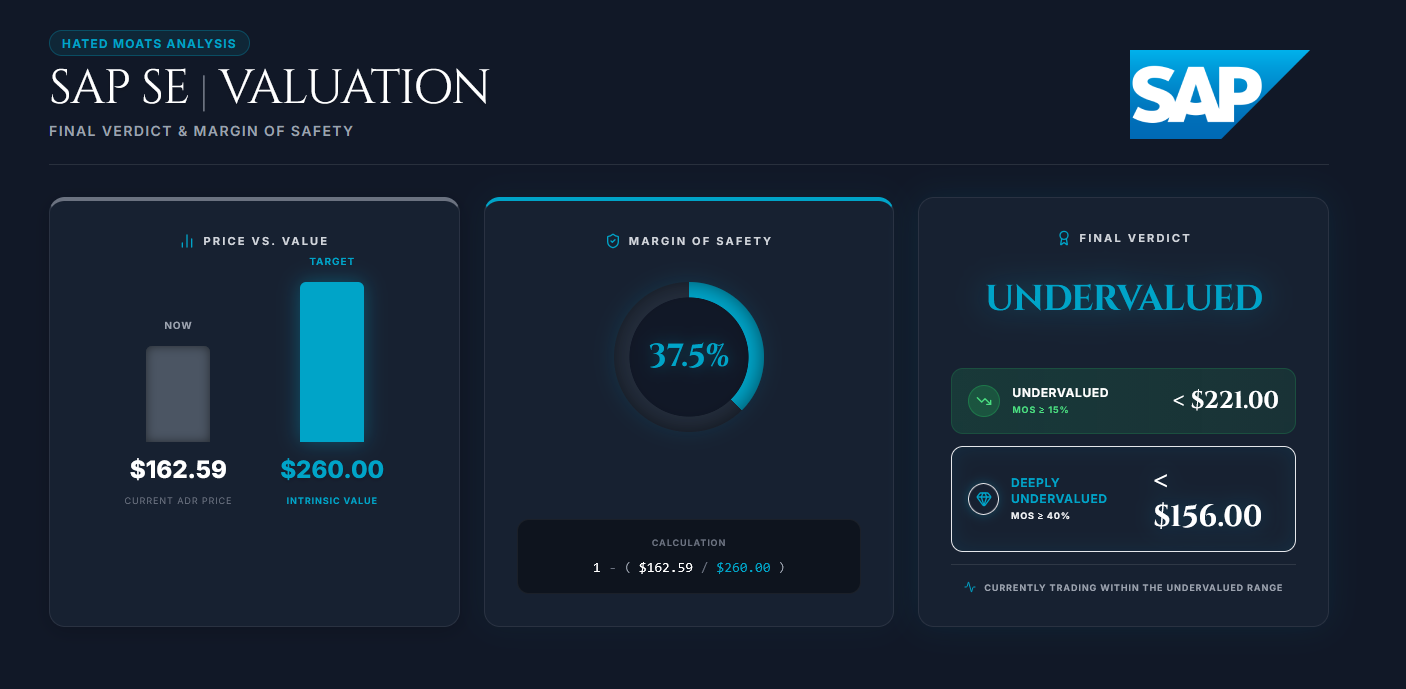

The updated verdict as of July 2, 2026 close (ADR price):

Date of Original Analysis: June 22 - 26, 2026

Current Verdict: Undervalued

Current Price Target (Base Case): $260

Price at the Time of Update: $162.59

Risk Factors

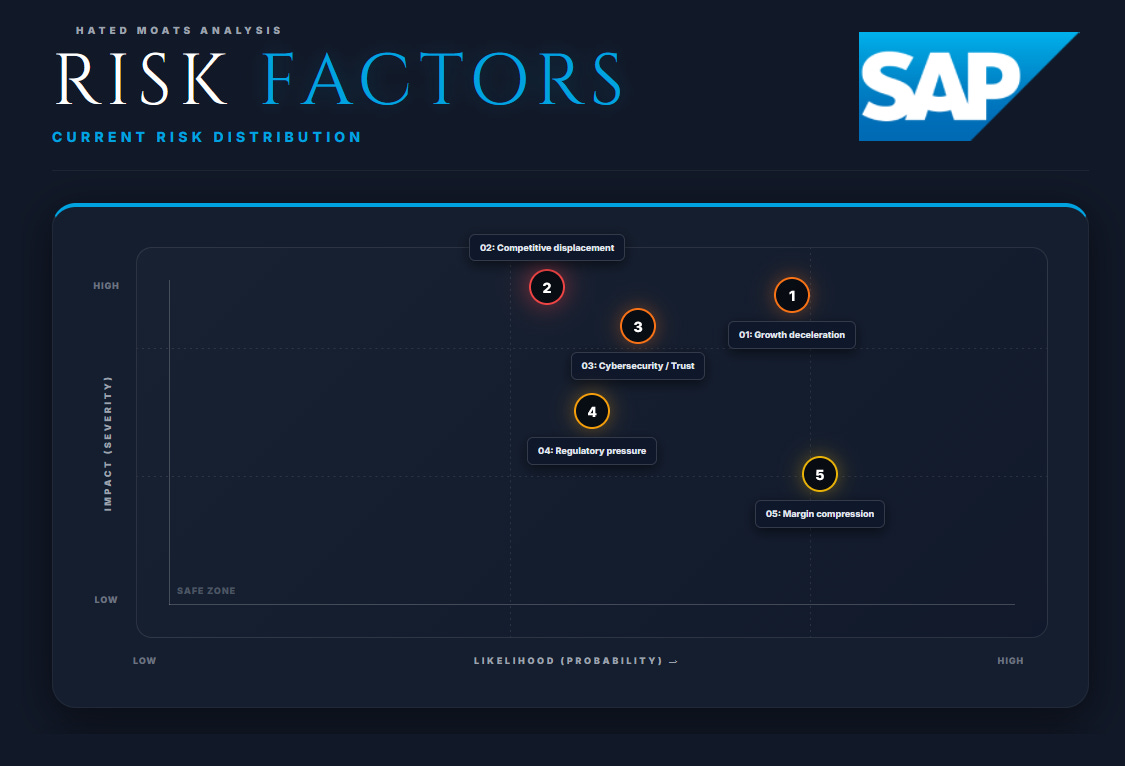

SAP’s main risks are execution-related. The company must move a vast on-premise customer base to the cloud while defending its position against Oracle, Microsoft, Workday, Salesforce, hyperscalers, and AI-native competitors. It must do so without alienating customers, weakening margins, losing control of the enterprise interface, or causing operational failures. They’re not in the perfect storm scenario, performance-wise, but execution-wise, it surely feels like navigating through one.

SAP’s Form 20-F highlights similar risks, including cloud execution, implementation, partner dependence, cybersecurity, competition, regulation, innovation, and acquisition integration. Let’s have a detailed look on them:

Cloud Transition & Operating Execution

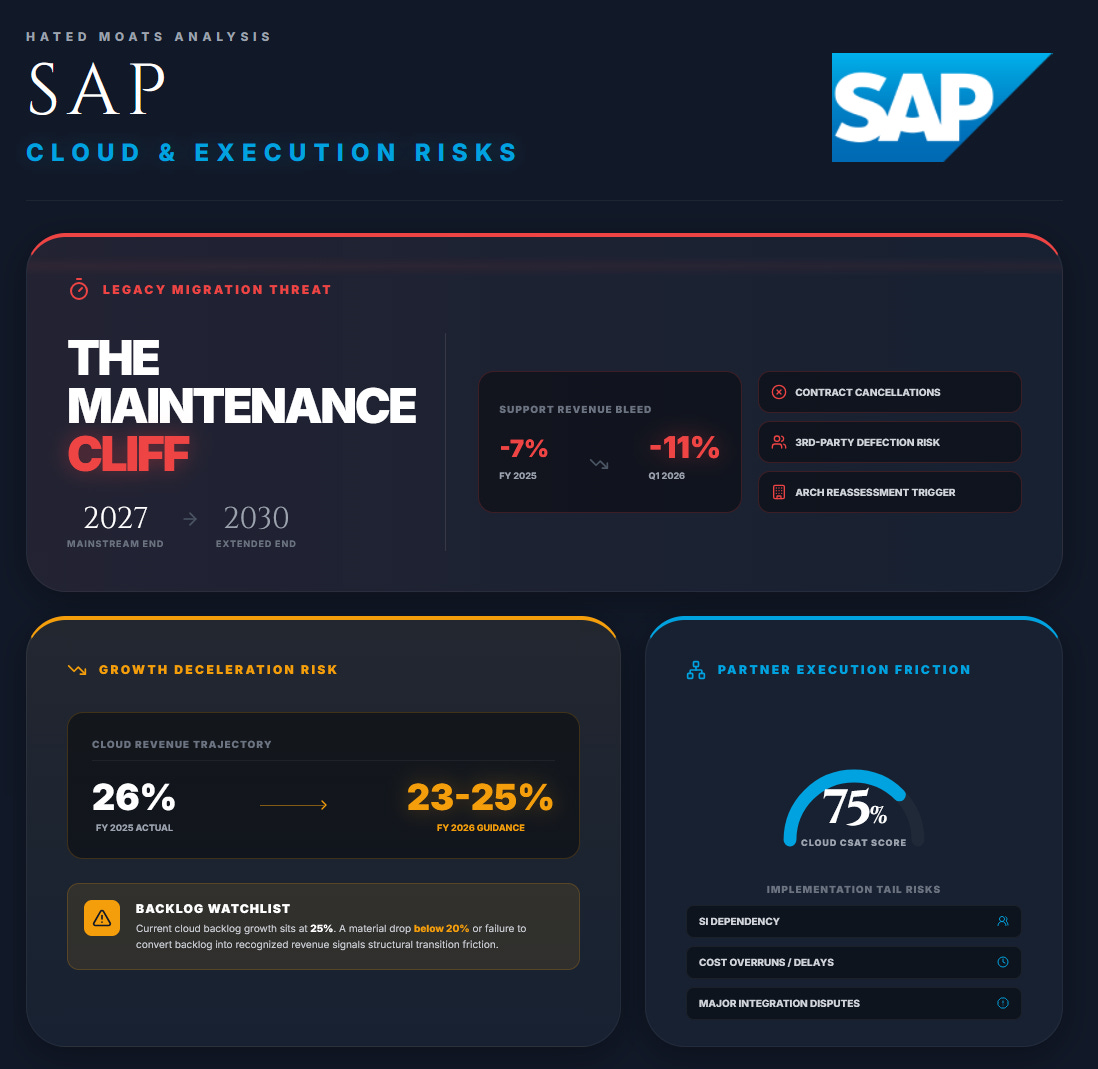

Cloud growth deceleration

FY2025 cloud revenue grew 26% at constant currencies, while 2026 guidance calls for 23% to 25%. Management also expects current cloud backlog growth to slow slightly from 25%. Q1 2026 remained strong, with cloud revenue up 27% and backlog up 25%, so the main concern hinges on whether deceleration becomes structural.

Large contracts can ramp slowly, while termination rights may limit backlog inclusion. This can increase volatility even when total contract value remains healthy. Warning signs here would include backlog growth falling materially below 20%, lower cloud guidance, or backlog failing to convert into revenue.

Legacy migration risk

SAP Business Suite 7 mainstream maintenance ends in 2027, with extended maintenance through 2030 and a conditional transition option for certain complex customers through 2033. These deadlines encourage migration, but also give customers an opportunity to reconsider their architecture and vendor.

Support revenue fell 7% in 2025 and 11% in Q1 2026. That is manageable if customers move into SAP cloud contracts, but more concerning if they cancel, delay migration, or choose competitors or third-party support. Investors should compare the support decline with Cloud ERP Suite growth.

Implementation & partner execution

SAP migrations can take years and depend heavily on systems integrators and customers. Delays, cost overruns, poor integrations, or failed implementations can damage trust even when SAP isn’t solely responsible.

RISE, standardised tools and SAP’s partner ecosystem reduce this risk, but the 75% Cloud Customer Satisfaction score leaves room for improvement. Key warning signs here include lower satisfaction, higher implementation provisions, major disputes, and customers extending legacy support instead of migrating.

Competition, AI, & Technological Disruption

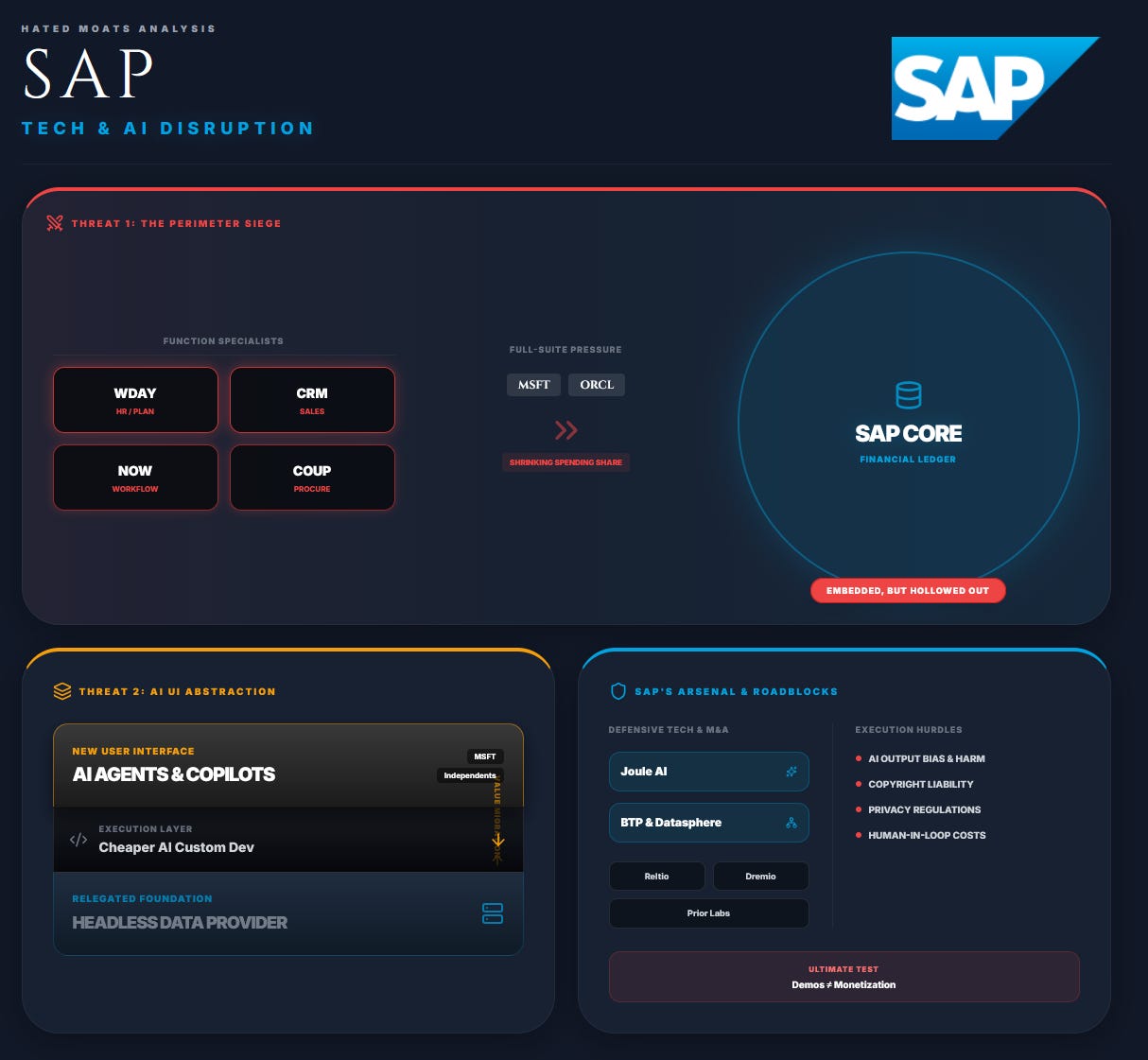

SAP faces full-suite competition from Oracle and Microsoft, while Workday, Salesforce, ServiceNow, Coupa and specialists attack individual functions such as HR, CRM, workflow and procurement.

The main risk is gradual loss of scope rather than wholesale replacement. Customers may retain SAP as their financial system of record while moving planning, analytics, procurement, HR and the employee interface elsewhere, leaving SAP embedded but capturing less spending.

AI could strengthen SAP because enterprise agents require trusted data, permissions, business context and access to transactional systems. Conversely, Microsoft, Oracle or independent agents could control the user interface, reducing SAP to the underlying system of record. Cheaper AI-assisted development may also allow customers and integrators to build functionality previously purchased as SAP modules.

SAP is responding to this through Joule, Business Data Cloud, Business Technology Platform and data and AI acquisitions. It completed Reltio acquisition in May 2026 and agreed to acquire Dremio and Prior Labs, strengthening its capabilities while adding integration and return-on-capital risk.

SAP also acknowledges that AI can produce biased, harmful or legally problematic outputs. Privacy, copyright, automated-decision rules and human-review requirements could delay adoption or increase costs. The strategy succeeds only if AI generates measurable usage and revenue, rather than merely appearing in demonstrations or contracts.

Cybersecurity, Cloud Reliability, & Trust

Cybersecurity is among SAP’s highest-impact tail risks because its products process financial records, payroll, manufacturing, procurement and sensitive employee data. A severe outage, data corruption event or exploited vulnerability could disrupt many customers simultaneously and damage SAP’s core promise of reliability.

“CVE-2025-42957” illustrates the risk. The critical S/4HANA vulnerability affected private-cloud and on-premise versions and allowed an authenticated, low-privileged user to inject code, potentially gaining full control of the system. Limited exploitation was reported before all customers had patched.

SAP provided a patch, but remediation still depends on customers patching on-premise systems and coordinating private-cloud maintenance promptly. SAP also relies on hyperscalers, subcontractors and acquired technologies, whose failures may affect SAP’s services even when it’s not the original source.

SAP states that the company and its partners have experienced cyberattacks, although none had materially affected its business as of the 2025 Form 20-F. Its controls include central security governance, vulnerability scanning, patch management, incident response, third-party oversight and board supervision. These measures reduce risk but cannot eliminate zero-day vulnerabilities, human error or supply-chain attacks. The variables that should be monitored thus include critical vulnerabilities, remediation speed, cloud availability and any disclosure of a material incident.

Regulatory, Legal, & Data-Governance Risk

The European Commission is investigating SAP’s on-premise maintenance practices, including restrictions on cancelling support for unused licences, using competing support providers and returning to SAP without reinstatement or back-maintenance fees.

SAP has offered commitments to ease switching between support providers, clarify fees, allow greater flexibility over unused licences and abolish reinstatement charges. The proceeding remained open in the Commission’s May 2026 report. If accepted, the commitments could resolve the case without an infringement finding or fine, although they may strengthen third-party support competition during the legacy migration.

The Teradata case(a high-profile legal dispute where Teradata sued SAP, accusing it of trade secret misappropriation, antitrust violations, and copyright infringement) is resolved. SAP agreed in February 2026 to pay $480M to settle all outstanding antitrust and intellectual-property litigation. The cost is manageable, but shows that supposedly non-recurring legal matters can still consume real cash.

We need to note here that a trade-secret lawsuit from o9 Solutions remains unresolved. It alleges that 3 former executives took confidential supply-chain software information to SAP. These are unproven allegations, but an adverse outcome could bring damages, injunctions, reputational harm or disruption to SAP’s planning products.

Privacy, data localisation, sanctions and AI regulation create further risk across jurisdictions with conflicting rules on data residency, international transfers and automated decisions. Sovereign-cloud products may help, but add infrastructure complexity and cost.

Financial, Currency, & Capital-Allocation Risk

SAP has substantial operating leverage. R&D represented about 18% of 2025 revenue and sales and marketing roughly 24%. Management expects 2027 operating-expense growth to equal 80% to 90% of revenue growth, so slower cloud growth or weaker cost control would pressure the margin thesis.

Adjusted results also require care. SAP excludes acquisition-related charges, restructuring, specified regulatory and litigation costs, and certain investment gains or losses, but includes SBC in non-IFRS operating profit. The adjustments are individually reasonable, although acquisition amortisation and restructuring can recur.

Currency remains meaningful. Q1 2026 revenue grew 12% at constant currencies but only 6% as reported. Hedging can reduce short-term volatility, but can’t eliminate the underlying translation and economic exposure.

Capital allocation is becoming more aggressive. Goodwill stood at €29.0B at year-end 2025. SAP has since completed Reltio, while Dremio and Prior Labs remain pending and SmartRecruiters closed in 2025. Poor integration here could weaken margins, distract management or lead to impairments.

The balance sheet and free cash flow remain strong, so insolvency is not the concern. The real danger is deploying SAP’s cash into acquisitions, AI investment and buybacks that fail to generate sufficient per-share returns.

Risk-Matrix

Scores use a 1 to 5 scale, with 5 representing the highest probability or impact.

SAP’s risks are real, but appear to be mostly manageable. The highest-probability danger is slower cloud execution. The highest-impact danger is a cybersecurity or technological event that damages customer trust. We believe that the core thesis breaks if support revenue declines faster than cloud economics mature, while AI and competitors gradually reduce SAP’s control over enterprise processes.

Our Scenarios (3-5 Year Horizon): Bull, Base, Bear Case

We use a 3-5 year convergence horizon to assess whether SAP can migrate its installed base, offset declining support revenue and monetise AI. The DCF runs through 2035, but the values below are estimates of current intrinsic value. The CAGRs show annualised price appreciation from the $155.09 reference price, excluding dividends.

Bull Case (25% Probability)

Key Assumptions

Customers move from ECC to S/4HANA Cloud through RISE while adopting adjacent products with limited competitive losses. Joule and SAP’s broader AI stack improve pricing, module adoption, customer productivity and internal efficiency. SAP doesn’t need to dominate AI globally. AI and suite consolidation must deepen its role in customer operations.

Financial Outcomes

The model assumes an 8.4% revenue CAGR through 2035, a 36.5% terminal IFRS EBIT margin and 3.0% terminal growth. This produces an estimated value of $349 per ADR, representing approximately 115% upside and annualised price appreciation of 29.0% over 3 years or 16.5% over 5 years.

Base Case (55% Probability)

Key Assumptions

Cloud growth slows with scale but remains sufficient to offset declining licence and support revenue. Migrations remain lengthy, while AI supports retention, automation and cross-selling without becoming a separate hypergrowth engine. Margins expand as operating expenses grow more slowly than revenue. This outcome requires solid execution, customer retention and sustained margin improvement.

Financial Outcomes

The model assumes a 6.9% revenue CAGR through 2035, a 33% terminal IFRS EBIT margin and 2.5% terminal growth. This produces an estimated value of $260 per ADR, representing approximately 60% upside, with the shares trading about 37.5% below estimated value. Annualised price appreciation is 16.9% over 3 years or 9.8% over 5 years.

Bear Case (20% Probability)

Key Assumptions

Migrations take longer, support revenue declines faster than cloud revenue replaces it, and competitors capture more adjacent workloads. AI shifts the user interface towards Microsoft, Oracle or independent agents. Cloud infrastructure, acquisitions, sovereign-cloud investment and AI spending also constrain margin expansion. SAP remains strategically important, but captures less value from customer workflows.

Financial Outcomes

The model assumes a 4.1% revenue CAGR through 2035, a 25% terminal IFRS EBIT margin and 1.5% terminal growth. This produces an estimated value of $141 per ADR, implying approximately 13.3% downside and annualised price depreciation of 4.6% over 3 years or 2.8% over 5 years.

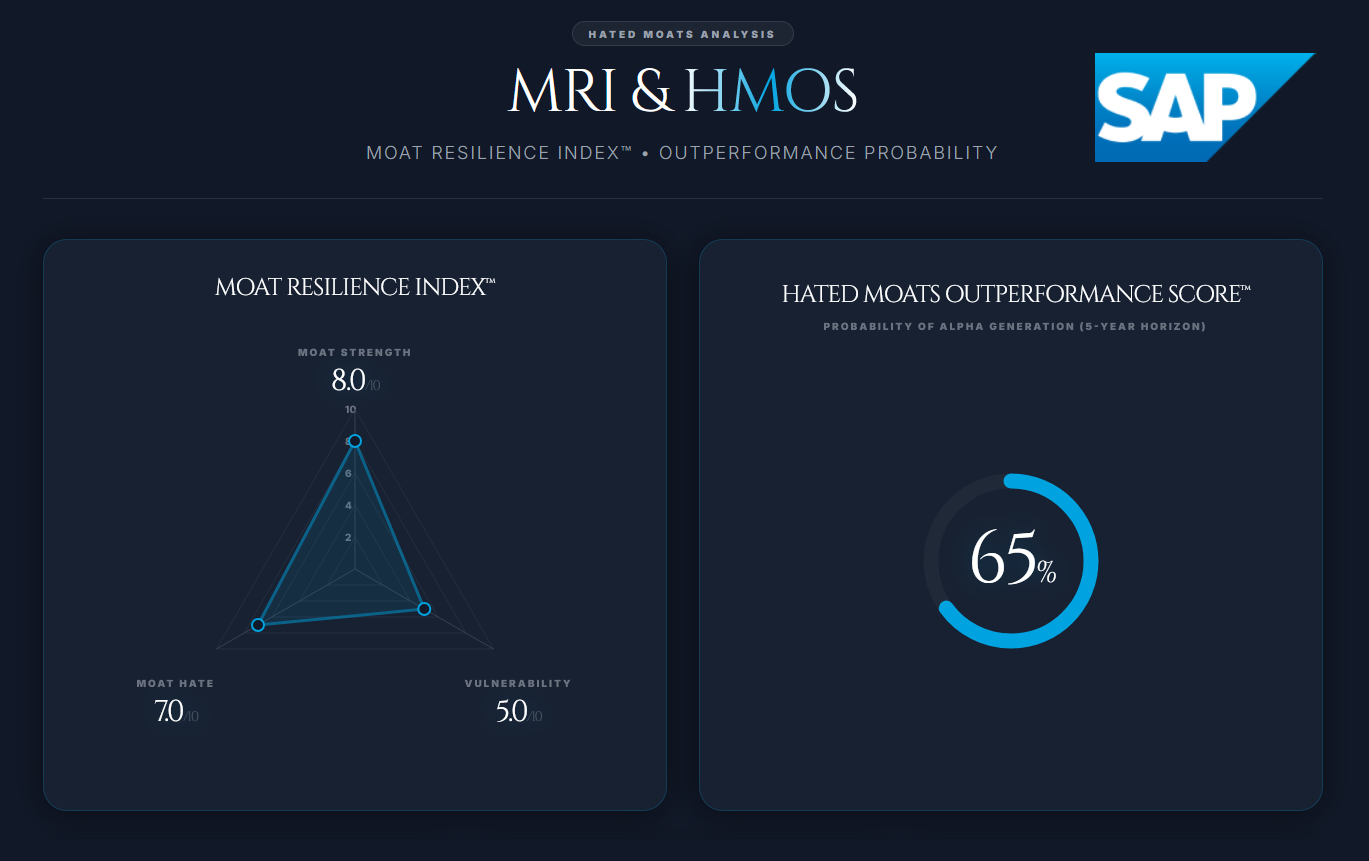

Moat Resilience Index™ (MRI)

Moat Strength: 8/10

SAP’s moat rests on high switching costs, operational centrality, industry-specific process knowledge and a large implementation ecosystem. Replacing its core systems can require years of migration, integration and retraining.

The score stops at 8.0 because cloud migrations give customers an opportunity to reassess their architecture, while competitors can capture adjacent products and the AI interface.

Moat Hate: 7/10

SAP has suffered a severe de-rating despite continued cloud growth, improving profitability and strong cash generation. Investors remain concerned about backlog deceleration, migration complexity, AI disruption and competition.

Sentiment is clearly weak, but the market has reduced its expectations rather than abandoned the company entirely.

Moat Vulnerability: 5/10

SAP’s core ERP position remains difficult to displace, but Oracle, Microsoft and specialist vendors can take adjacent workloads. AI agents could also weaken SAP’s control of the employee interface.

The main risk is gradual erosion of scope and pricing power rather than rapid replacement of the core platform.

Hated Moats Outperformance Score™ (HMOS): 65%

SAP receives an HMOS of 65/100, indicating a moderately favourable 5-year outperformance set-up rather than a statistically derived probability.

The opportunity rests on cloud conversion, margin expansion and successful AI monetisation. The principal risks are slower backlog growth, declining support revenue, competitive erosion and poor returns from acquisitions, AI investment or buybacks.

Conclusion

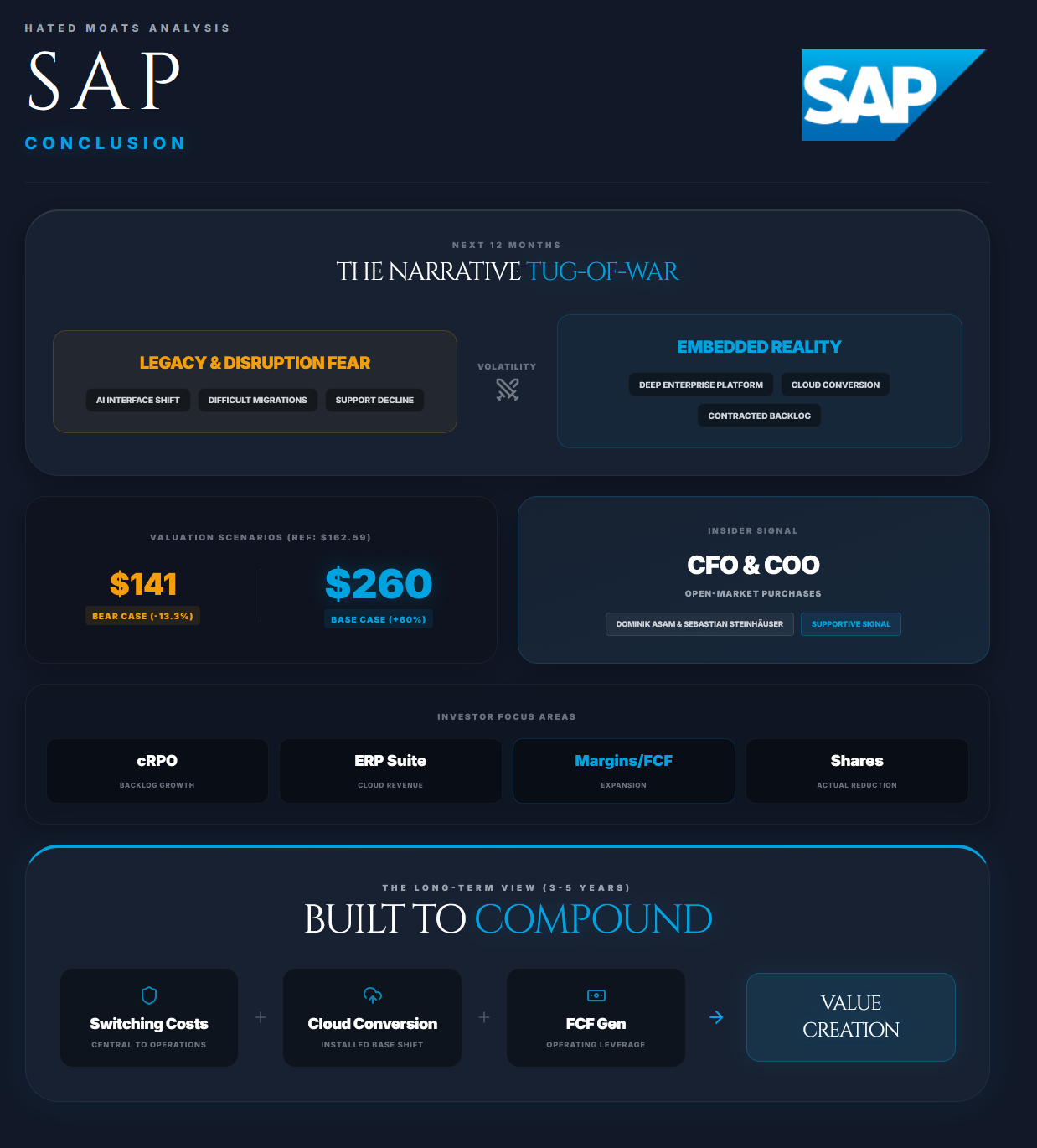

SAP remains caught between two narratives. On one hand, there is a deeply embedded enterprise platform successfully moving customers to the cloud, and on the other hand, there is a mature incumbent facing slower backlog growth, difficult migrations, competition and AI disruption. Near-term volatility is therefore likely to continue.

The long-term case rests on SAP’s switching costs, contracted backlog and ability to convert its installed base into cloud revenue and cash flow. It doesn’t need to control every enterprise-software layer, but it must remain central to customers’ financial, operational and data processes.

The main risk is that declining support revenue, lengthy migrations and competitive losses offset cloud growth. AI could deepen SAP’s role through Joule and its data platform, or shift the employee interface towards Microsoft, Oracle and independent agents.

At the $162.59 reference price, the $260 base-case value implies 60% upside. The $141 bear case implies 13.3% modelled downside, but outcomes could be materially worse if execution, cybersecurity or acquisition returns disappoint.

Management has improved cloud growth, profitability and cash generation. Open-market purchases by CFO Dominik Asam and COO Sebastian Steinhäuser provide a supportive, although not decisive, signal.

WE believe investors should focus on current cloud backlog growth, Cloud ERP Suite revenue, support decline, operating margins, FCF per share, customer satisfaction and actual share-count reduction.

Final Verdict: BUY

SAP qualifies as a Buy, although not a Strong Buy. Its business quality, switching costs, cash generation and valuation support a positive 3 to 5-year outlook. Cloud execution, AI uncertainty, migration risk and increasingly aggressive capital allocation limit our conviction.

We also remain concerned that SAP doesn’t disclose some of the important KPIs (company-wide retention, net revenue retention, cloud customer counts or migration-cohort data), limiting visibility into the health of the crucial cloud transition.

Despite the Buy rating, the main author held no personal position at publication of this article because of private portfolio constraints/structure and limited available capital. However, we are still considering trimming some positions in our Hated Moats Fund, and gain an exposure to SAP in this way.

Our verdict remains BUY and we do believe SAP offers a compelling opportunity for investors who believe in the bull, or even the base case scenarios. The market appears to be pricing SAP as if its moat is weakening faster than the evidence currently suggests. We believe that view is too pessimistic, but SAP still has to prove it.

Disclaimer & Our Investment

The author of this report does not hold a position in the security of SAP SE. This report is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

this is good. i also covered SAP but i believe something you forgot to cover was the cloud backlog growth decel which management highlighted in earnings...but valuation wise it is cheap. well done

A quality product, SAP is on my watchlist and should the price continue to drop I may soon open a position