Wix: Deep Dive Analysis

The market is pricing Wix like a melting ice cube while the business is still compounding cash flow and buying back stock massively. Will AI really disrupt this business?

Overview & Positioning

Wix.com Ltd ( WIX 0.00%↑ ) is a leading global SaaS platform for creating and managing websites and online services, catering primarily to individuals, small businesses, and increasingly agencies and enterprises. Founded in 2006 in Tel Aviv, Wix has evolved from a do-it-yourself website builder into a comprehensive “operating system” for online presence. Its offerings include Wix Editor and Wix Studio (design platforms), e-commerce and payment solutions, marketing and SEO tools, a third-party App Market, and new AI-driven products like Wix Harmony (Wix’s flagship AI website builder / hybrid editor combining vibe coding with visual editing). This breadth positions Wix as a one-stop solution for users to design, host, and grow their digital presence without deep technical skills. The company’s mission of “democratising web development” remains central, now extended to AI. Its Base44 (June 2025) acquisition brings natural-language “vibe coding” capabilities, aiming to let users build web applications through ChatGPT-style prompts. With around 293 million registered users globally (and millions of paying subscribers), Wix entered 2026 at an inflection point, i.e. transitioning from a pure website builder to an AI-enhanced web creation platform.

In short, Wix’s positioning leverages a strong brand in the DIY website space and a decade-plus track record of steady growth, now augmented by aggressive moves into AI tools and higher-end customer segments (agencies via Wix Studio, developers via Velo). The company’s value proposition is broad functionality with low complexity, enabling customers to go from blank page to fully functional site or app, backed by Wix’s cloud infrastructure and support.

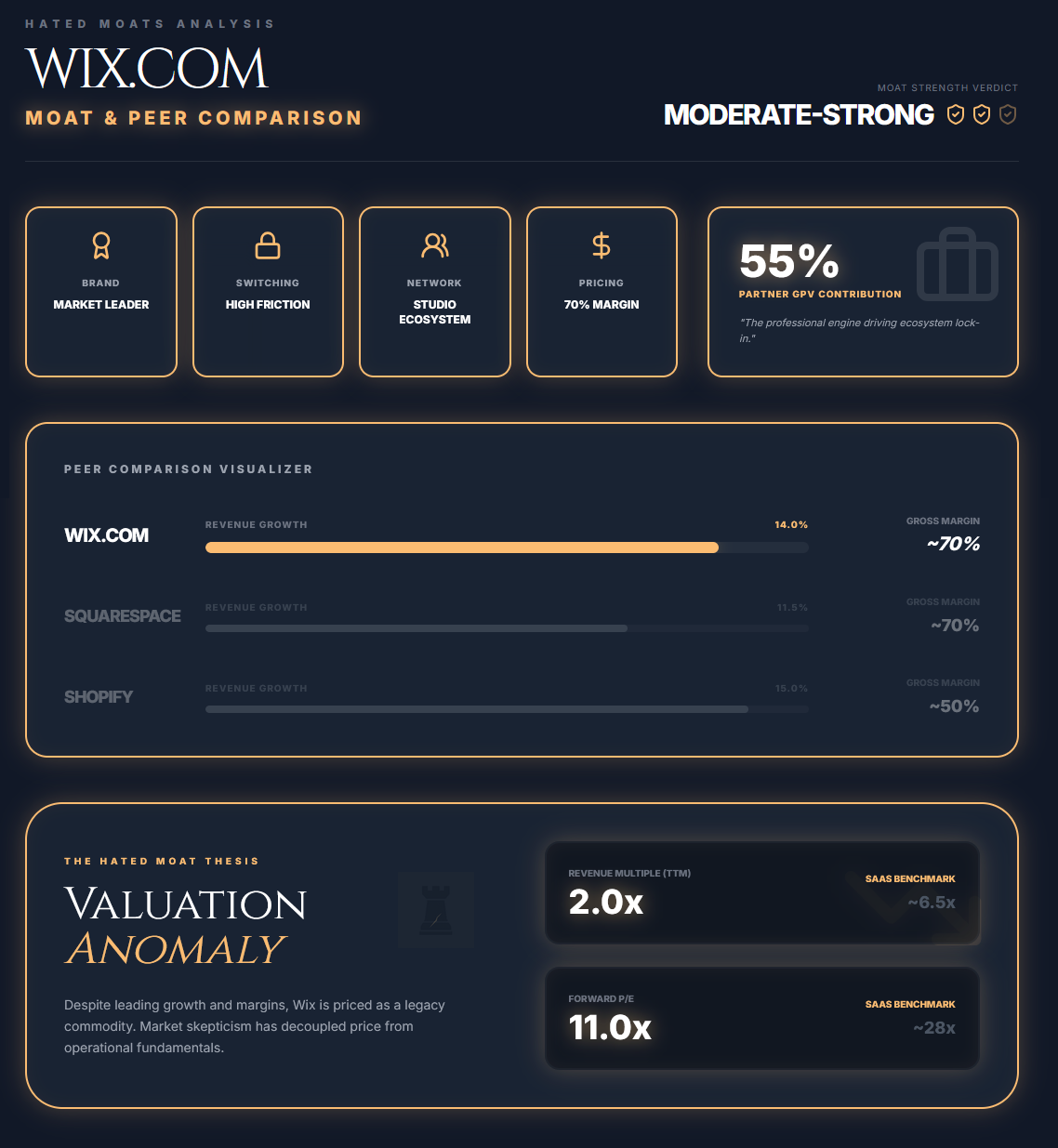

Competitive Moat & Peer Comparison

Wix benefits from several sources of competitive advantage. First is its brand recognition and scale in the website builder market. With hundreds of millions of users, “Wix” has become synonymous with easy website creation, giving it strong mindshare among small businesses and creators. This drives a powerful network of templates, apps, and partner developers. Wix’s App Market and developer platform (Velo) encourage third-party integrations, making the ecosystem richer and stickier for users. Wix has also nurtured a community of agencies and freelancers who build sites for clients on Wix (the “Partners” channel). By early 2025 commentary around FY2024 results, Wix leadership cited “over 2 million Studio accounts,” reflecting rapid adoption among professionals (“partners”). Partners are a major driver of Wix’s commerce activity. For example, in Q3 2025 Partners contributed roughly 55% of GPV. That is a significant network effect that funnels professional clients to Wix. Combined with high switching costs (migrating a website to another platform can be time-consuming and disruptive for a business), this gives Wix a moderate moat around its core business. Financially, the moat is evident in high gross margins (68% GAAP) and recurring revenue streams, which are hallmarks of a SaaS platform with pricing power.

As far as competition goes, Wix’s closest public comparable is Squarespace (formerly NYSE: SQSP), which was taken private after Permira completed its acquisition on Oct 17, 2024, another DIY website/commerce platform. Squarespace, though smaller, has also grown double-digits but focuses more on design-centric customers. We note that comparisons to Squarespace should note Squarespace is now private but if we do so, Wix is expanding into higher-value services more aggressively. Shopify ( SHOP 0.00%↑ ) is sometimes seen as a competitor in the sense that it provides web storefronts, but Shopify’s focus is e-commerce / transaction volume, whereas Wix serves a broader range of sites (including content, portfolios, etc.). Shopify’s revenue base is larger but Wix’s website-centric approach fills a different niche. WordPress (open-source software/ecosystem) is a major alternative. Automattic operates WordPress.com (a hosted WordPress service) and is a major contributor to the broader WordPress ecosystem, but it lacks Wix’s all-in-one hosting and support. Many non-technical users prefer Wix’s fully managed SaaS model. GoDaddy ( GDDY 0.00%↑ ) is a company that offers domains, its own site-building and commerce tools. Its builder is generally positioned as simpler than Wix’s broader platform.

In terms of competitive positioning, Wix has established a strong spot among self-service and small-business clients who want richer design capabilities than very basic tools (GoDaddy, Weebly) but more simplicity than coding from scratch or managing WordPress. By launching Wix Studio (targeting professionals) and integrating AI (Base44, Harmony), Wix is also moving into territories traditionally served by custom developers or high-end SaaS (e.g. Adobe’s web design tools, or even low-code platforms). This strategy is meant to future-proof its moat. Rather than being disrupted by AI, Wix is embedding AI to make its platform indispensable for a new cohort of “prosumers” who are between no-code and full-code.

When we look at peer comparisons in financial terms, Wix’s valuation has compressed significantly, making it cheaper than most peers on fundamentals. At $87 per share, Wix trades around 2x TTM revenue, far below typical SaaS peers. Wix’s forward P/E of 10-11 is also low for a profitable software company. This reflects market scepticism (discussed below).

Operationally, Wix’s 14% YoY revenue growth in Q3 2025 slightly outpaces Squarespace’s 11-12% (2025E) and is in the same ballpark as Shopify’s post-COVID normalised growth. Wix enjoys up to 70% gross margins (typical for software), similar to Squarespace, though Shopify’s are lower (50% gross margin) due to heavy merchant services. Wix’s moat versus peers comes down to its breadth (it combines what might require multiple plugins on WordPress), ease-of-use, and now a first-mover push into AI-enhanced site building. However, there are certainly threats present and generally this is not the most robust category of moat. Open-source or big-tech AI tools could reduce the need for a platform like Wix (more on this risk later), and competitors like Squarespace and Shopify are also adding AI features. Overall, Wix’s competitive moat rates as moderately strong. Surely not impregnable, but solidified by its large installed base, extensive feature set, and increasing ecosystem lock-in.

Recent Stock Performance & Market Sentiment

2025 was a rollercoaster for WIX’s stock. After a strong run in late 2024 and early 2025 (the stock hit a 52-week high was about $246.76 in January 2025), sentiment reversed sharply. Shares fell about 51-52% in 2025, ending the year around $104. This collapse came despite the company meeting or beating financial targets. For instance, in Q3’25 Wix delivered 14% revenue growth (to $505M) and beat adjusted (non-GAAP) EPS expectations (about $1.68 vs consensus roughly $1.49-$1.46, depending on the estimate source). It even raised full-year guidance slightly. Normally a “beat-and-raise” sparks a rally, but Wix’s stock fell 21% in one day after Q3 earnings, despite a beat and slightly higher guidance. Did we hear Hated Moat?

Yes, we did. The market’s reaction underscores extremely negative sentiment overshadowing fundamentals. Investors fixated on two issues: One, near-term margin pressure from AI investments (and fears of AI being the disruptor on its onw), and two, delays in a flagship product launch. In Q3, Wix’s new AI-driven coding tool (Base44) was growing rapidly, but heavy marketing spend on it dented operating margins. Management also shifted more customers to monthly subscriptions (away from multi-year prepaids), which, while potentially boosting long-term value, hurt short-term visibility and worried investors about revenue predictability. Additionally, the CEO admitted a highly anticipated new product (the AI-powered Wix Harmony site builder) had to be postponed, saying he was “clearly unhappy” about delaying a flagship product from summer 2025 to 2026. This fed a narrative that Wix’s growth drivers were slipping, just as the market was looking for acceleration. The result was a rush for the exits. By November 2025, WIX was down roughly 50% YTD and trading at 14x forward earnings and 10x FCF, i.e. levels indicating scepticism about its growth and its moat.

Notably, macro and sector sentiment likely contributed to volatility, but we attribute the sell-off primarily to company-specific concerns cited around Q3 (AI spend/margins and the Harmony delay). Short interest in WIX stock climbed (recently 10-12% of float is short), reflecting traders betting on further declines or hedging. Among the retail investors, sentiment also soured, often echoing the “AI threat” theme, questioning if Wix could survive the rise of generative AI that might build websites autonomously. This dichotomy (strong results vs. fearful narrative) defines the stock’s recent story, and potentially presents an opportunity for Hated Moats.

Market sentiment has started to mend a bit in early 2026. Wix’s management took decisive action by the end of January. On Jan 28, 2026, the Board authorised a massive $2 billion share repurchase program. This is extraordinarily large (over 40% of Wix’s $4.8B market cap during the announcement) and signaled confidence. The response was generally positive, and Wix is generally getting Buy ratings (even while many analystts are trimming price targets, which many of still imply 90-100% upside from current levels. Furthermore, Wix successfully launched Wix Harmony (the delayed AI product) in January 2026, to add some positive buzz. The company even had a Super Bowl ad for Base44 (“It’s App to You”), a bold marketing move reminiscent of Wix’s earlier growth years. This has added to optimism that Wix is going on offense. Despite all of these positive signals, as of mid Febuary 2026, Wix is down over -30% YTD, since quite literally every company in SaaS environement is getting hammered, priced like they should be replaced by an AI alternative within a year. And Wix is not exception here, tanking just as ugly.

Overall, while 2025’s market sentiment was extremely bearish, 2026 is opening with a more balanced view as far as fundamentals go, but continues in the carnage of stock price. The “AI disruption” worst-case still feeds the fear and sentiment remains fragile. Wix needs to prove that its AI-enhanced strategy can rekindle growth without eroding profitability. If it can, the stock’s depressed valuation provides significant upside, a point we turn to in the next part of our analysis.

Fundamental Analysis

Growth & Profitability

Despite the stock’s volatility, Wix’s fundamentals have been steadily improving. The business today is far stronger than a few years ago, with consistent double-digit growth, expanding margins, and robust cash generation. Below we break down key metrics.

Revenue Growth

Wix has maintained solid growth, indicating enduring demand for its platform. 2025 full-year revenue is expected around $1.99-2.00 billion, up 13-14%. In Q3’25, revenue was $505.2M (+14% YoY), with Creative Subscriptions (recurring SaaS fees) up 12% and Business Solutions (payments, e-commerce, etc.) up 18%. Notably, growth accelerated from earlier periods, partly thanks to strong new customer cohorts and Base44’s contribution. This reversed a prior slowdown and shows that Wix’s pivot to focus on higher-value customers (agencies, merchants) is paying off. Management raised 2025 bookings guidance to $2.06B-2.078B (+13-14% YoY), signaling confidence in continued momentum. For 2026, analysts and Wix’s internal model (base case) foresee low-to-mid teens growth as achievable, with AI features potentially reducing churn and boosting pricing power (i.e. customers will pay for more advanced functionality). Wix grew from $24.6M revenue in 2011 to $1.761B in 2024 ( +7,057% vs 2011). On the 2025 revenue guide of $1.99-$2.00B, that’s +8,000% vs 2011. While that pace naturally moderated, Wix has proven it can still find new avenues of growth (e.g. Partners channel, international expansion, and now AI-driven products). AI is thus not a bug but rather a feature in form of an opportunity for new path of growth.

User Base & Monetisation

Wix’s freemium model means many users start free and convert to paid. Wix ended 2024 with 6.2M total premium subscriptions. As of Q3 2025, Creative Subscriptions ARR was $1.457B. The company’s focus has shifted from simply adding users to increasing ARPU and lifetime value of each user. For example, “average bookings per subscription” rose 13% to more than $294 in 2024, driven by users adopting higher-tier plans and more business solutions. Also, net revenue retention improved to 100% in 2024 (meaning existing cohorts are spending at least as much as last year, offsetting churn). That’s a very positive metric for a mature SaaS. This indicates stable or expanding spend by customers, thanks to upsells like payments, email marketing, etc. Wix’s large funnel of 282M+ registered users (Dec 2024) is an asset on its own. Even slight improvements in conversion or upsell rates can drive growth for years. Google Trends data shows “Wix” maintaining strong search interest, and Wix’s own top-of-funnel remained “robust” through 2025, aided by marketing. In short, the user base is both growing in number and being monetised more effectively. Compare this to the popular “AI buzzword” noise, and we have an objective signal in front of us here, and we like this one a lot.

Profitability & Margins

Wix underwent a significant margin expansion initiative in recent years (partly prodded by activist investors like Starboard Value). This was a good move. In 2024 Wix achieved the “Rule of 40” (growth + FCF margin ≥ 40) a year ahead of schedule. For 2024, bookings grew 15% and non-GAAP operating margin reached 20%. Free cash flow was $478.1M in 2024 and excluding HQ build-out capex, FCF was $488.4M (28% of revenue). Entering 2025, management set a new goal of “Rule of 45” (combining growth and margin). Through 2025, Wix’s margins have remained healthy albeit with some temporary compression due to AI investments.

Gross Margin

Gross margin was 68% GAAP in Q3’25 (about 69% non-GAAP). This is slightly down from 70% in 2024, as the Base44 AI tool incurs cloud compute costs and its revenue (classified under Business Solutions) has lower margin (32% gross margin for Biz Solutions vs 83% for Creative Subscriptions). Management guided full-year 2025 non-GAAP gross margin 68-69%. While AI introduces some new costs (inference computing isn’t free), Wix expects these to normalise as scale grows, which we see as a healthy business assumption. Even at 68%, gross margin is robust, reflecting high software leverage you strive for with SaaS.

Operating Expenses

As far as operating expenses go, Wix drastically improved operating efficiency. In 2023, it implemented $150M cost cuts and reined in marketing spend. In 2024, Wix’s non-GAAP operating margin was 20% on a 69% non-GAAP gross margin, implying non-GAAP operating expenses of roughly 49% of revenue. In 2025, Wix did increase spending for AI and marketing. The company now expects opex to be 50% of revenue (non-GAAP), a bit higher than initially planned due to aggressive Base44 marketing (but still resulting in a hefty operating margin near 18-20%). Higher spend for AI (which is understandable and shows the company does not want to be left behind but rather innovate) aside, the trend of expenses is favourable in our view, sensibly trying to become leaner as the business matures. Notably, Wix is following a TROI (targeted ROI) methodology for marketing. They claim strong returns on Base44 marketing and thus are willing to spend more, which, again, is sensible. R&D is a major expense line. For example, in Q3’25 GAAP R&D was $172.0M on $505.2M revenue (i.e., 34%). Overall, Wix is balancing profitability with growth. It’s a highly FCF positive business while still investing in new tech.

Net Income and EPS

Wix historically reported GAAP net losses (due to heavy non-cash stock compensation and amortisation). However, in Q3’25 it was essentially break-even on a GAAP basis (net loss of only $0.6M). For full-year 2024, GAAP net income was $138.3M (diluted GAAP EPS $2.36). In Q3’25, GAAP net loss was $0.6M. Non-GAAP EPS (which excludes stock-based comp and one-offs) is much higher. Q3’25 diluted non-GAAP EPS was $1.68 (basic $1.80). Using non-GAAP earnings, Wix’s forward P/E is only 10-11x, well below software industry averages. The key point here is that Wix has crossed into real profitability. Importantly, management and our analysis treat stock compensation as a cost in evaluating true earnings power. Wix does have substantial stock compensation, but it’s now offsetting dilution with buybacks (more below). On an “owner’s earnings” basis, Wix’s earnings quality is high given the strong cash conversion.

Balance Sheet and Capital Structure

Wix’s balance sheet is sound, though GAAP equity is negative (book value per share is about -$5). The negative equity is a quirk of accounting caused by accumulated past losses and the fact that in Sept 2025, Wix issued $1.15B of 0.00% convertible senior notes due 2030 and repaid $575M of an existing convertible series (at Sept 30, 2025, convertible notes (net) were $1.124B.). What matters more here is liquidity and leverage.

As of Sept 30, 2025, Wix reported: cash & cash equivalents $889.6M, short-term deposits $387.4M, and marketable securities $312.5M (incl. long-term), i.e. about $1.59B combined. Convertible notes (net) were $1.124B, implying net cash/investments of roughly $0.47B before other liabilities. The convertible carries a low interest rate and a conversion price well above current levels (so it’s essentially debt unless the stock doubles/triples). Wix’s debt-to-EBITDA is modest (EV/EBITDA 26x, and net debt/FCF is negligible given net cash). With $600M FCF yearly, Wix could theoretically pay off that debt in under 2 years if it chose. Instead, it’s using cash for buybacks. The balance sheet also shows hefty deferred revenue ($728.7M current + $110.7M long-term = $839.4M) due to pre-paid subscriptions. That’s another sign of a healthy subscription model (money upfront). No dividend is paid (Wix reinvests or buys back stock and from a objective point of view, as a growth company, it’s not really expected to issue a dividend).

In sum, Wix’s fundamentals are objectively robust. Mid-teens growth, improving quality of earnings (GAAP near profitability, strong FCF), and a shareholder-aligned management returning capital. Key financial ratios underscore how undervalued the stock appears: As of mid Febuary, 2026, WIX is ~$70-71 with market cap of ~$3.87B. Using TTM revenue of ~$1.93B, P/S is ~2.0. Using Wix’s 2025 free cash flow guidance of ~$600M, P/FCF is ~6.5.

These are metrics you’d associate with a no-growth and challenged business, not one growing double-digits with a competitive moat. By contrast, Wix’s Rule of 40 performance (14% growth + 30% FCF margin = 44) is among the elite class of SaaS companies, illustrating that it’s both growing and efficiently managed. One could argue the market is “pricing in” a collapse in Wix’s business (more on that fear in Risks), but current fundamentals do not show such a collapse. Contrary to that, they show resilience and adaptation.

Free Cash Flow & Capital Allocation

FCF

Wix’s crown jewel metric is definitely free cash flow (FCF). The company generates cash well in excess of its GAAP profit due to large deferred revenue (customers paying upfront) and because stock compensation is a non-cash expense. Trailing 12-month FCF is over $500M. In fact, Wix’s FCF in the last 4 quarters was about $520M (which aligns with the $478M mentioned for annual FCF as of early 2025 plus growth in 2025). For full-year 2025, Wix guided FCF $600M (i.e., 30% FCF margin). This is a very robust cash generation for a $4.8B market cap company. Even adjusting for one-time items (like the $80M cash cost of acquiring Base44, which affected Q3), underlying FCF is strong. In Q3’25 alone, operating cash flow was $128.7M and capex a mere $1.4M, yielding $127.3M FCF (32% of revenue when excluding one-time acquisition costs). Wix’s business requires relatively low capex (mostly cloud hosting and office equipment), so most operating cash turns into free cash. This fuels the company’s buybacks and provides a buffer for downturns. By comparison, Wix’s FCF margin rivals some of the best SaaS companies and far exceeds the likes of Squarespace or Shopify (which had lower FCF margins and sometimes negative GAAP earnings). Free cash flow durability is one reason some analysts believe the market is underestimating Wix, including us. At 8x Price/FCF, the stock is priced as if Wix’s cash flows might decline, yet management is actually growing FCF (via both revenue growth and margin expansion).

Cash Allocation

Wix has become very shareholder-friendly in its capital allocation. In 2022-2023, under pressure to improve returns, Wix initiated buybacks (e.g. it repurchased $500M in 2022). In Q3’25 alone, it bought back $175M of stock (1.3M shares at ~$136 avg). Now, with the new $2B buyback authorisation, Wix could retire a substantial portion of shares over 2026-27. We can look at this move from different angles, but we believe this is a signal of confidence. Management is effectively saying the best use of excess cash is to invest in its own undervalued stock. It also helps offset dilution from stock-based compensation (Wix issues stock to employees, but buybacks prevent shareholder dilution, i.e. in Q3, shares outstanding actually fell QoQ).

When we look at insider ownership, Wix’s co-founders (CEO Avishai Abrahami, President Nir Zohar, etc.) and insiders collectively own around 3-4% of the company, which we’d consider rather notable for a 20-year-old public company. Insiders have not been significant sellers recently. In fact, data shows more insider buying than selling in recent periods (over the last year, insiders bought around 153k shares and sold 0 shares, per stockinvest.us analysis). This suggests that those closest to the business believe in its upside (or at least are not cashing out at these prices). Additionally, institutional ownership is 98%, meaning major funds are heavily invested. Some prominent investors (e.g. Starboard Value) took positions to drive changes and have largely seen those changes through. An interesting recent development was a US congressman Ro Khanna disclosing multiple small purchases of WIX stock in Nov 2025 (right around the post-earnings dip). While a trivial note, it’s a cheeky anecdote that even on Capitol Hill someone saw value on that dip. :)

Valuation

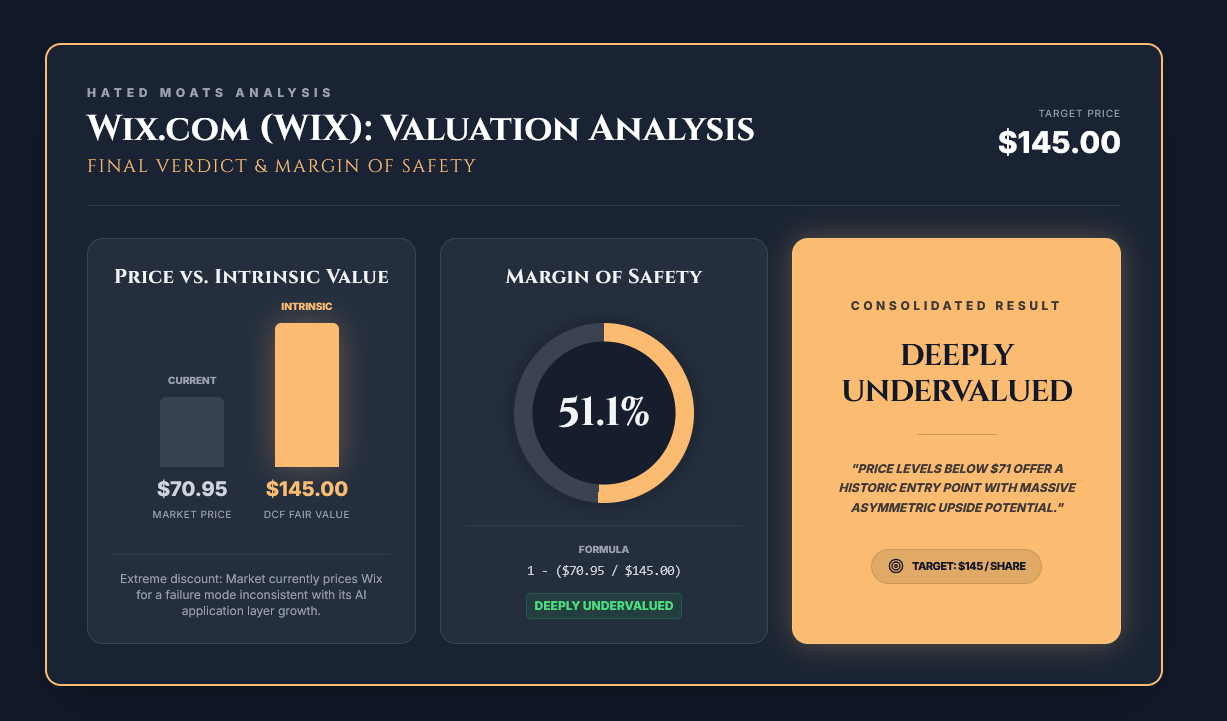

Intrinsic Value & DCF

Wix’s steep stock decline in 2025 and YTD in 2026 has created a disconnect between intrinsic value and the current market price. Our Discounted Cash Flow (DCF) analysis indicates that WIX is deeply undervalued. In fact, we estimate a base-case fair value around $145/share (more than 100% above the mid-Feb 2026 price). This aligns with independent analyses that peg Wix’s fair value in the mid-$160s, as well as the median analyst price target of $160. The unanimity of these valuations suggests that if Wix executes as expected, substantial upside exists.

The market’s current pricing (around $70) implies either a collapse in Wix’s cash flows or a permanently low growth/margin future. Essentially a “terminally challenged” scenario. It’s as if Wix is being “priced for a Chegg outcome,” to quote our analysis. But our view is that this fear is overblown and reductive. Wix is not sitting still awaiting disruption. It’s actively becoming the platform that harnesses AI for web creation. In doing so, Wix may actually expand its TAM (total addressable market) by integrating AI. For example, Base44 targets users who outgrow drag-and-drop but aren’t full coders. If Wix captures this “pro-sumer” segment, it gains a growth vector that wasn’t even in its legacy model. Additionally, Wix’s move upmarket (serving larger businesses via agencies, etc.) increases the longevity and scale of its cash flows. In our DCF, even when we model conservative fade of growth to 4%, the value is well above the current price, meaning the market could be far too pessimistic about Wix’s ability to maintain relevance.

In short, our intrinsic valuation finds significant upside. We must caveat that this assumes Wix can navigate the competitive/AI landscape (see Risks). But given the information as of early 2026 (strong fundamentals, proactive strategy shifts, and capital return), WIX stock appears to offer a margin of safety and attractive return potential. Our DCF-based base case of $145 aligns with management’s own actions (they’re buying back stock aggressively because they see it as undervalued).

You can find the whole valuation analysis HERE. Above, you can see an updated final verdict based on the most recent price (Febuary 12, 2026 at $70.95 per share).

Risk Factors

Investing in Wix is not without risks. The company straddles the volatile tech sector and serves millions of small businesses globally, exposing it to numerous potential pitfalls. Here are, in our view, the key risk factors:

Disruption by AI and New Technology

The foremost risk (and the one that drove the stock down) is that generative AI could commoditise web development. This is the so-called “Chegg scenario” fear. If anyone can prompt ChatGPT (or another LLM) to “build me a website” and get a ready-to-use site, platforms like Wix might see users bypass them entirely. Large Language Models could make coding trivial, undermining Wix’s no-code advantage. Additionally, tech giants (Google, Microsoft) could integrate AI site-building into their ecosystems (imagine Google offering a free AI website builder (perhaps powered by Gemini) to all Google Business users). Such developments could increase competition or force Wix to lower prices. To mitigate this, Wix is actively embracing AI. Base44 and Harmony are attempts to ride this wave rather than be drowned by it. There is a risk these efforts fail to gain traction, but early signs are encouraging - Wix reported Base44 has “over 2 million users served” and indicated Base44 was expected to reach $50M in ARR by year-end 2025. Nonetheless, objective fact is that the moat vulnerability to AI is real. If Wix’s AI features don’t keep pace, or if open-source AI tools become ultra-easy and reliable, Wix could face declining new customer additions or pressure on its subscription pricing (“why pay Wix if an AI tool is free?”). We rate this risk as the most significant long-term threat. We also acknoledge that Wix is objectively doing its best to actively counter it.

Competitive Pressure

Beyond AI, competition from established players is also a risk. Squarespace (now private), Shopify, GoDaddy (how we still hate this company’s name!), Weebly, WordPress,.. All of these fight for a share of online presence. WordPress (with its plugins like Elementor) is effectively free (aside from hosting) and could lure price-sensitive users, especially once their UX is improved. Shopify could move further into general website building from its commerce base. There’s also Wix’s own customers as competitors, ironically enough. Some agencies start with Wix but could switch clients to custom solutions as they grow. And as Wix goes upmarket, it may increasingly bump into Webflow (a popular designer-oriented site builder), Adobe/Magento, or custom dev shops. Wix’s challenge is to remain the most convenient and cost-effective solution. Any stagnation in innovation could see users defect. So far, Wix’s retention is solid (100% net retention in 2024), but switching costs for small websites aren’t insurmountable. A determined small business can move to Squarespace, for example, if frustrated. Wix must continue to invest in product and customer support to keep its edge in this perspective.

Execution Risks (Product Delays, Integration)

Wix’s ambitious product roadmap itself is a risk. The company delayed its “flagship” AI product launch from 2025 to 2026, indicating some execution hurdles. Further delays or misfires (e.g. if Wix Harmony’s user experience disappoints) could hurt credibility and give competitors an opening. Integrating Base44’s tech and user base is also crucial. Cultural or technical integration issues here could prevent Wix from getting the full value out of the $80M acquisition. Additionally, expanding into new areas (like offering more complex web apps via AI) means venturing outside Wix’s traditional expertise. Missteps here could be more prone to happen, incuring costs without returns.

Macroeconomic & SMB Health

Wix’s customers are largely small and medium businesses (SMBs), entrepreneurs, and freelancers. Their ability and willingness to spend on websites is tied to economic conditions. In a recession or tight economic climate, SMBs might cut marketing budgets, delay setting up websites, or downsize premium subscriptions. During COVID, Wix saw a surge as businesses moved online, but in a protracted downturn, new site creation could slow. Moreover, Wix derives some revenue from transactional volume (payments, e-commerce). A consumer spending slowdown would directly hit that Business Solutions segment. Macro indicators to watch here include consumer confidence, retail sales, and small business optimism. Deteriorating trends there could foreshadow softness in Wix’s growth. So far, Wix has shown resilience (2023-25 had high inflation and rising rates, yet Wix still grew 14%), but macro risk is ever-present. Also, foreign exchange (FX) can impact reported revenue. Wix sells globally, and a strong USD could weigh on growth in constant currency terms (the company reports some metrics ex-FX).

Geopolitical and Concentration Risks

Wix is headquartered in Israel with significant operations there. Geopolitical tensions (as seen in late 2023 with conflict in the region) pose a risk to employee safety and business continuity. While Wix has offices worldwide and could shift workloads, any sustained instability in Israel could affect R&D output or morale. Specific regulatory or legal changes (e.g. EU data privacy laws) could impose new compliance costs. Wix manages a lot of user data and must stay abreast of privacy/security regulations. The company has faced occasional legal disputes (there was a patent lawsuit years ago, for instance), though nothing currently appears material.

Financial Risks: Currency, Leverage, Dilution

Wix issued 0.00% convertible senior notes due 2030 (upsized to $1.15B principal in Sept 2025). If interest rates rise further, future refinancings could be at higher rates (though currently the note is low-coupon). Interest rate swings also affect the discount rate for valuing growth stocks (a risk to stock price). As far as dilution goes, stock-based compensation, if not offset, could dilute shareholders. Wix uses significant stock-based compensation. The aggressive buyback should more than neutralise this, but if the stock price spikes or cash flows dip (limiting buybacks), dilution could become 1-2% per year. Also, it needs to be noted that negative GAAP equity by itself doesn’t imply near-term solvency risk. The practical watch-items are liquidity, debt obligations, and cash generation (especially given Wix’s use of converts and repurchases).

Operational Risks

As a cloud platform, Wix must maintain uptime and security. A major outage or security breach (e.g. customer websites hacked, data loss) could damage its reputation. Similarly, any significant issues in the product (say, SEO problems, or templates breaking) could drive users away. Wix also relies on third-party infrastructure (like cloud providers, payment processors) and issues there could disrupt service. Finally, a key personnel risk. CEO Avishai Abrahami is a co-founder and the visionary behind Wix. If he or other top execs were to leave unexpectedly, it could impact the company’s direction (though Wix does have a deep bench, including the President and CTO who are long-timers).

In reviewing Wix’s SEC filings, the risk factors section highlights many of the above, i.e. competition, rapid tech changes, need to innovate, reliance on search engines/social platforms to attract users where adverse changes in their policies/pricing/listings could hurt user acquisition and performance, and intellectual property issues. Notably, one risk mentioned is “the market may not accept our new products/features” - very pertinent to the AI bets Wix is making. Another is “pricing pressure from competitors or partners”, e.g. domain registrars or hosting companies undercutting on price.

Overall, the largest risk is that the market’s fear proves correct. If AI makes websites so easy to create that Wix’s value-add is eroded, or if a new competitor uses AI to leapfrog Wix, growth could stall or decline. In such a bear scenario, Wix could be relegated to a slow-growth utility, justifying the low multiples. Or, worse, it could face user attrition. The second biggest risk is macroeconomic. A severe recession could curtail Wix’s growth for a time (though not destroy the business model). Mitigants include Wix’s own proactive strategy (embracing AI, focusing on higher-value customers who are stickier) and its strong financial buffer (lots of cash, ability to cut costs if needed, which is something they did already before). Also, even if AI tools become prevalent, there’s an argument that many small businesses will still prefer an all-in-one service like Wix to handle hosting, security, commerce, etc. The UI might change (voice or prompt-based design instead of drag-and-drop), but Wix can adapt to that. As a matter of fact, that’s what Harmony and Base44 aim to do.

In conclusion, while Wix faces real headwinds and the stock’s volatility reflects those risks, none of these are insurmountable. The company’s recent actions (cost discipline, AI pivot, buybacks) suggest it is aware of challenges and actively addressing them. Investors should keep a close eye on user growth, churn, margin trends, and the competitive landscape for early signs that any risk is manifesting materially. So far, the evidence (growing ARR, stable cohorts) indicates Wix’s moat is holding, but risk management will be key to realise the bullish scenarios.

Our Scenarios (3–5 Year Horizon): Bull, Base, Bear Case

Bull Case (20% Probability)

Key Assumptions

In the bull case, Wix surprises to the upside on growth and cements a formidable position as an “AI web platform,” flipping the narrative from fear to “Wix as a leader of a new paradigm.” Base44 and Wix’s AI initiatives succeed beyond expectations, while Wix Harmony and vibe coding attract a new wave of users such as makers of web apps, not just websites. Wix finds a way to monetise AI-driven creation through premium services, materially boosting ARPU. A “killer app” emerges that allows growth to re-accelerate to around 20%, for example if Wix becomes the go-to platform for small businesses to build simple native apps or other digital experiences, expanding TAM. Wix also has to demonstrate that AI is not merely defensive but a true growth catalyst, with Base44 potentially reaching $60–90M ARR by 2026, $80–120M ARR by 2027 and continuing to scale, adding several points of growth. In parallel, Wix’s push into agencies and enterprise via Wix Studio / Enterprise solutions gains traction and brings larger clients on board (incrementally, but meaningfully). This scenario further assumes benign competitive dynamics, either because competitors struggle with their AI efforts or because the market expands significantly as more businesses come online globally. Finally, excellent execution is required (i.e., no major product flops and continued high customer satisfaction), allowing Wix’s brand to evolve from a “website builder” into an indispensable platform for SMB digitisation. This bull scenario is framed as roughly a 20% probability in our model, and it builds on the view from some analysts that Wix may be substantially below intrinsic value with strong long-term earnings power.

Financial Outcomes

If the bull scenario plays out, revenue growth stays in the mid-teens to around 20% for several years rather than decelerating, and within ~5 years revenue could exceed ~$4B. With growth that robust, margins may expand as Wix scales overhead and benefits from higher operating leverage, potentially driving FCF margins into the low-to-mid-30% range. The $2B buyback executed at low prices would retire a meaningful amount of stock and amplify per-share results. In that context, investors could plausibly see a 2-3x return, with a stock price in the $300-$380 range, which is characterised as still reasonable on forward multiples (roughly 3.5-4.5x sales and 12-16x FCF on late-2020s numbers) for a SaaS business growing at high-teens rates.

Base Case (60% Probability)

Key Assumptions

In our base case, Wix executes its strategy and continues to grow as a healthy, if not explosive, compounder. The company sustains low double-digit revenue growth of roughly 10-15% for the next 3 years, then transitions to high single-digit growth beyond that. Creative Subscriptions expand in the high single digits as Wix adds new subscriptions globally and modestly raises prices or ARPU, while Business Solutions grows faster (mid-teens to 20% early on) as more users adopt Wix Payments, e-commerce, and related monetisation tools. Base44 and AI features improve the business model rather than disrupt it by reducing churn and increasing upsells, with net revenue retention improving from 100% toward 102-105% as AI/Business Solutions upsells offset churn, and some users moving into higher-tier plans or purchasing AI add-ons, collectively contributing a couple points of incremental growth. Wix continues to hit “Rule of 40+” performance, with AI acting as an augmentation that increases customer value and lifetime rather than compressing monetisation. FCF margins around 30% are maintained or slightly improved in this scenario, potentially toward 32-35% if scale economies persist, as operational efficiency offsets incremental AI cloud costs. Competition remains manageable, the core user base stays resilient with no mass migration away, macro conditions are neutral to mildly positive without a deep recession that wipes out SMB demand. Capital allocation remains disciplined with executing buybacks without starving growth investments. As confidence builds, the market gradually re-rates Wix’s valuation multiples upward, reflecting belief in a stable growth trajectory into the late 2020s.

Financial Outcomes

With these assumptions, Wix’s EPS and FCF grow in line with or faster than revenue because of net share count reduction of 1-2% per year (after offsetting SBC) while 2-3% is achievable if repurchases remain aggressive and the stock price stays subdued. The net effect is a steady compounding profile consistent with targets like 12% growth paired with a 30% FCF margin. By 5 years out, in this scenario, Wix could be generating $2.9–$3.2B revenue and $850–$1,000M FCF (28-32% FCF margin), assuming revenue CAGR high single-digits to low teens and AI unit costs don’t structurally depress margins. If the market applies a moderate valuation (such as 15x free cash flow or a PEG around 1 for a 12% grower), the stock would more than double from today. This supports our base case valuation around $145 and potentially price target of $170-180 over a 3-5 year horizon, alongside a potential multiple expansion where forward P/E rises to around 20x as investor confidence increases. This outcome is framed as the median expectation and we assign it the highest probability at 60%.

Bear Case (20% Probability)

Key Assumptions

In this scenario, AI tools become widely available and commoditise basic web design, narrwoing Wix’s differentiation, which slows Wix’s new user growth and proves the pessimists partly right. A plausible trigger is a large tech company launching a free AI website builder bundled into its broader cloud ecosystem, siphoning off would-be Wix customers. New premium subscriptions slow sharply and churn increases as more tech-savvy users migrate to cheaper alternatives. Wix’s pricing power erodes, forcing heavier discounting or keeping entry plans low to remain competitive. At the same time, intense competition in payments and e-commerce (especially from the established platforms) caps Business Solutions growth. Operationally, Wix struggles to balance investment and efficiency. It may spend aggressively to chase growth and retention, compressing profitability, or cut costs too deeply and weaken innovation, further undermining differentiation. Even if gross margins remain relatively healthy in the mid-60s to 70% range, incremental marketing and competitive pressure prevent meaningful operating leverage. This downside setup also assumes Wix’s own AI initiatives disappoint, with no material lift from efforts like Base44 or Harmony, and that alternative AI solutions undercut Wix’s value proposition enough that small businesses feel comfortable building and managing sites without Wix’s tooling and support. A severe external shock, such as a multi-year recession that drives widespread SMB failures, could further reinforce this dynamic.

Financial Outcomes

Revenue growth decelerates quickly and falls to low single digits here, roughly 3-5% annually, within a couple of years. FCF margins compress into the low 20% range as economies of scale are offset by higher marketing spend needed to retain users and defend share. With a slower growth and lower margin profile (around 4-5% growth paired with 20-25% free cash flow margins), intrinsic value drops meaningfully, a plausible downside is FCF falling to roughly $450-$600M with the market applying 10-14x FCF, which could justify a stock price in the $75-90 range. Over a 3-5 year period the stock could trade sideways or drift lower, underperforming the market, as FCF stagnates and the narrative shifts toward a vulnerable moat. Even so, the company would likely remain profitable and cash-generative, making this less an existential collapse than a “value trap” outcome. This is framed as a lower-probability scenario at about 20%, partly because Wix would still have strategic levers (such as moving upmarket or emphasising cost discipline and realising buybacks) to protect cash generation and value to shareholders even if growth weakens.

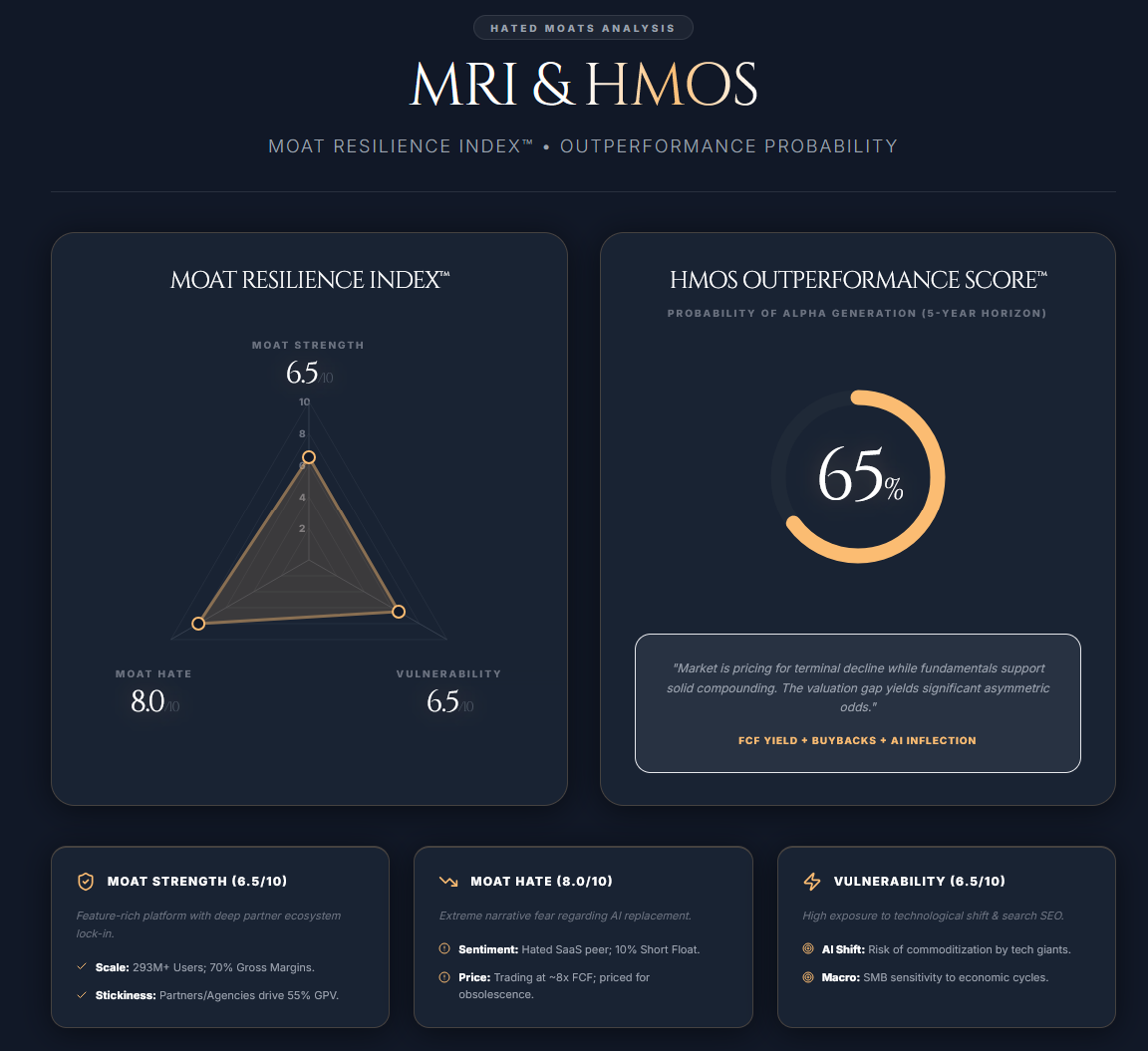

Moat Resilience Index™ (MRI)

We assess Wix on our proprietary Moat Resilience Index™ (MRI), focusing on three dimensions – Moat Strength, Moat “Hate”, and Moat Vulnerability.

Moat Strength: 6.5/10

This is an assessment of how durable and strong Wix’s competitive advantages are. Wix earns a 6.5, i.e. a solid, but not unassailable. On one hand, Wix has a strong brand, huge user base, and a decade head-start in building out features and infrastructure. Its platform is feature-rich (covering domains, hosting, design, commerce, marketing, etc.), creating convenience and one-stop-shop appeal that new entrants would struggle to replicate quickly. The ecosystem of third-party apps and agency partners adds switching costs. Many web developers have built businesses around Wix, and users have their sites and client data embedded in Wix’s ecosystem. The recurring subscription model with good retention also points to a sturdy customer base (Wix isn’t a fad, businesses need websites continuously). On the other hand, the moat is not immune to competition. Alternatives exist and the cost to switch, while non-zero, is not prohibitive for motivated users (a savvy user can recreate a site on WordPress or Squarespace) and the the cost to switch could reduce significantly if a UX-friendly alternative would be pushed broadly by a tech giant, for example. Additionally, Wix operates in a tech realm where continuous innovation is required. Today’s moat can be eroded if a competitor builds a better mousetrap. But overall, we view Wix’s moat as resilient. The combination of brand trust (for a non-technical customer, using Wix is a safe choice), network effects in its partner community, and scale (allowing it to invest above 30% of revenue in R&D and leverage marketing across millions of users) gives it an edge. We also note Wix’s high gross margins and improving retention as evidence of pricing power and customer stickiness. Those are signs of a viable moat. Thus, 6.5/10. Strong, though challenged by emerging tech trends.

Moat Hate: 8/10

This measures how disliked the company is by the market - essentially, the contrarian appeal. Wix scores a 8 here, indicating extreme pessimism has been priced in. The stock’s 2025 plunge (continued well into beginning of 2026) and 70% drop from its Jan 2025 peak show that investors have heavily discounted Wix over fears of AI disruption and slowing growth. Short interest is elevated (around 10% of float) and until very recently, sentiment on forums and headlines was very negative. When a fundamentally profitable, growing company trades at <10x cash flow and some analysts see 100% upside to targets, you know it’s hated in the market. This “moat hate” is actually a positive for contrarian investors who have enough conviction. It means expectations are low. We give it 8/10 because while sentiment has ticked up slightly with the buyback news, the “SaaS carnage of 2026” continues and Wix is still among the more disfavoured cloud/software stocks (many peers trade at far richer valuations). The high “hate” score implies potential for outsized gains if the narrative shifts.

Moat Vulnerability: 6.5/10

This reflects how vulnerable the moat is to being breached or weakened. We score Wix a 6.5, meaning moderately vulnerable. The biggest vulnerability, as discussed, is technological disruption. Specifically, the risk that the very concept of a dedicated website-building platform becomes obsolete in an AI-driven world. If, for instance, future businesses simply use an AI agent that manages their entire online presence (social, web, ads) without the need for a Wix-like interface, then Wix’s role could diminish. Another angle could be price-based competition. There are free or open-source solutions (WordPress, etc.) that could gain capabilities, potentially pressuring Wix on price/value. Wix is also vulnerable to platform dependency. A lot of its traffic comes via search engines. If Google ever favoured its own site builder or changed SEO rankings in a way that made Wix sites less visible, that could hurt (Wix has worked to improve its historically weak SEO reputation, but the vulnerability remains that a change outside its control could impact customer success). Furthermore, SMB customers can be fickle and sensitive to cost. A large hike in Wix’s pricing or economic stress can lead to churn. That’s not a vulnerability unique to Wix, but part of its customer profile.

We give 6.5/10 because while Wix has countermeasures (it’s adopting AI, it’s moving upmarket to more stable clients, etc.), the rapid pace of tech means its moat could be partially eroded if they ever fall behind. It’s not as invulnerable as, say, a company with network effects like a social network or a monopolistic market position. However, it’s also not extremely vulnerable. Wix has shown adaptability and has multiple revenue streams (subscriptions, payments, new products) to buttress against one area weakening. So, we assign a moderate vulnerability. There are real risks, but manageable with strong (or perhaps even good enough) execution.

Hated Moats Outperformance Score™ (HMOS): 65%

Taking the above into account, we estimate a 65% probability that Wix will outperform the S&P 500 over the next 5 years. This probability is warranted by Wix’s combination of low market expectations (and thus a lower bar to beat) and solid fundamental momentum. Essentially, the market is pricing Wix like a company that might shrink or barely grow, whereas we find it more likely to keep growing and compounding cash flow. This gap yields a meaningful chance of outperformance. A 65% probability doesn’t mean Wix is risk-free, but it indicates our conviction that, over a multi-year horizon, an investment in WIX today has better-than-even odds of delivering stronger returns than a broad market index.

Supporting factors include: Wix’s FCF yield (cited 12-15%) provides a built-in return component that is already competitive with long-term equity returns. If the company simply maintains value, shareholders can still benefit via buybacks improving per-share value; any growth or multiple expansion is incremental upside. Moreover, the stock’s beta (~1.4) suggests it can swing, but given the current low valuation, the swings could be asymmetric to the upside if fears abate and fundamentals remain intact. We acknowledge the 35% chance it doesn’t outperform, primarily if our bear case (or elements of it) occurs. For example, slower growth combined with no multiple improvement, or AI-driven pressure on conversion/retention that keeps sentiment depressed. But more likely, Wix’s current pricing offers a cushion such that even middling outcomes can yield decent returns.

Conclusion

Wix.com Ltd. presents a compelling case of a fundamentally strong company whose stock has been beaten down by an overreaction to emerging risks. The business has shown the rare combination of steady growth, improving profitability, and shareholder-friendly actions. Yet the market remains sceptical, largely due to fear of AI disruption and perhaps general tech fatigue. After deep analysis, our view is that Wix’s core franchise (enabling and empowering the online presence of millions of small businesses) remains valuable and durable, and the company’s proactive adaptation (incorporating AI, moving upmarket) will likely strengthen its moat rather than destroy it. The current valuation offers a wide margin of safety, with the stock trading at depressed multiples versus its own history and many software peers.

From a classic value-investing standpoint, we believe Wix is the kind of situation where the market’s short-term anxieties have created a long-term opportunity. The stock is hated (in sentiment) but the business itself is not broken. In fact, it’s generating strong cash flows (2024 FCF was $478M / $488M excluding HQ build-out, and management guided $600M FCF for 2025). This asymmetry between perception and reality is exactly what we look for at Hated Moats. Of course, no investment is without risk, and we have detailed those. Mainly, the risk that AI changes the game in ways we can’t fully predict, and assuming Wix fails to fully adapt to. But weighing everything, we find that Wix’s management has earned some credibility (they delivered on margin promises early, and they are investing where needed while still returning cash to owners), and that the company’s long runway in the massive SMB digitalisation space is not reflected in the current price.

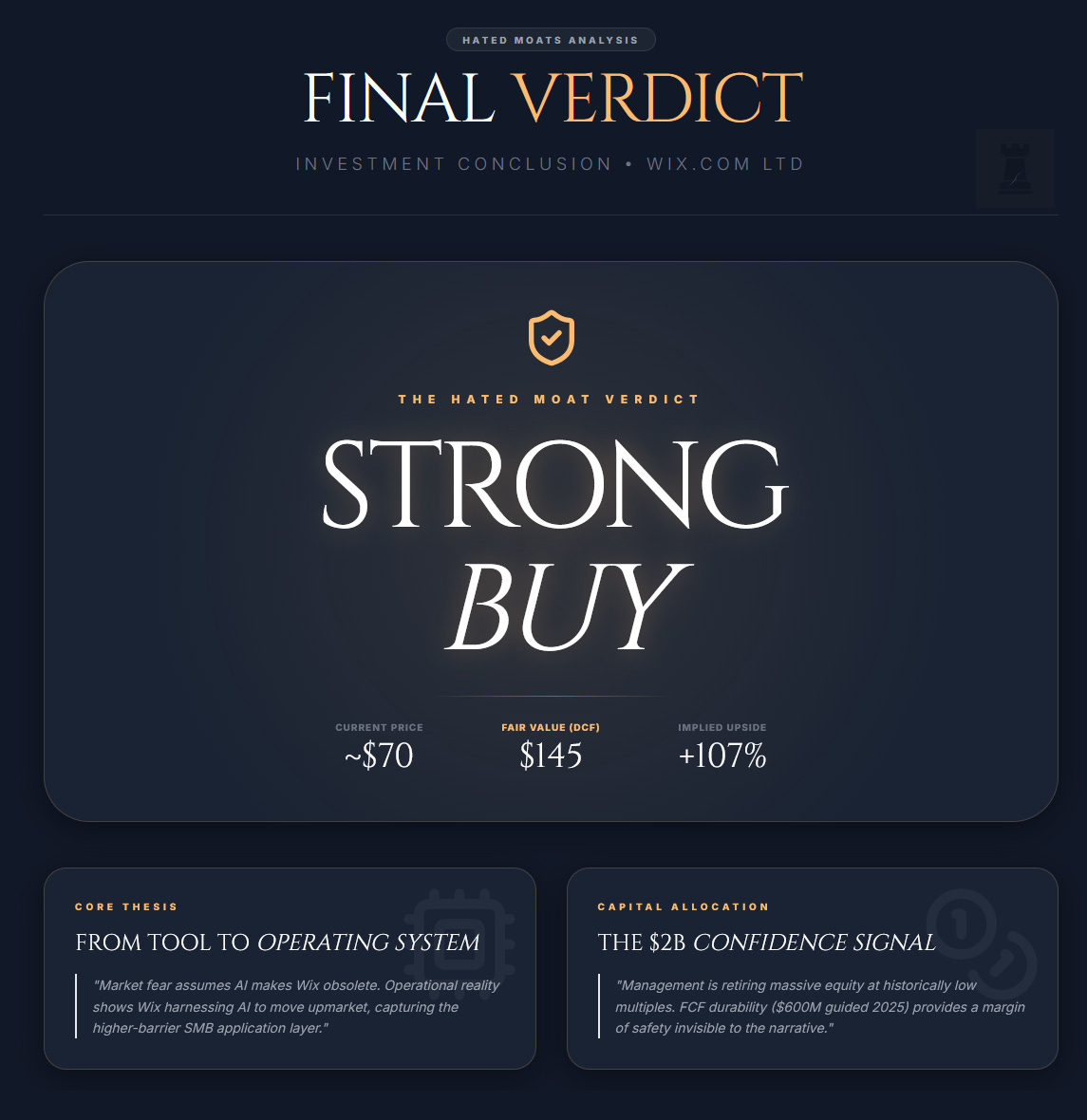

Final Verdict

We rate WIX as a Strong Buy. Our conviction is high that the stock is undervalued and poised for significant upside. At around $70/share, Wix offers a rare mix of value and growth. Value in its low valuation on cash flow (and a discounted earnings multiple versus many profitable software peers) and hefty buyback yield, and growth in its double-digit sales increase and optionality from new AI products. Our DCF-based price target of $145 underscores the upside potential, and even that may prove conservative if the bull case unfolds. Any sign of re-acceleration or simply maintenance of guidance could be a positive catalyst, given how low expectations are. In the long-term (3-5 years), we see Wix potentially compounding shareholder value at an attractive rate, driven by its expanding ecosystem and high cash generation. By that horizon, if Wix executes well, it could very likely trade well above its prior highs, especially as the share count will be considerably lower if $2B in buybacks are completed.

To close this one up, Wix.com exhibits the hallmark of a “hated moat” situation. A solid (even widening) moat that the market hates for transitory or speculative reasons. This disconnect is our opportunity. With a professional management team, improving financial metrics, and a clear commitment to innovation, Wix appears positioned not just to survive the AI era but to harness it. Investors who can look past the doom-and-gloom headlines and focus on fundamentals may find Wix to be an unexpected winner in the coming years. We would not be surprised to see sentiment do a 180 turn. Today’s pessimism can turn into tomorrow’s optimism once results speak for themselves, and all we’ll see will be “it was so obvious” and “we all knew this was gonna happen” as a new general consensus. Hence, we confidently label WIX as a Strong Buy, expecting substantial alpha over the mid to long term. The stock is down, but far from out. In our analysis, the downside scenarios are well overshadowed by the upside potential of this hated moat.

Disclaimer & Our Investment

The author of this report does hold a position in the security of Wix.com Ltd. in private portfolio since Jan 27, 2026 at $86.42 per share as well as a position in our Hated Moats Portfolio from the same date, with avg. price of $86.72. This report is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

Wix will be disrupted by AI website builders. We run our site (and several others) through Wix, but we're moving. We build a much better website in 1-2 days with others, such as Framer and other website builders. (We actually had Wix on our watchlist 2 years ago, due to the massive lock-in effect, but to be honest, it's gone). We also know quite a lot of other entrepreneurs who will be leaving.

But hey, maybe we're wrong! One thing is for sure, Wix needs to more with AI (and better!). It currently sucks.